Download PDF:

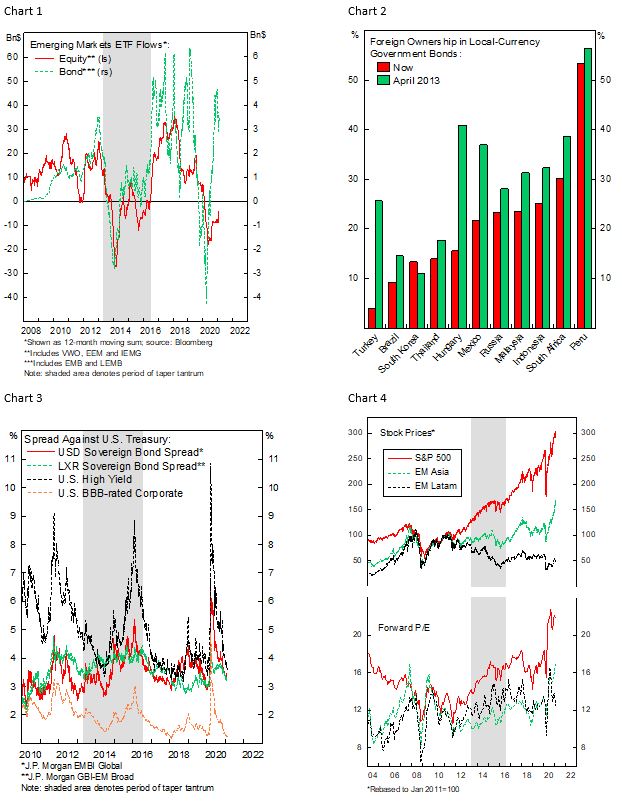

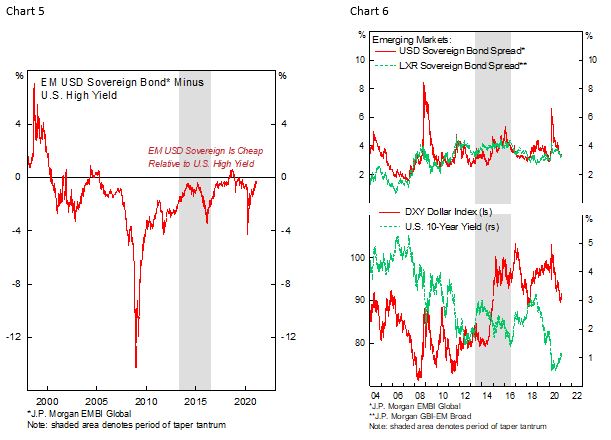

Potential for Sizable Portfolio Outflow is Limited. The period before 2013 Taper Tantrum was marked by strong capital flow into EM assets, in contrast to current situation where flow into EM bonds and equities are only beginning to recover (Chart 1). More importantly foreign ownership of EM bonds, especially for the more fragile EM countries, are now much lower than pre-taper tantrum (Chart 2), further limiting the pressure of outflow from local bond market and currency.

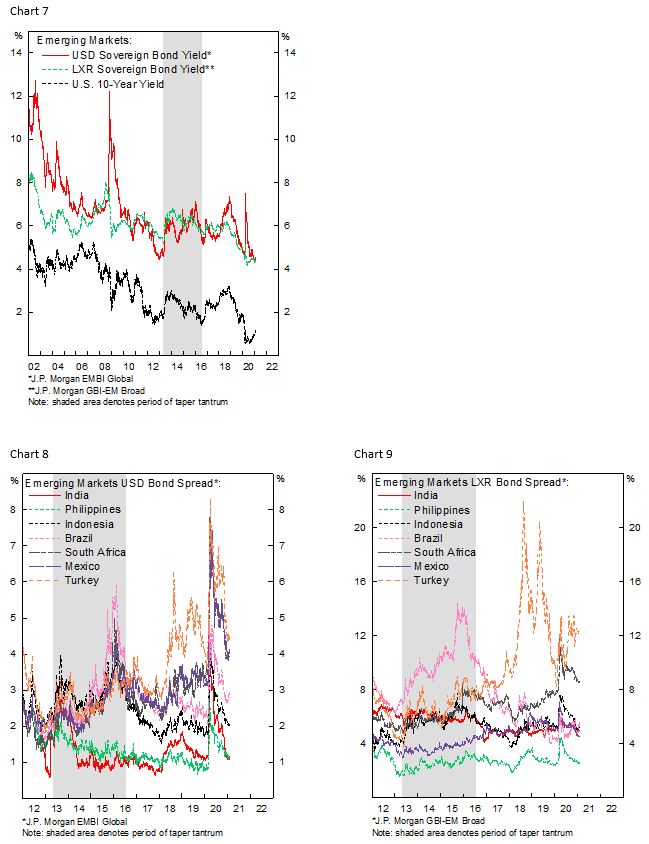

Yield Pick-Up for EM Bonds is Still Attractive. Attractive valuation for U.S. bonds and equity manage to pull capital back to domestic assets in 2013. However, Chart 3 and 4 show the situation today is marked by record-low U.S. yield and extreme valuation in U.S. equity; currently IG and HY bond are trading at only 1.2% and 3.6% spread relative to Treasury, compared to 3.3% and 3.4% for local-currency and USD sovereign EM bonds – in normal circumstances USD sovereign bond should be trading at a significantly lower spread relative to high-yield corporate market due to its higher credit rating (Chart 5).

There Are Little Signs of Complacency. During the taper tantrum, USD-denominated EM bonds suffered the most while LXR-denominated EM bond spread was relatively flat (Chart 6), as the index is dominated by China and the historical incidence of default of local-currency bond is low (Table 1). Moreover, capital flight was mostly focused on fragile countries with twin deficits where spread was as low as 2% – a sign of complacency as investors searches for yield – contrary to current situation where yields are widely dispersed according to respective country’s outlook (Chart 8 and 9).

A scare in the market is an opportunity to further accumulate EM bonds, as the Fed is not likely to hike rates anytime soon and EM bonds is still trading cheap relative to U.S. IG and HY domestic bond market. However, we noted that downside risk remains high for high-profile countries such as Brazil and South Africa, whose fiscal outlooks are bleak and both dollar and local-currency bond spread has already compressed significantly of late. Investors should be cautious on Latam bonds and Asian equities but maintain overweigh on Latam equity and Asian bonds, as a “taper tantrum” is likely to occur alongside strong global growth and commodity demand and a flight to safety should benefit low-yielding EM Asian bonds relative to its Latam counterpart.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.