Download PDF:

Global stocks continue to experience a dichotomy in recent months amid unequal economic recovery in the developed and emerging world. With vaccination rate crossing above 50% of total population and covid-19 number goes into the rear-view mirror in the rich world, both manufacturing and service sector has rebounded strongly amid last year’s pent-up demand being released. The euphoric mood in the economy is also reflected in the valuation multiples of many DM equities, in which the majority is now above their historical 70th percentile. The violent rally in global equities have brought valuations out of the cheap territory but investors should expect earnings to continue to rebound and drive stocks higher. However, we are turning bearish on U.S. stocks in the short term due to it being among the most expensive bourse in the world and looming slowdown in U.S. growth outlook, which weighed U.S. bond yield of late (more on this below).

Meanwhile, EM stocks still offer valuation advantage relative to its DM counterpart but with few caveats. First, the pandemic situation in EM countries have only worsened in the past quarter amid the spread of the Delta variant and low vaccination rate. Countries that in 2020 were deemed to have excellent response to the pandemic has lagged in procuring vaccines and are now facing surge in cases, which is a headwind for their domestic demand and assets. We are seeing that covid-19 will continue to weigh countries like Indonesia and South Africa at least in the coming 6 months as these countries will neither be able to reach herd immunity nor curb the virus’ spread anytime soon. Second, Chinese cycle is turning down again, and recent reserve requirement ratio cut is unlikely to help the downturn in the second half of this year. Taken together, this means the risk for stocks have risen significantly and investors should pare down aggressive bets on global equity.

In terms of asset allocation, we are bond bullish, neutral on equity, and expect the dollar to strengthen against major currencies in the short term.

Bonds. Treasury yields continue to shift lower as the market sniff out the peak in the business cycle, slowdown in China and the U.S. In last month piece we lay out the case to turn defensive on global risk assets and we continue to hold this stance this month. S&P 500 and copper both have much more room to fall to correct the overbought condition and lofty valuation in the former. Meanwhile, the later is weight by marginal downshift in Chinese economy – a major global copper consumer.

Equities. Global equities are now expensive, although earnings growth may continue to be robust in the second half this year. With the Fed and ECB start to talk about tapering liquidity in the market, our hunch is that the market will experience rounds of volatility. This, combined with the slowdown in growth outlook and lofty valuation could trigger an above 10% correction in global equities and commodities.

Currencies. The dollar is likely to strengthen amid Fed’s relative hawkishness relative to ECB and BOJ, but its appreciation is more likely against major currencies instead of the still cheap EM FX for few reasons. First, the Fed is likely to stay put for the next 2 years while EM central banks have started raising policy rate aggressively since earlier this year, providing a decent yield pick up from the interest rate differential. Second, valuation of EM currencies remains cheap, unlike in 2013 when most currencies were overvalued against the dollar. Lastly, we are betting that inflationary pressure in EM to stay under control and that may result in some EM central bank end up being too hawkish, a tailwind to the currency at the expense of domestic growth.

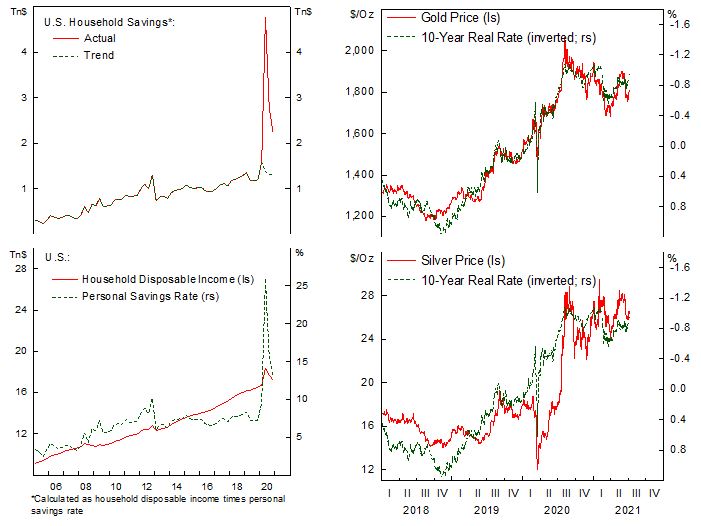

Will Excess Savings Be Spent in the U.S.?

The massive fiscal stimulus and unemployment insurance in the U.S. last year has helped households to coped with the lockdown restrictions and associated loss in income. Surveys show that most of the government transfers have been saved and used to pay down consumer debt. According to our estimate, U.S. household has $5.8 Tn (27% of GDP) in excess savings arising from last year’s fiscal support, which may partially be spent in the second half this year. We are skeptical as to whether large amount of the excess savings will be spent, as historically savings rate would only fall slightly to pre-crisis level but not nearly as much as to counter the rise in excess savings during the crisis period.

As fiscal thrust will turn negative this quarter, aggregate demand in the U.S. economy likely falls as private sector investment unable to completely offset the decline in government spending and compound the excess savings problem. From investment perspective, this means real yield is likely to stay low without a policy shift from the Fed – supporting precious metal prices. However, the return/risk profile has deteriorated somewhat for precious metals, and we shifted our allocation on gold and silver into neutral since last month as the risk of upturn for the dollar rises.

EM Currencies: Will Rising EM Policy Rate Counter Fed’s Hawkishness?

- Periods of Fed’s hawkish tilt has historically boded poorly for EM currencies. A significant rise in real yield in the U.S. likely curtail investors’ optimism on risk assets and increase the attractiveness of U.S. fixed income, resulting in capital outflow from EM countries.

- But EM FX is now much cheaper compared to 2013 episode while the dollar is still expensive, meaning that there is still plenty of runway for the former to rally. On the downside, idiosyncratic factors could weigh respective countries’ currency, such as political factors seen in Latam of late and policy blunder in Turkey. We expect fundamental and economic drivers to eventually dominate, although investors should be wary and monitor the possibility of political problem turning into economic issue.

- A growth slowdown coming from U.S. and China could further delay the timing of Fed’s rate hike, while EM countries have been normalizing its policy rate earlier and at a faster pace. A peaking out in U.S. inflation numbers in the coming months will shift the Fed back into dovish stance and propel EM currencies higher.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.