Download PDF:

- We remain positive on some EM local currency bonds, favoring countries with higher yields and cheaper currencies, stronger external profile, and lower interest burden. Investors should overweigh local currency bonds in Indonesia, China, Colombia and Russia, and under weigh those in India, Philippines, Malaysia, Taiwan and Chile.

- Valuation is cheap for both Brazilian and South African bond and currency, but the combination of poor fiscal outlook, rising political risk and weak external profile means both countries will suffer the most during global risk-off period. A correction in the commodity complex, tightening monetary policy and fiscal drag could further undermine these countries growth outlook.

- Declining bond yields in select countries should also push down equity earnings yield lower, at a time when earnings are still rebounding from the pandemic effect. The case is even stronger for Russia and Colombia amid the prospect that oil price could stay high for longer due to OPEC+ agreement last month.

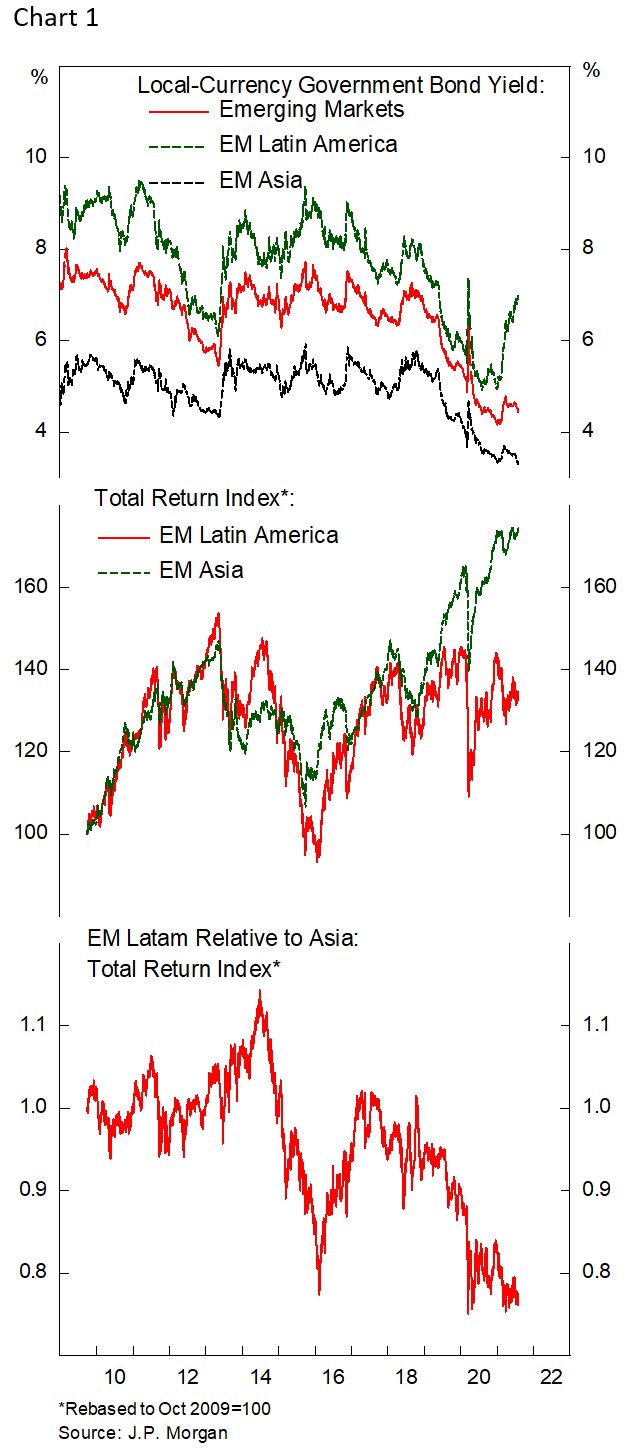

The performance of EM local currency bonds has diverged since early this year with EM Asian bonds significantly outperforming its Latam counterpart (Chart 1). Political volatility in Colombia, Chile, Peru and Brazil brought their borrowing cost much higher and added downward pressure for currencies, while the more developed Asian countries’ bonds have rallied amid risk-off sentiment from worsening pandemic situation. This week we are updating our framework and tweaking some positions in anticipation of a shakeout in global risk assets. In addition, the second part of the report discuss policy rate expectation for major EM countries and their implication for respective countries’ local currency bonds and stocks.

The Selection Criteria: Ranking EM Bonds Attractiveness

Our bond allocation is based on four-criteria selection process, and we are adding a fifth in this report to account for the downside risk during market turmoil.

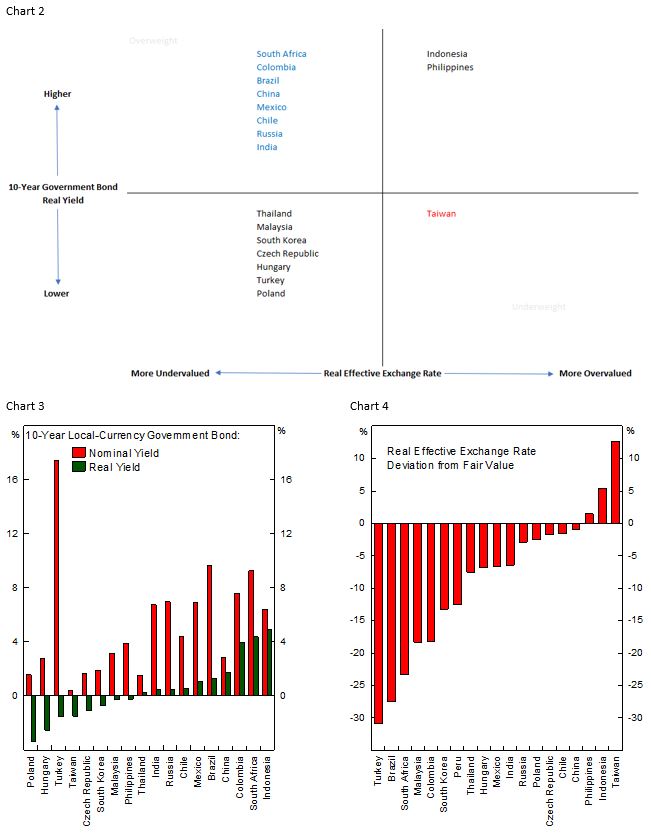

First, bonds with high real yield and cheap currency are attractive as they provide greater room for appreciation, or at least act as a downside buffer. Chart 2-4 ranks major EM countries real 10-year government bond yield and currency deviation from our fair value estimates. By this criterion, South Africa, Colombia, Brazil, Indonesia and China have the most favorable combination of high real yields and cheap currencies. The opposite holds for Taiwan and India. The increase in headline inflation in many EM countries, especially the more fragile one such as Brazil, Mexico, Russia and South Africa have reduced their real yield significantly even as nominal yield is rising – most of the increase in their headline inflation has been driven by rise in food and energy prices, lagged effect of last year’s currency depreciation and base effects, all of which is moderating.

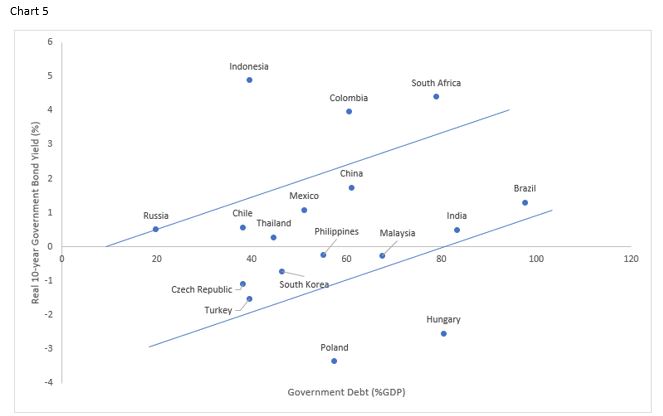

The second criterion compares government debt-to-GDP ratio with their respective real and nominal yields. Indonesia and Colombia still stand out by this metric, as both countries have manageable government debt level and interest burden (Chart 5 and 6). Another outlier is Russia, whose debt-to-GDP level and interest burden is among the lowest within EM, yet its bond yield is trading at similar level to Mexico, which has high share of foreign-currency sovereign debt, and India, whose interest burden accounts for near 30% of fiscal revenue (Chart 7). Meanwhile, India, Brazil, South Africa and Hungary rank poorly by this metric. The situation is particularly bleak in Brazil and South Africa amid their government’s inability to reform or cut its spending due to poisonous politics and weak growth. In Brazil, President Bolsonaro is mulling to extend the pandemic aid into next year, possibly to boost falling his approval rating before the presidential election in October 2022. A recent poll by IPEC shows popularity of Bolsonaro as President of the Republic dropped to 22% from 25% in February, whereas the same poll for Lula increased from 34% to 48%.

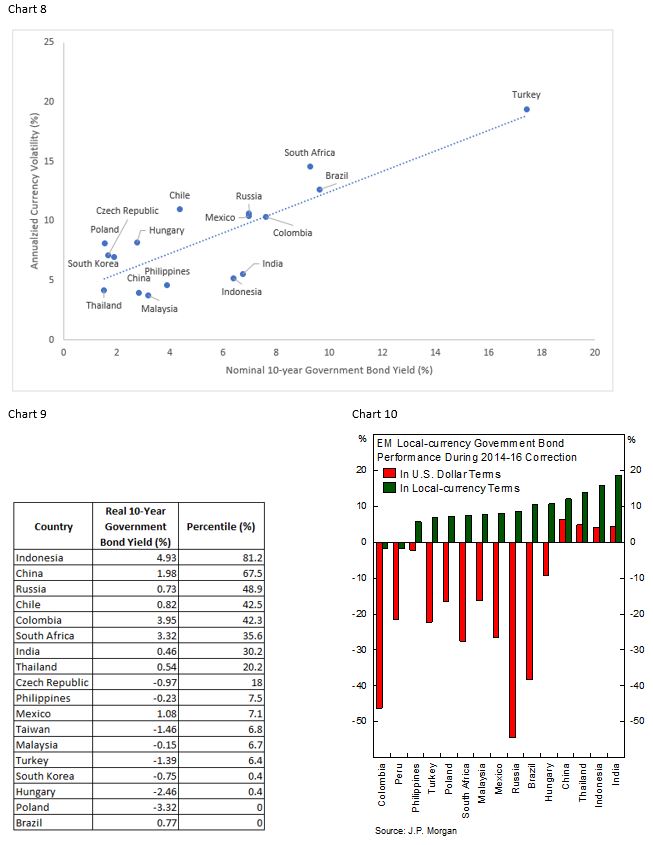

Third, comparison between bond’s nominal yield and its currency volatility helps investor gauge the reward for taking the risk of falling currency. This is particularly relevant for a country in crisis like Turkey, whose 18% nominal yield is more than offset by the fall in Turkish Lira in the past 3 years (Chart 8). By this metric, Indonesia and India ranks favorably, while South Africa and Chile are unattractive. Moreover, both Chilean bond yield and currency volatility have risen since the social unrest in 2019, and the upcoming November’s presidential election could stir another round of volatility for the country’s asset market.

The fourth criterion ranks the percentiles of EM countries’ real bond yield to gauge the expensive or cheapness-level across time. A country with high percentile offers attractive long opportunities in the hope that real yield will mean revert to its average. By this measure, Indonesia and China are the only two countries with above average percentile (Chart 9). On the contrary, Brazil and Poland’s bonds currently have record low real yield amid rising inflationary pressures.

The new fifth criterion considers the winners and losers during major market correction. Generally, fragile Latam countries suffered more than its Asian counterparts, both from larger increase in bond yield and currency depreciation (Chart 10). Investors should avoid Russian, Brazilian, Mexican, South African, Filipinos and Colombian bonds according to recent experience. However, it is important to note that during the 2014-16 correction oil price dropped by over 70%, weighing Colombian, Mexican and Russian currencies; currently oil price is trading at much higher level and is expected to stay that way at least until early next year. The situation for Russia in 2015 was also an exception, as the country’s problem was worsened by punitive U.S. sanction, and it has sanction-proof its economy since. For investors who are not restricted from holding Russian bonds, it remains one of the most attractive EM bond opportunity.

Taken together, we remain positive on some EM local currency bonds, favoring countries with higher yields and cheaper currencies, stronger external profile, and lower interest burden. Investors should overweigh local currency bonds in Indonesia, China, Colombia and Russia, and under weigh those in India, Philippines, Malaysia, Taiwan and Chile.

EM Central Banks’ Policy Divergence

After cutting policy rates to record low last year amid the pandemic, EM central banks have started to reverse their policy this year (Chart 11). Last week seen Brazilian central bank raise its policy rate by a full percentage point, following similar action by its Russian counterpart last month. With the economy recovering and inflationary pressure rising above respective countries’ target, some more fragile countries are forced to tighten. Chart 12 shows that in general, rate hike expectation for the more fragile Latam countries is much higher than EM Asia due to the region’s weaker anchor of inflation expectation and higher structural vulnerabilities. More importantly, Latam countries’ real policy rate is currently deeply negative, and the higher carry could become a tailwind for their undervalued currencies to appreciate should the dollar resume its bear market (Chart 13).

The differing drivers of inflation, growth outlook and structural vulnerability will determine the monetary policy of each country. For example, EM Asia and Central Eastern European countries could afford to stay put and let inflation rise without jeopardizing their macro stability, while more fragile countries such as Brazil, Mexico and Russia have and will continue to increase their interest rate as inflation rises.

- Rising food and energy prices could hardly be solved by demand management and increasing interest rate to curb their price growth is a futile effort. In Brazil and South Africa, for example, half of the increase in headline inflation is contributed by higher food and oil prices, which will naturally decline next year should prices stay constant. More concerning is the increase in Russian inflation, half of which is driven by generalized increase of core goods and services prices. This explains why the country’s central bank hiked rate by 225 bps this year, bringing policy rate above pre-pandemic level.

- The hike in borrowing cost and the past year’s appreciation of domestic currency are translating to a much tighter monetary condition, at a time when many EM countries are still battling with the pandemic and fiscal policy is already becoming a drag for growth (Chart 14). We should see a growth disappointment in countries that reverse their policies aggressively, such as in Brazil and South Africa (Chart 15 and 16).

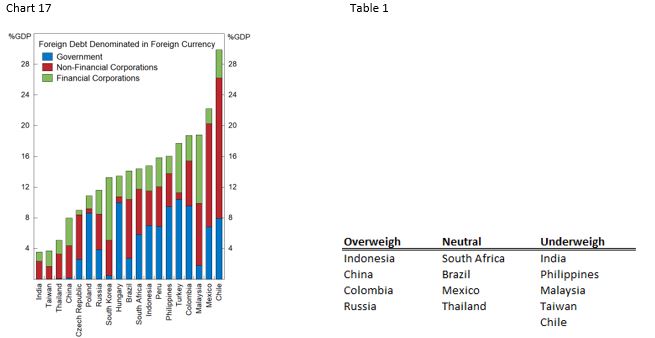

- Countries with weak structural profile and have high foreign currency liabilities could ill afford to have their currency depreciate significantly as it would jeopardize domestic macro stability (Chart 17). To prevent the spiral of currency depreciation and higher inflation, the country’s central bank has to hike policy rate and stem capital from flowing out of the country.

Table 1 shows country recommendation for our EM bond allocation. We are downgrading high-yielding bonds of Brazil, South Africa, and Mexico for now as they will suffer the most in dollar terms during risk off period – amid the combination of poor fiscal outlook and rising political risk – and opting instead for Indonesian, Colombian, and Russian bonds due these countries stronger external profile and currency stability, albeit at slightly lower yield. A correction in the commodity complex, tightening monetary policy and fiscal drag could further undermine these countries growth outlook, despite the cheap valuation of both Brazilian and South African bond and currency.

EM Bonds vs Equity Allocation

From asset allocation perspective, the outlook for EM bonds is more favorable relative to EM equity. Slowing Chinese economy, Fed’s hawkish policy and below average equity risk premium point to further downside in EM equity-to-bond ratio (Chart 18). Similar to our bond allocation tilt towards safety, our equity allocation this quarter is also positioned accordingly.

It is increasingly important for investors to be selective in harvesting EM country risk premium, as decline in a country’s bond yields could also push down equity earnings yield lower, at a time when earnings for major countries are still rebounding from the pandemic (Chart 19) and capital inflow is still strong. The case is even stronger for Russia and Colombia amid the prospect that oil price could stay high for longer due to OPEC+ agreement last month.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.