Download PDF:

- Developed World: Earnings and Valuation Outlook

Earnings for most sector has recovered to pre-pandemic level, with health care and IT sector posting strong earnings in Q1. Growth expectations for both sectors, and materials, are strong and valuation is not demanding for the later. We believe that we are entering a structural bull market in commodities, as discussed in our copper report earlier this year. Years of underinvestment has resulted in supply rigidity that does not catch up to increasing demand from strong cyclical pick up and trend in the shift towards green energy and infrastructure. Despite the bullish case on commodities, however, we remain more bearish on traditional energy sector as more and more countries are curbing its fossil fuel emission and electric vehicle’s market share are expected to rise significantly in 10 years, potentially reaching above 50% of sales.

We think valuation in the developed world – particularly in the U.S. – is lofty and investors are wise to raise some cash holdings as U.S. growth momentum peaked and downside risks are increasingly priced in, from geopolitics to a more hawkish monetary policy. As expectations for earnings improvement are topping out, we believe the market will correct from current level (SPX at 4200) in the coming months. Sector-wise we favor financials, materials, consumer staples, and industrials.

Investors should also look to EM for value, as we have advocated for years, as valuation and earnings outlook are very bullish for resource-heavy countries such as Brazil, South Africa, Chile, and Peru. Although geopolitical risk in this country is high, as demonstrated by the current bloody protest in Colombia, 2019 Chile riot, and recent left-tilt in Peru, these countries’ valuation is attractive and stock prices should continue its rise – Brazilian equity has done well despite erratic policies from Bolsonaro’s government on fiscal policy and covid-19 response and Mexican equity has rallied strongly despite a nonmarket friendly policy in the energy sector.

Investors should also look to EM for value, as we have advocated for years, as valuation and earnings outlook are very bullish for resource-heavy countries such as Brazil, South Africa, Chile, and Peru. Although geopolitical risk in this country is high, as demonstrated by the current bloody protest in Colombia, 2019 Chile riot, and recent left-tilt in Peru, these countries’ valuation is attractive and stock prices should continue its rise – Brazilian equity has done well despite erratic policies from Bolsonaro’s government on fiscal policy and covid-19 response and Mexican equity has rallied strongly despite a nonmarket friendly policy in the energy sector.

Silver: Back From The Dead?

The past two weeks saw silver prices moving higher again and the technical picture looks bullish. We have a large long position on the precious metal since Summer last year, when silver price was surging to $30/Oz before tumbling down 15% in days and continue to play the bullish side since.

- The dollar should resume its downtrend due to stronger economic recovery in Eurozone and larger current account and fiscal deficit relative to other DM countries. After last year’s slide in the DXY index the dollar remains overvalued against G7 currency basket. A weak dollar has always been bullish for commodities and precious metals.

- Long-term Treasury yields are peaking out as Fed reiterate its dovish stance and brush off the potential for permanently rising inflation amid strong U.S. domestic recovery and large fiscal spending planned by the Biden’s administration. The market is still pricing significantly more hawkish projection of Fed policy rate hike and we believe 10-year yield will slide towards 1.2-1.4% in the coming months. This, combined with 10-year inflation breakeven rate at 2.5%, should propel silver prices to above $35/Oz.

- Silver is also making a bullish configuration on the technical side with potential to test the $50/Oz level.

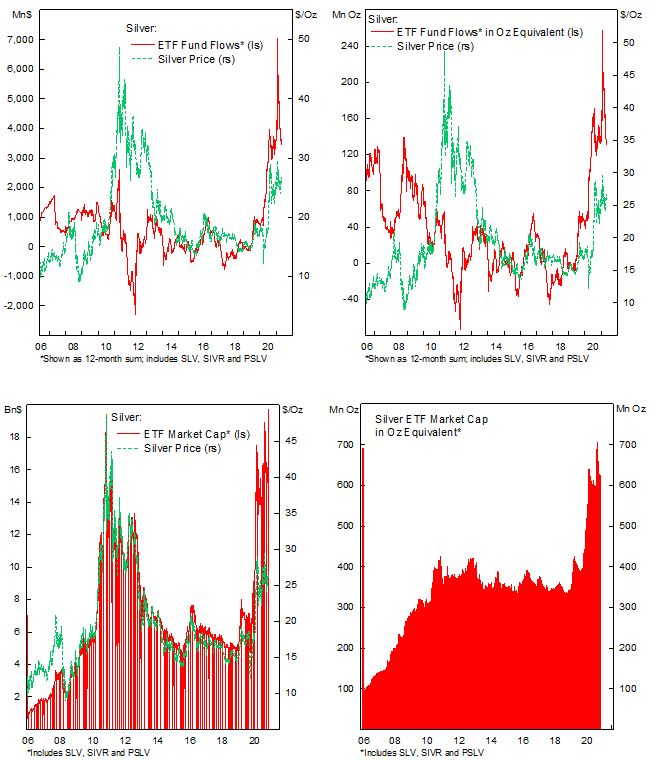

- Previous bullish position on precious metals have been unwound and inflows to gold and silver ETFs should resume and drive prices higher. Fund flows have been strong since last year and we suspect further demand from physically backed silver ETF will drive prices higher. For the past decade silver supply has been flat around 1000 Mn Ounces and the two years alone demand from silver ETF is above 300 Mn Oz. It is almost impossible to source over 15% of world’s silver supply annually without prices moving significantly higher. Silver ETF market cap is still relatively small, with the top 3 ETF amounting to $17 Bn, and sizeable inflow will inevitably cause silver price to spike higher.

EM Inflation: Transitory or Permanent?

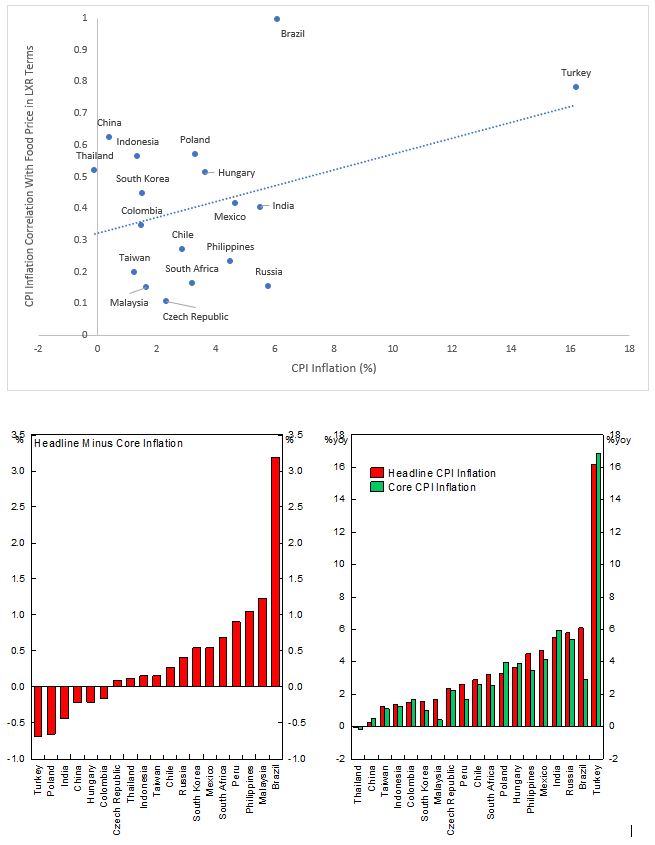

Inflation across the world and in EM countries have risen back to pre-pandemic level amid favorable base effect and cost-push inflation from rising commodity prices. The more fragile EM countries – Russia, Brazil, Mexico, Turkey – inflation has spike higher in the past two months as global food and oil prices are rising. It is reasonable to ask whether EM countries in general will have an inflation problem as economic recovery accelerates, or whether the current uptick in inflation is temporary. We are betting on the later due to few reasons:

- The rise in inflation has been fueled by rising food and oil prices instead of broad-based core goods and services. Last year’s oil price slump drives down transport cost for EM countries, which also dragged down headline inflation (see charts on Brazil and India). As economic activity normalizes and oil prices recovers, transport price inflation suffers this year from abnormally low base effects, which will moderate in the coming months.

- On the issue of rising food price, it is important to note that agricultural supply-demand is rather elastic, and recent surge in prices should incentivize farmers to switch into higher priced crops and bring prices lower in the next harvesting season. The current rise in gasoline and food prices, however, will hurt the poor in least developed countries most and may result in domestic political volatility – as it did in the Arab Spring of 2011 that started in Tunisia with complain of high bread prices.

- The effect of currency movement to domestic price inflation has lessened for most countries, even for Turkey (see chart). Contrary to previous crisis experience, last year’s dramatic currency depreciation was followed by lower inflationary pressure across EM. Although the effect of currency movement is becoming less important in determining domestic prices, recent strength and stability in EM currencies, combined with monetary tightening in few countries, should cap inflation from rising much higher.

The risk of Inflation Flare Up

Although we believe that inflation will remain muted in most EM countries, a flare up in inflation in select countries could not be completely ruled out. It is important to note that different countries have varying weight of consumption basket with poorer countries having greater weight for food and transport prices, which translates to higher headline inflation figure when food and oil prices are rising.

Despite some EM countries being either a large exporter of agricultures, oil products, or both, rising global prices also translate to higher domestic inflation. For example, food and oil prices inflation account for over half of the headline inflation figure in Brazil and Russia. However, unless prices continue to rise, inflation should start to moderate in the coming months.

Brazil and Russia, on top of Turkey, have a historically high correlation between domestic inflation and commodity prices and currency movement, and headline inflation has indeed risen in the past quarters for these countries. The beta or sensitivity has decreased significantly in the past two decades, but large dependence of these countries’ economy on commodity exports and drastic depreciation of their currency in the past year mean the risk of overheating in their domestic economy should not be overlooked.

From a cyclical perspective, both Brazilian and Russian economy has recovered from the slump and their currencies are cheap, both of which normally coincide with rising inflationary pressure. The risk is further heightened in Brazil due to its ultra-easy fiscal and monetary support last year, which has helped domestic consumption and activity to recover strongly.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.