Download PDF:

For over a year, investors have been rewarded for tilting their portfolio towards risk assets on the backdrop of plentiful support for households from the government’s generous fiscal transfer that supported spending and Fed’s support on the credit market, preventing a crunch in liquidity of the debt market. The unprecedented fiscal and monetary supports have translated to one of the strongest rallies in risk assets over the past century. The U.S. currently has its stock market at record high level and corporate bond yields are near historical low, with real borrowing rate at deeply negative level. But as fiscal thrust is becoming a drag on growth and the Fed is shifting its focus from towards more hawkish policy, equity multiples and bond spread could suffer from the decline in growth rate and liquidity.

The past decade has been a boom for debtors as lower borrowing cost allows struggling firms to survive and profitable firms to take more debt while returning equity to shareholders. The strong performance of U.S. stock market has partly been bolstered by this positive feedback loop, which makes it important for investors to watch for spike in corporate yields that has reverberation for both equity multiples and earnings outlook. Historically, a correction in the equity market has almost always been preceded by stress in the bond market.

Going forward, the outlook for global risk assets will hinged on the development and interaction of three main drivers for global growth, namely Federal Reserve’s policy, strength of Chinese growth and liquidity in the financial market that ebb and flow alongside valuation in risk assets.

U.S. employment and inflation, and Fed’s Policy

We are in the camp that see inflationary pressure as temporary and is increasingly vindicated by the stable “core” inflation and abating surge in “reopening” categories such as used car and energy prices. In fact, Dallas Fed’s trimmed mean inflation measure is barely at 2% (Chart 1). On top of the inflation outlook, U.S. labor market likely stay below potential at least until 2025, according to our projection (Chart 2).

This means the current market expectation and Fed’s guidance that the first rate hike will take some time in 2023 are simply too hawkish. Once it is clear to the market that deflation remains the trend of the decade and labor market slack will take years to tighten, bond yields will continue its downward structural trend and the Fed backing away from its hawkish stance. However, tapering Fed’s monthly bond purchase is justified as the credit market no longer needs liquidity support with repo rates flirting below zero in May. This could pop the bubbly credit market and trigger a shakeout in IG and HY spread from its record low level.

If our forecast on the labor market and inflation is right, then 10-year Treasury yield could come down as low as 1% before the curve start to steepen again. The dollar, which currently is still some 10-20% overvalued, could continue its decline. Risk assets should do well in this environment, with commodity and precious metal potentially making new highs. A bleaker environment lies when the Fed starts raising policy rate, which is years down the road. The marked increase in corporate leverage means that as Treasury yields rise, corporate spread most likely will widen too, especially for high yields. As liquidity continue to tighten and credit market shows signs of weakness, the Fed will eventually pause and the cycle turn down, a precursor for bear market in equities.

China’s Growth and Policy Tilt

In China, policymakers’ focus is still tilted towards cleaning up bad credit in the system and reforming its social construct, although easing efforts start to materialize as highlighted by recent cut in banks’ reserve requirement ratio and promise to accelerate local-government bond issuance in the second half this year. For the next 3-6 months we see above 50% chance for credit incidence in the domestic corporate bond market as growth continue to slow, and further volatility related to Huarong and Evergrande’s potential default could not be ruled out, although systemic fallout should be avoided.

More importantly, the crackdown in various sector of the economy – finance, ride sharing and other start up, education, and more recently gaming – has shaken the confidence of investors in China’s protection of shareholders right. Unlike in the U.S., where companies could rely on independent court and fight government policies, Chinese firms are at the mercy of regulators without any chance to fight back. If anything, Chinese stocks’ multiple should be de-rated as risk premium rise and its margin and terminal growth rate cut due to limitation on become a monopoly in certain industry, not to mention vicious competition for the low capital industry such as tech and software.

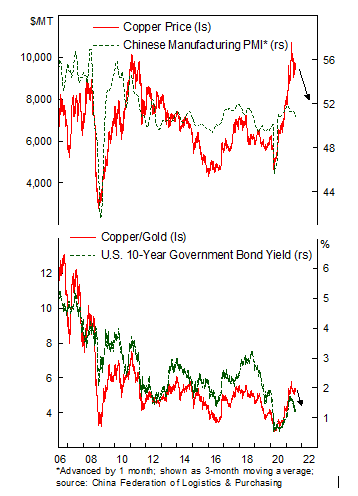

From cyclical perspective, we think Chinese growth is still on the early phase of the growth slowdown and a larger correction in either stocks or commodities will have to occur first before policymakers’ easing focus intensifies (Chart 3). For the past quarter we have turned defensive and trading copper from the short side, although bull staying power remains powerful in the market.

Global Liquidity and Valuation

With tapering of bond purchase in the mind of Fed’s officials and economic rebound going strong, the era of slosh excess liquidity has peaked, and monetary condition should tighten going forward (Chart 4). This will have several ramifications down the road. First, banks’ deposit – which have grown 25% since the pandemic – should continue to grow at slower pace closer in line with GDP growth while credit should pick up, leaving less money in the system to go to the financial market, and ease banks’ capital requirement. Second, decline in excess savings amid the withdrawal of fiscal stimulus and pick up in the real economy should push equity valuation down from frothy level (Chart 5). Europe should do better amid the relatively dovish ECB policy and weaker member states’ growth outlook, although the central bank is likely to taper in the second half of this year as well.

Meanwhile, in China, money growth has been relatively tight relative to credit since the crackdown at the end of 2014, one of many reasons Chinese growth number has continue to come down and deflationary pressure becoming the norm. With the government taking a heavy-handed intervention in the country’s capital market and private companies, the risk for Chinese stocks and economy remains on the downside.

Conclusion

Taken together, an unjustified hawkish tilt by the Fed, deepening growth slump in China, and tightening liquidity in the asset market all potentially cause rally in risk assets to reverse – especially in the high-flying U.S. equity index and commodities (Table 1). A dovish pivot from the Fed and greater reflationary effort in China would fuel the next leg higher but is unlikely at least until the end of the year when the downturn becomes clear.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.