Download PDF:

The Brazilian 10-year bond yield has continued to shoot up to 11% this month amid the political debacle in the country and lack of credible proposal from the government to reign its growing public debt. A hawkish Fed, deterioration in Chinese growth and flareup of the pandemic globally all point to downside risk for EM risk assets. We had been positive on Brazil and other resource rich countries up until the first half of the year amid the improving global growth outlook and rally in commodity prices and downgraded them early last month due to peaking global growth and poor credit numbers coming from China. Going forward, the cyclical tailwinds will continue to diminish while the country’s structural problems are coming to light.

First, Brazil is sliding further into a fiscal crisis amid the government’s lack of political capacity to enact tax and expenditure reforms. After the pension reform in 2019, there is no major steps taken by the government to curb its deficit while the very generous pandemic-related spending has more than offset the gain from the former (Chart 1). This week the vote on tax reform bill is being postponed for the third week straight amid an impasse in the Congress, and an eventual agreement of the bill will likely see it being watered down significantly – reducing the potential tax revenue collected. Meanwhile, a fifth of government revenue is dedicated for paying the country’s debt burden, a number that is set to continue to rise and further push Brazilian bond yields higher (Chart 2).

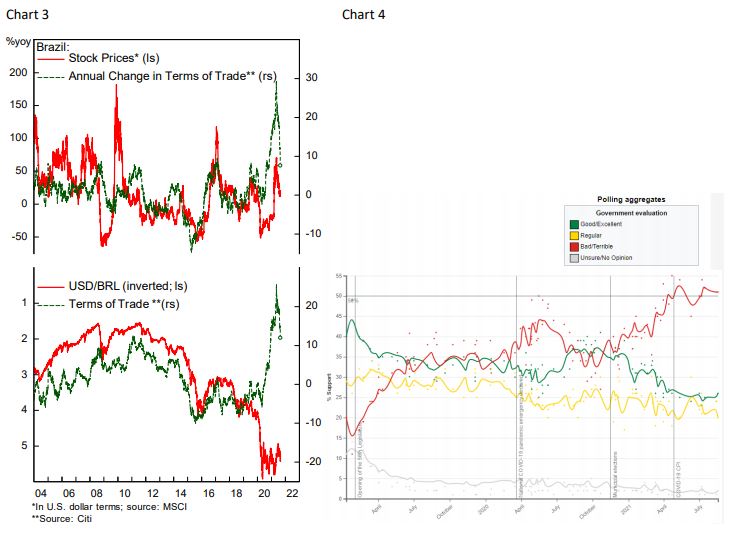

Second, Brazilian growth outlook will continue to be weak amid the country’s complicated tax system that dissuade private sector investment and limited government resources for productivity-enhancing investments – even before the pandemic more than 70% of the government revenue is earmarked for mandatory expenses. Cyclically, the current reversal in agricultural and iron ore prices bode poorly for its terms of trade and exports. Despite still being cheap from valuation perspective, Brazilian stocks and the Real will be bogged down by the decline in commodity prices, while risk premium could further rise amid the deterioration in government fiscal revenue and political uncertainty (Chart 3).

Lastly, President Bolsonaro’s erratic behavior will likely persist until the election in October next year and push risk premium higher. His popularity continued to decline amid the poor management of the pandemic, corruption allegation on his family, and efforts to dismantle the country’s democratic institutions. Recent polls show that his disapproval rating has risen to above 50% (Chart 4). Already President Bolsonaro is laying the groundwork for a voter fraud allegation should he lose next year’s election. He has insisted on using paper voting receipts for the election, a proposal that failed to pass the three-fifth majority threshold in Congress last month. In addition, the president is currently on probes over unfounded election fraud claims that could result in him being disqualified from running next year. The alternative, however, could mean former President Lula da Silva from the left-wing Worker Party winning, under whom Brazilian fiscal expenditures were rising rapidly and eventually culminated into 2015 fiscal crisis.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.