Download PDF:

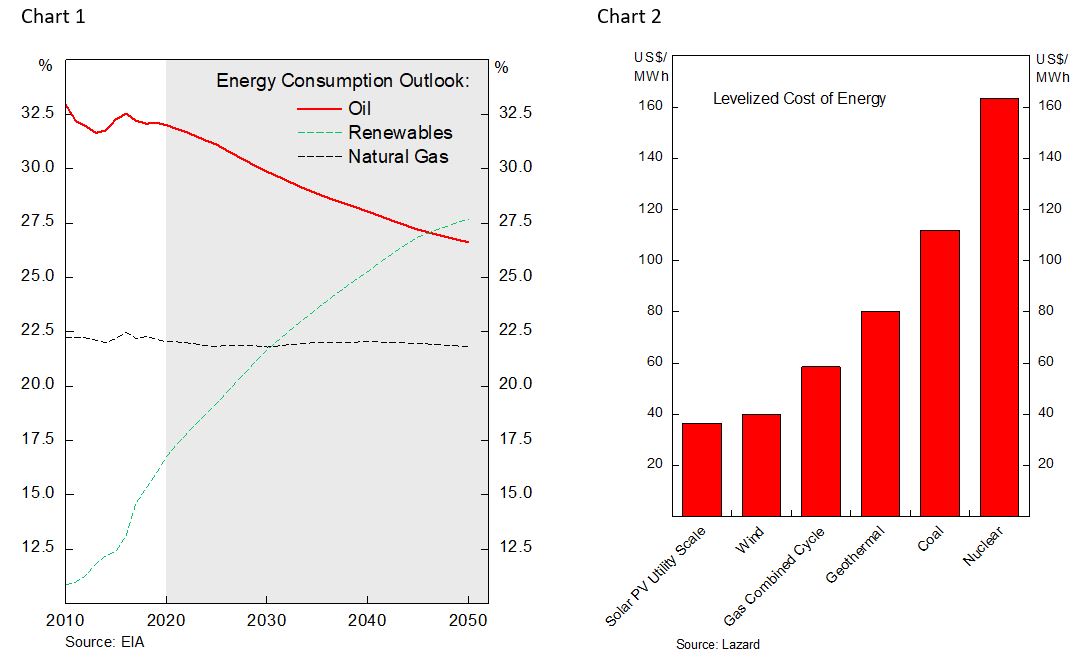

The year 2020 has seen major economies in the world affirming their commitment to limiting the increase of global average temperature to 2 degree Celsius above pre-industrial level, with a more ambitious target of 1.5 degree, as had been agreed under Paris Climate Agreement. EU and Japan would strive for a net zero target by 2050, while China is aiming for 2060. Achieving all this ambitious target requires increasing energy efficiency, decarbonization of the power sector, switching to low or zero-carbon fuels, and utilization of carbon capture technology, trends which have already started this past decade and will only accelerate (Chart 1). More importantly, all these shifts increasingly make sense from a financial point of view. In the past decade alone, energy cost from solar PV has declined almost 80% and onshore wind by 25%. Currently, levelized cost of energy – considering the total cost of building the facility and the energy produced during its lifetime – for solar PV and onshore wind power generation is lower than traditional source of power (Chart 2).

The overhaul of traditional energy infrastructure into a renewable one bodes well for several base metals, such as copper, nickel, lithium, and silver that are major components of EV’s battery, wind turbine and solar panels. Demand for refined copper is set to doubled in the next two decades, driven by increasing copper intensity as developing economies grow, electrification of vehicle, and demand from renewable energy. Meanwhile, several headwinds exist that could constrain the growth in production in the coming decades.

The Demand Side

- About half of copper consumption today is used for building construction, whose demand will continue to increase as developing countries are getting richer and its population rise. Long-term annual growth demand of copper is relatively stable at 2.8%, fluctuating alongside world’s real GDP growth (Chart 3). Marginal copper demand for infrastructure building will still be driven by China, which its imports alone account for over 20% of refined copper usage, and increasingly by other emerging countries.

- World’s transition to green energy requires significantly more metals to produce electricity, with wind turbine and solar panel require 4-6 times the amount of copper to produce each MW of electricity. EIA projected that wind and solar energy will account for above 30% of global electricity generation by 2050 (Chart 4), which potentially add 5-6 Mn Tonnes of copper demand.

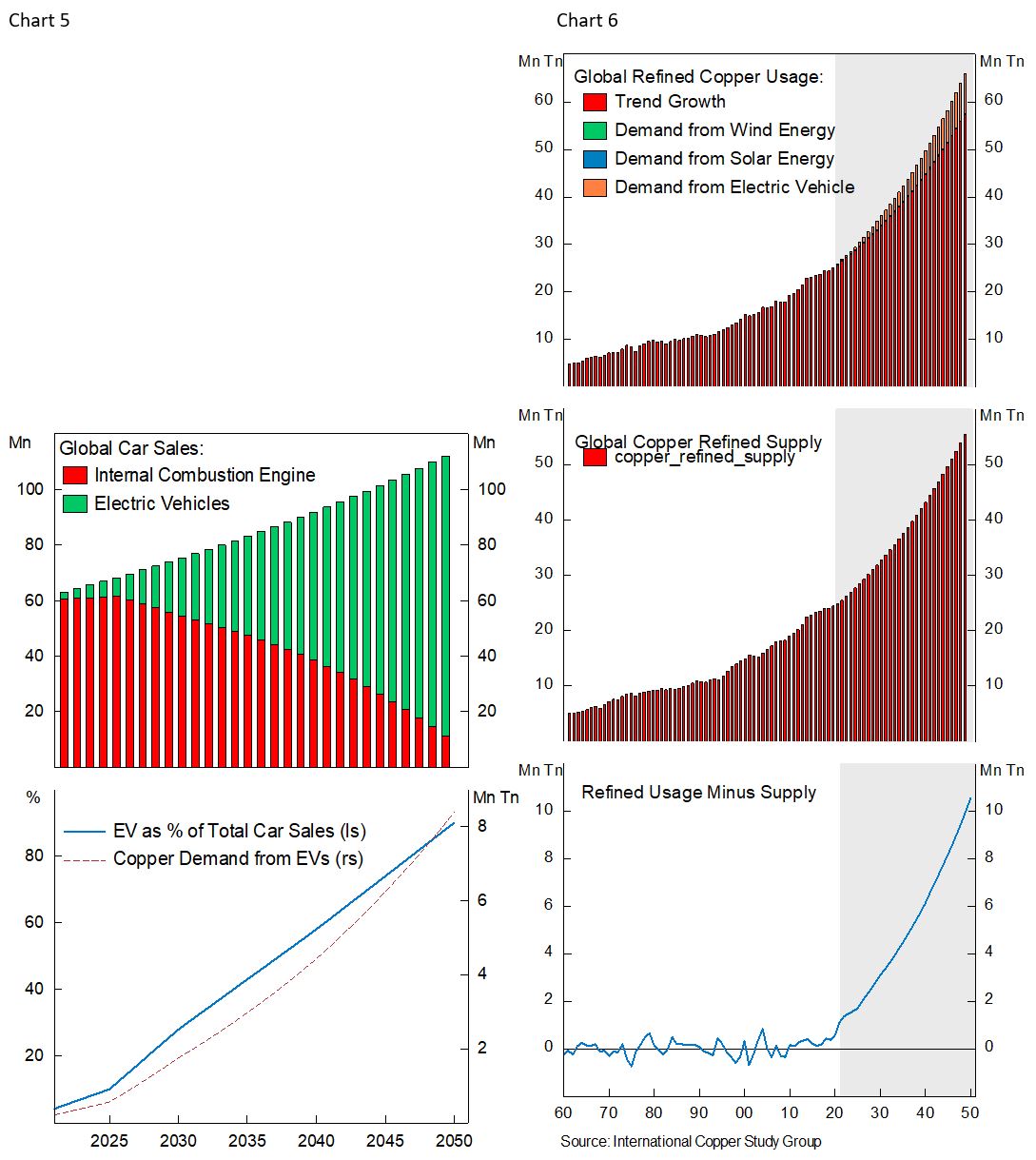

- The largest new demand for copper will come from the shift of internal combustion engine to electric vehicle, the later requiring 83 Kg of copper per vehicle vs 23 Kg for ICE. EV today accounts for only 2.3% of total vehicle production, a figure that will rise to close to 100% by the middle of the century (Chart 5). This adds 2 million tonnes additional demand of copper annually by 2030 and increase gradually to 8 million tonnes by 2050, without even accounting for the infrastructure required to support EV’s charging station and electricity distribution.

- Tallying the numbers above, refined copper demand will likely triple in 30 years time, far outpacing its historical growth rate since 1950s. Even without accounting for several headwinds facing copper supply and assuming historical growth rate of supply going forward, deficit of the base metal is a very likely scenario (Chart 6).

The Supply Side

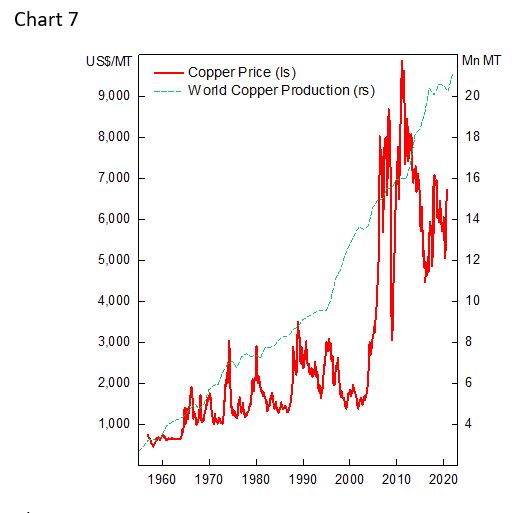

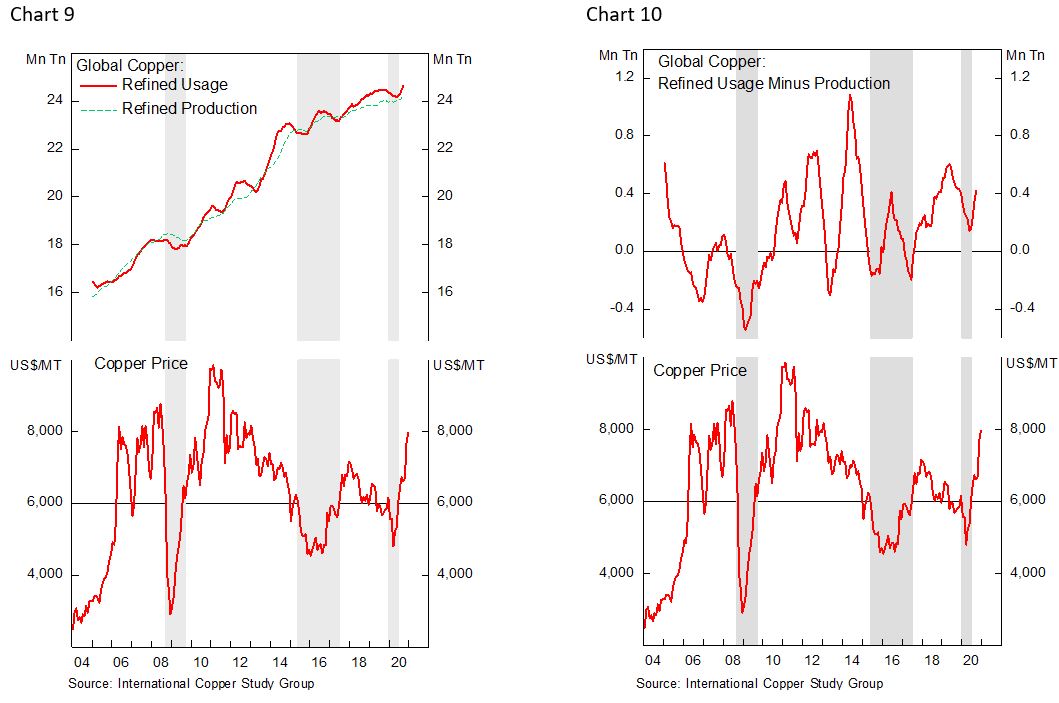

- Unlike oil, the technological revolution in extracting copper from the ground has not gone through a significant breakthrough in the past decades, which has seen increasing amount of copper has to be mined at an increasing cost (Chart 7 and 8). Production cost of copper varies between $3-6/Kg and historically we have seen copper refined supply to stop growing or even fell whenever price dipped below $6000/Ton, which have forced miners to curtail production, such as the period between 2014 and 2017 (Chart 9 and 10). Moreover, miners often mine for higher-grade ore in the beginning of the stage and go through lower grade in the later stage of production, meaning that it is more difficult and expensive to sustain production as lower quality ore being mined. All these translate to higher copper demand will only be supplied at increasingly higher prices.

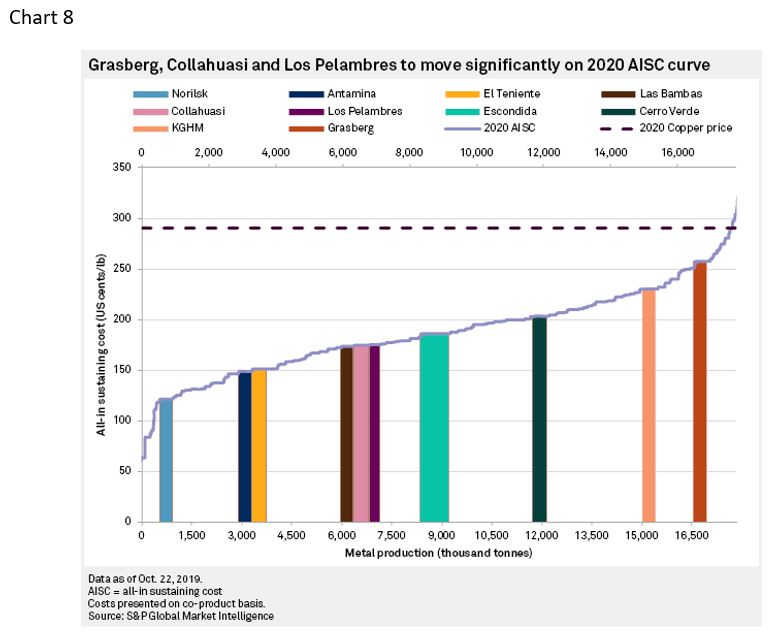

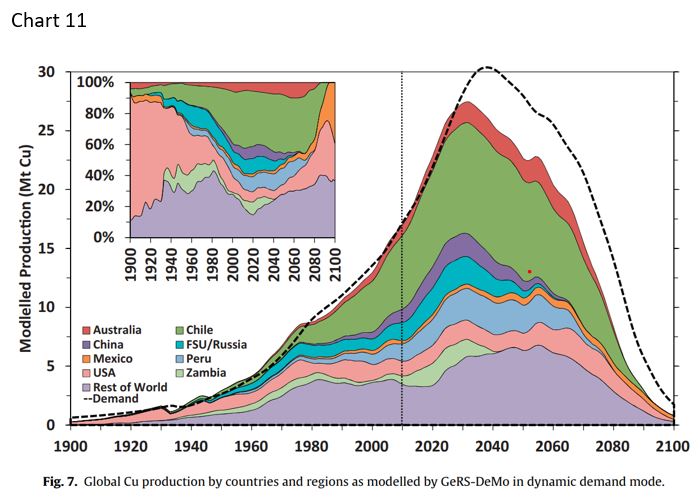

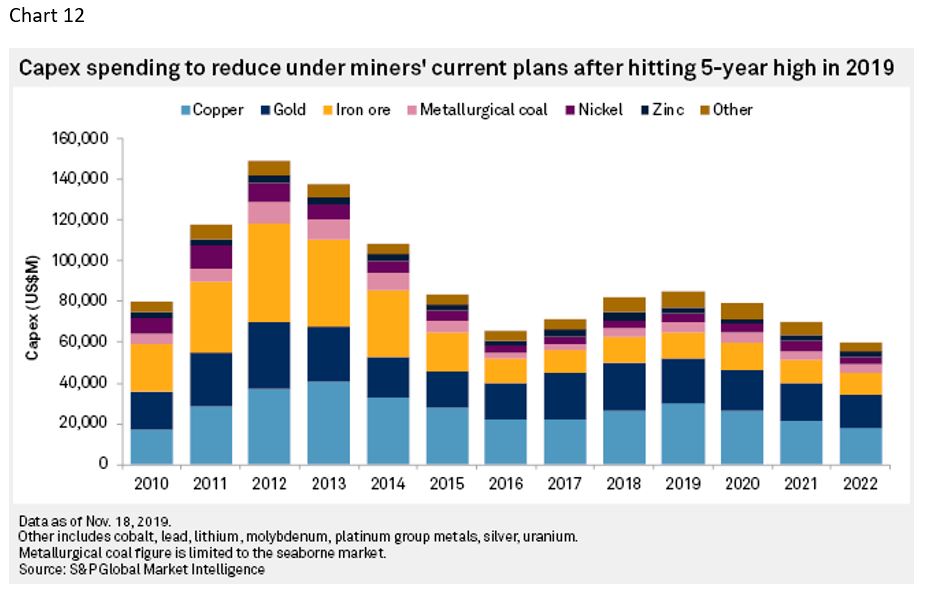

- Lack of new exploration and major discoveries also put a lid on miner’s ability to expand production. Based on copper grade, a study concludes that global copper production will likely peaks sometime in 2030, bar any major discoveries, putting a strain on the ability to ramp up production significantly to meet supply (Chart 11). Capital spending among miners has been low for years, and the decrease has been dramatic for iron ore exploration, which has seen its price surging over 70% in 2020; a similar case for copper could not be ruled out (Chart 12). Meanwhile, global metal inventories, including copper, are near decade’s low, which should provide a tailwind for prices to go higher (Chart 13).

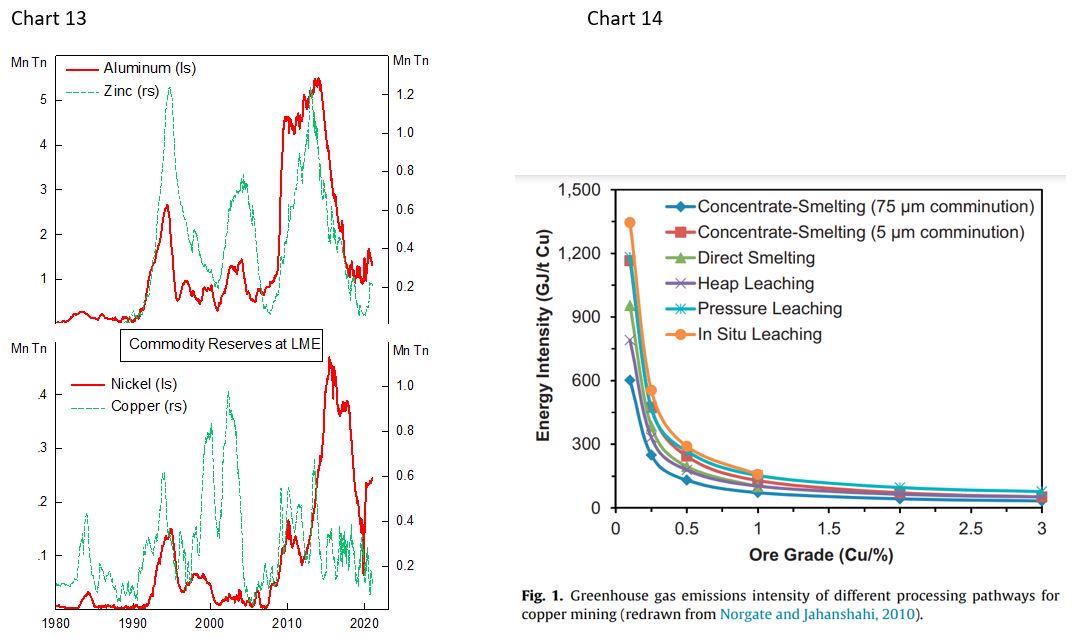

- Miners are also increasingly facing tightening environmental standard, and few have activities in geopolitically unstable countries. For instance, lower grade ore, which tend to be found in a larger mine requires higher water and energy consumption for operation and is associated with higher environmental cost (Chart 14). A global push towards limiting emissions could mean higher operating cost that is passed over to prices. In addition, the past few years have seen labor strike in Chile and Peru demanding higher pay that could further add to production cost.

Investment Implication

- Higher copper price and structural bull market for the base metal is likely this decade. Investors should overweigh the base metal commodity complex and emerging markets in a strategic allocation as a hedge to the inflation risk coming from higher commodity prices and potentially weaker dollar (Chart 15).

- Countries with large copper production and reserves such as Chile and Peru will likely enjoy periods of high growth. This could potentially allow the two countries to escape middle-income trap through a boost in savings and investments. Increasing regional conflict in Latin America and few African countries such as Congo is also likely as China, Europe and U.S. secures their supply of the metal.

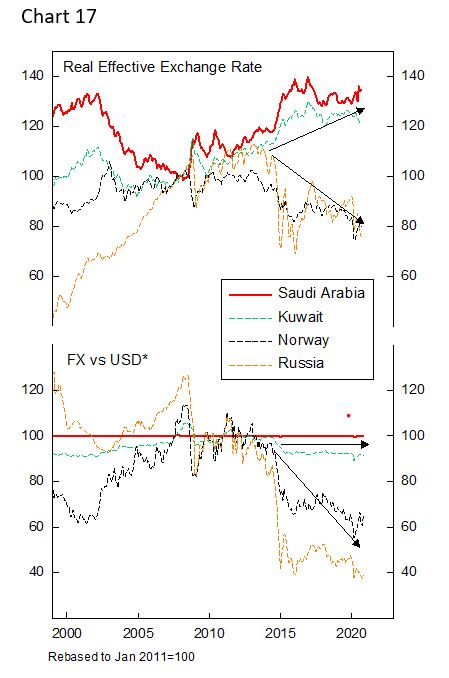

- Oil producer countries will suffer from lower equilibrium oil price as demand flattened out and more countries are shifting their power generation toward green energy (Chart 16). Price war between OPEC, Russia and the U.S. will become more often as each country tries to maximize the present value of its oil reserves. This means that currency peg in Gulf countries, such as Saudi Arabia and Kuwait, are unsustainable and will have to be devalued (Chart 17).

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.