Download PDF:

The news related to Evergrande default last month has reignite investors attention to the country real estate sector, which is a major driver of Chinese growth and strongly intertwined to the country’s banking sector. Moreover, property accounts for 70% of household wealth – a significantly higher portion compared to U.S. and Japan at 50% and 35% respectively – and correction in housing price could dent consumer spending through the declining wealth effect.

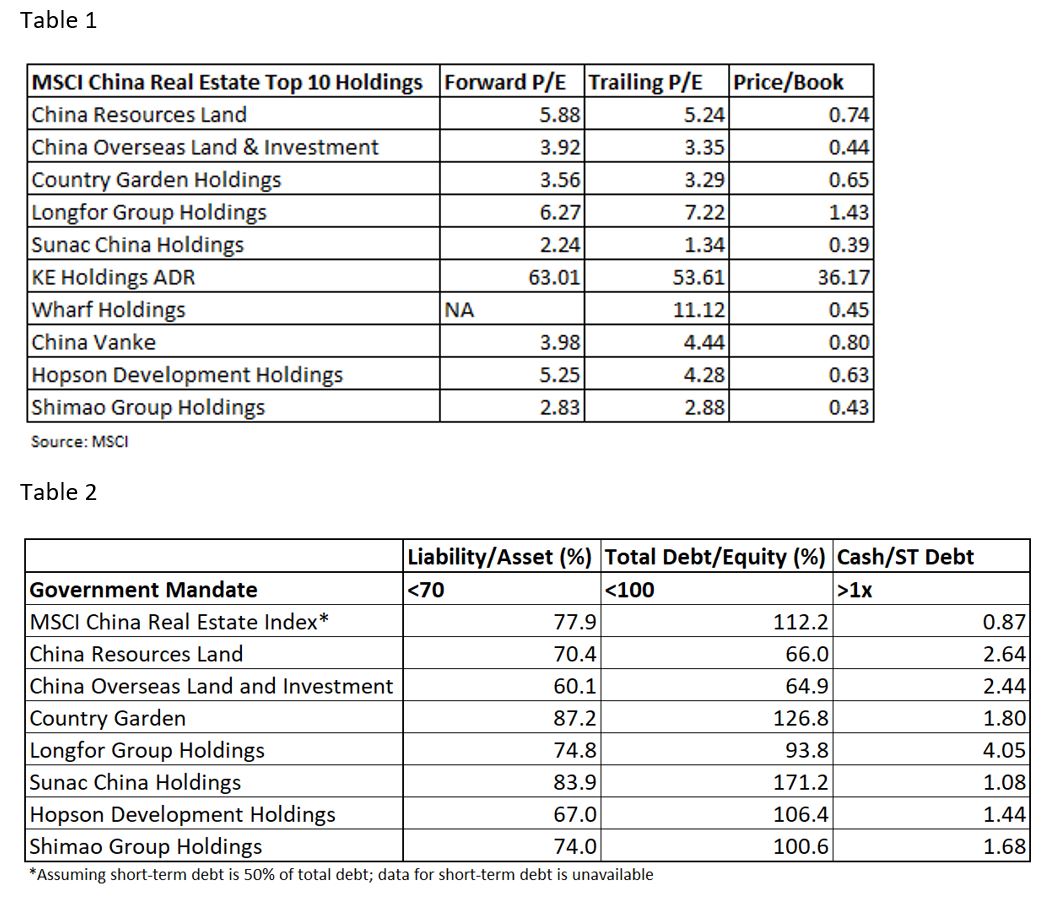

Majority of Chinese property developers has an inherently high leverage that violates Chinese government “three red lines” and may not survive a prolonged downturn in the sector. Table 1 shows that in August, among the top 8 developers listed in MSCI China Real Estate sector, four of them have cash to short-term debt ratio less than two and both their bond and stock prices have wobbled. In fact, the whole sector is trading at a distressed forward earnings ratio and valued below book value – highlighting the going concern issue for the whole sector (Table 2).

It is doubtful that the government will force the domestic developers to deleverage quickly, as it would worsen the liquidity problem, but a gradual reduction in debt ratio and investment in the coming years is likely, which would cool activity and bode especially poorly for the second and third tier city. Already there are signs that mortgage lending has been eased following the decline in house prices last month, and this week Evergrande surprisingly pay its offshore dollar bond coupon before the end of its 30-day grace period.

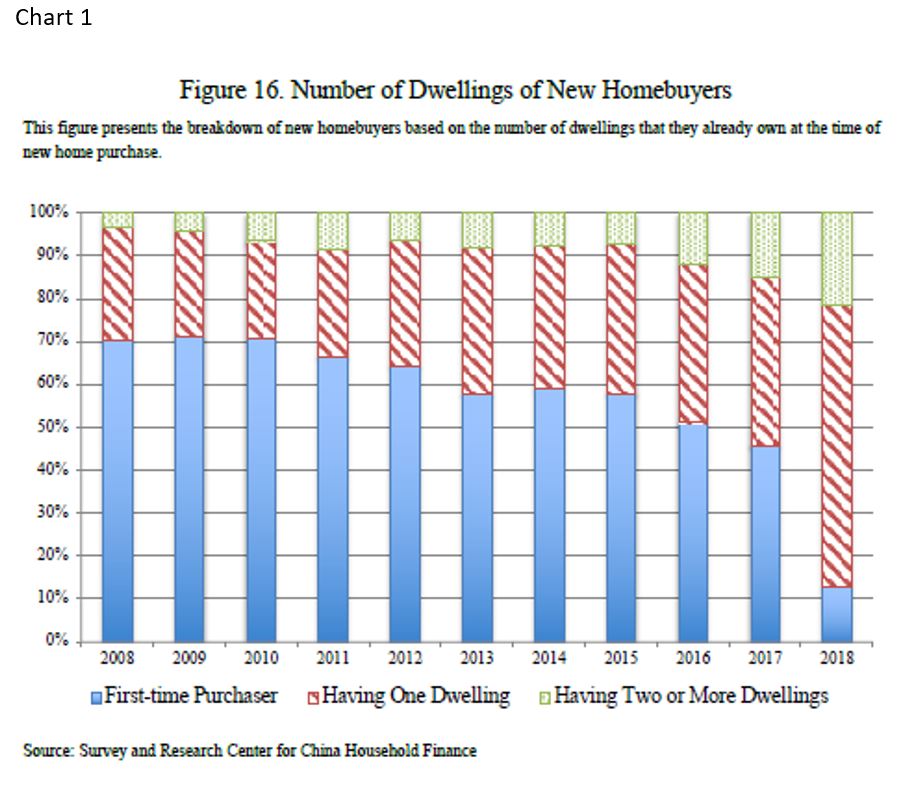

In a controversial paper, Rogoff and Yang (2020) discussed the downside risk for Chinese house prices as population growth is slowing and housing transaction is increasingly dominated by those already having a primary dwelling (Chart 1). With the government mulling for a property tax to curb speculation in real estate, many will be tempted to shift their wealth allocation from real to financial assets, a potential trigger for cooling in prices.

Structurally, there are several reasons weighing China’s real estate activity:

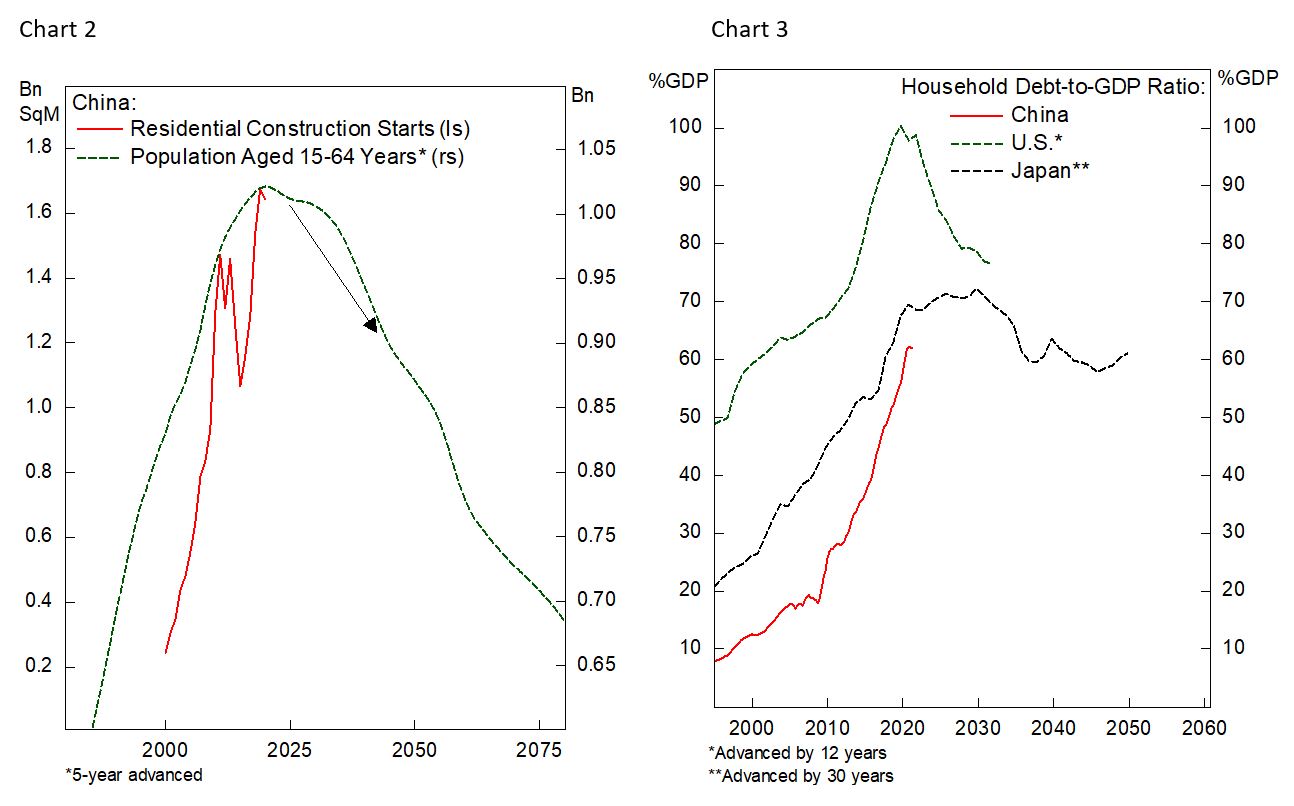

- The country is facing a declining working-age population, a structural headwind for housing construction, but at only 65% urbanization rate, construction demand in big cities should fare better (Chart 2). Chinese rural population will continue to move to big cities where higher-paying job is located and drive demand for residential property. This will support demand for construction in Chinese cities at the expense of abandonment of villages.

- Chinese household leverage is rather high for its income level and an accelerated rise since the Global Financial Crisis (GFC) has coincided with rising residential expenditure for households (Chart 3). Without a rapid income growth or structural decline in interest rate, high residential prices bode poorly for household consumptions and further lower Chinese real GDP growth. With households already stretched by mortgage payment, demand for property should decline on the margin.

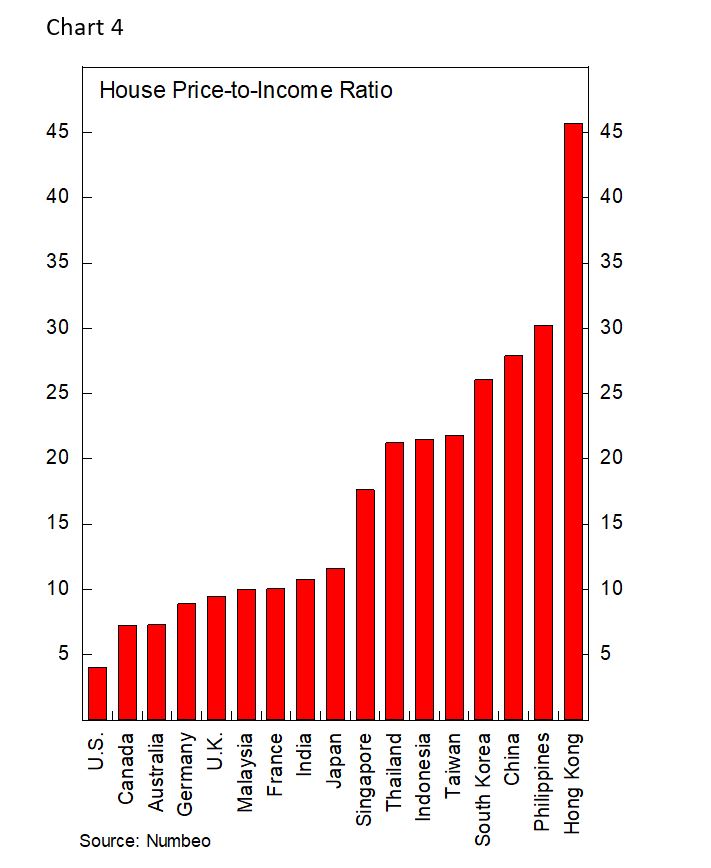

- House price in China is comparable to those in large cities around the world, despite household income at a fifth of those in the rich world (Chart 4). The high unaffordability level of Chinese real estate is squeezing younger population from the housing ladder and building a family, which is one among many social issues Chinese government is aiming to resolve. The government has continued to limit the share of bank lending to real estate sector, which raise their cost of capital and make it difficult for developers to take on new projects aggressively as in the past. Although in the longer-term this will likely make the supply of property even more acute, tightening in access to capital will weigh down construction activity in the medium term.

The Fate of Chinese Property Developers and Local Governments

As mentioned in the previous section, a declining working-age population means housing demand will also gradually decline, although demand in large cities could remain strong as urbanization could add housing demand for another 200-300 million workers. Developers who are focusing on projects in large cities should continue to do well, but those in second and third tier cities will do worse. Already there are signs of overbuilding in smaller cities – vacancy rate is quoted at above 20% in tier-2 and 3 city and inventory is at 3 million square meters or equivalent to two years turnover.

Moreover, a prolonged crackdown in the real estate sector means that developers with weak balance sheet and low cash to short-term debt ratio will go under. It is not impossible for the government to take real estate construction from the private sector to under local government, which will be losing revenue from lower land sales to developers in the medium term.

Help from Beijing is needed for the government to balance its fiscal, on top of the introduction of property tax that could partly offset the lose of income from land sales. Without direct transfer from Beijing, local government will be forced to slash expenditure and tighten significantly, which probably explains the weakness in state-owned investment of late. In addition, such weakness in local government finances will expose Chinese government to another problem in Local-Government Financing Vehicle (LGFV), which is an opaque tool issued by provinces to fund projects and likely plagued by capital misallocation. We are doubtful that Beijing wants to deal with another mini crisis when growth rate is already very weak.

In the longer-term, Chinese GDP growth may average under 6% in the coming decade, with the impact from slowing real estate and construction activity accounting for 0.7-1% decline of real GDP growth annually (Chart 5 and 6).

Global Macro Impact

Chinese growth of only 0.2% in Q3 highlights downside risks to global post-pandemic recovery and risk assets. We have been arguing for some time that global growth will moderates in the second half this year amid reversal of the fiscal and monetary stimulus and growth normalizing back to trend. This process is still underway in U.S. and Europe, which currently still enjoys expansion in manufacturing activity and strong retail sales.

However, the pace of growth deceleration in China has been faster than what we expect amid the lack of easing from fiscal and monetary policies. Loan growth and total social financing remain tepid, while there is no sign that PBoC is ready to cut rates or further lower the reserve requirement ratio for banks, after cutting it in July. This caused Chinese government bond yield to go back up and is effectively a monetary tightening for the economy. This should translate to weak Chinese growth in the next 3-6 months, with implications for risk assets.

- Short copper. Chinese building construction accounts for 15% of global refined copper demand. Recent spike in price is driven mostly by supply concern, as smelters across China – where 6 out of 10 largest refiners are located – are shut down due to the electricity shortage. Decline in coal prices is a proxy for the easing in energy crisis, which will bring industrial metal prices lower. We will be writing about this issue in an upcoming publication.

- Long/overweight U.S. Treasury bonds. Despite the threat of inflation being longer than expected, we maintain our view that supply-driven inflationary pressure should not force the Fed to tighten next year. Tightening by the Fed, at a time when there are still 5 million of workers out of employment, will be a policy mistake. Negative gap of 5-year/5-year forward inflation and 5-year inflation expectation and flattening yield curve highlights market conviction that inflationary pressure is temporary and a rate hike will necessitate a reversal afterwards. Tepid Chinese growth and slowing growth outlook will weigh the upside potential of Treasury yield.

- Underweight EM equity and bonds. Commodity-sensitive countries will suffer from slowdown in Chinese growth and will face rising risk premium from tighter global financial condition. Political risk in Latam is also rising: fiscal discipline is becoming an issue again for Brazil and President Bolsonaro is becoming more confrontational heading to next year’s election; Chile is facing a shift to the left and November’s election will likely confirm this trend; Peruvian political risk seem to have peak with the president showing signs of moderation, but the country outlook remains uncertain.

- Stay away from U.S. High Yield Corporate bonds. The risk/reward trade off is very poor amid compressed spread and increase in leverage. Just as massive QE last year brought spread to record low level, tapering of QE by the Fed next month will cause repricing of the asset class.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.