The jitter surrounding Evergrande’s solvency problem has spread to other Chinese property developers that account for sizeable portion of Chinese and Asian High Yield Corporate index. Chart 1 and 2 show spreads of Chinese and Asian USD bonds have widened to 16% and 11.5%, respectively, while the total return index declined 18% and 12% from the peak early this year. Despite yields already at double digit level, however, the risk for both Chinese and Asian High-yield bonds remain on the downside, for the following reasons:

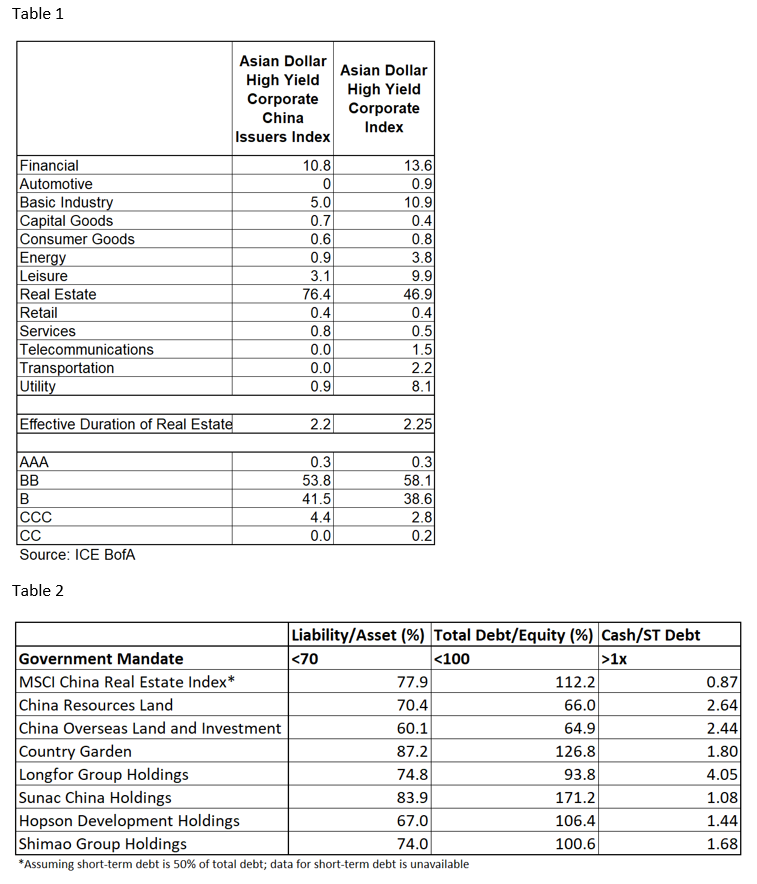

- First, both index is heavily concentrated on bonds issued by Chinese real estate developers, which are currently facing macro and regulatory headwinds (Table 1). As in every other sector, companies issuing large amount of debt, and hence have a greater weight in the bond index, usually have a more vulnerable balance sheet. This leaves investors tracking the index more exposed to vulnerable firms.

- Second, most developers have a high leverage ratio and are in violation of one or all the government three red lines – a liability-to-asset ratio of less than 70%, a net gearing ratio of less than 100%, and a cash to short-term debt ratio of more than 1x (Table 2). This means that as long the government maintain its hawkish stance on forced deleveraging of property developers and tightening credit through domestic banks, a mass default of Chinese real estate companies with weaker balance sheet could not be ruled out. Already, bonds of some other large developers have been under pressure (see appendix).

- Third, low duration of both indices (Table 1) means issuers are dependent on near-term liquidity to rollover their financing. With investors turning cautious on Chinese real estate developers and domestic banks constrained or unwilling to extend financing to developers, the latter could face a cash crunch that potentially led to a solvency crisis – similar to the Evergrande saga – despite potentially being solvent under normal business condition.

- Lastly, uncertainty related to potential government intervention translate to difficulty in estimating default rate and recovery value. Moreover, Chinese authorities may see that the default of offshore bonds to be irrelevant for domestic financial stability, potential lowering its recovery value much below that of bank loans and onshore bonds.

The bottom line is that unless the government steps back from its deleveraging campaign of property developers, it is likely that we will see more defaults by weaker developers and further spread widening. In the near term we expect volatility will remain high as restructuring is being worked out on Evergrande, making it too early to bottom fish high-yield credit of Chinese and Asian bonds.

Appendix

Sunac China Holdings: Liability/Asset 84%, debt/equity 171%, cash/short-term debt 1.08x

Hopson Development Holdings: Liability/Asset 67%, debt/equity 106%, cash/short-term debt 1.44x

Shimao Group Holdings: Liability/Asset 74%, debt/equity 100%, cash/short-term debt 1.68x