Download PDF:

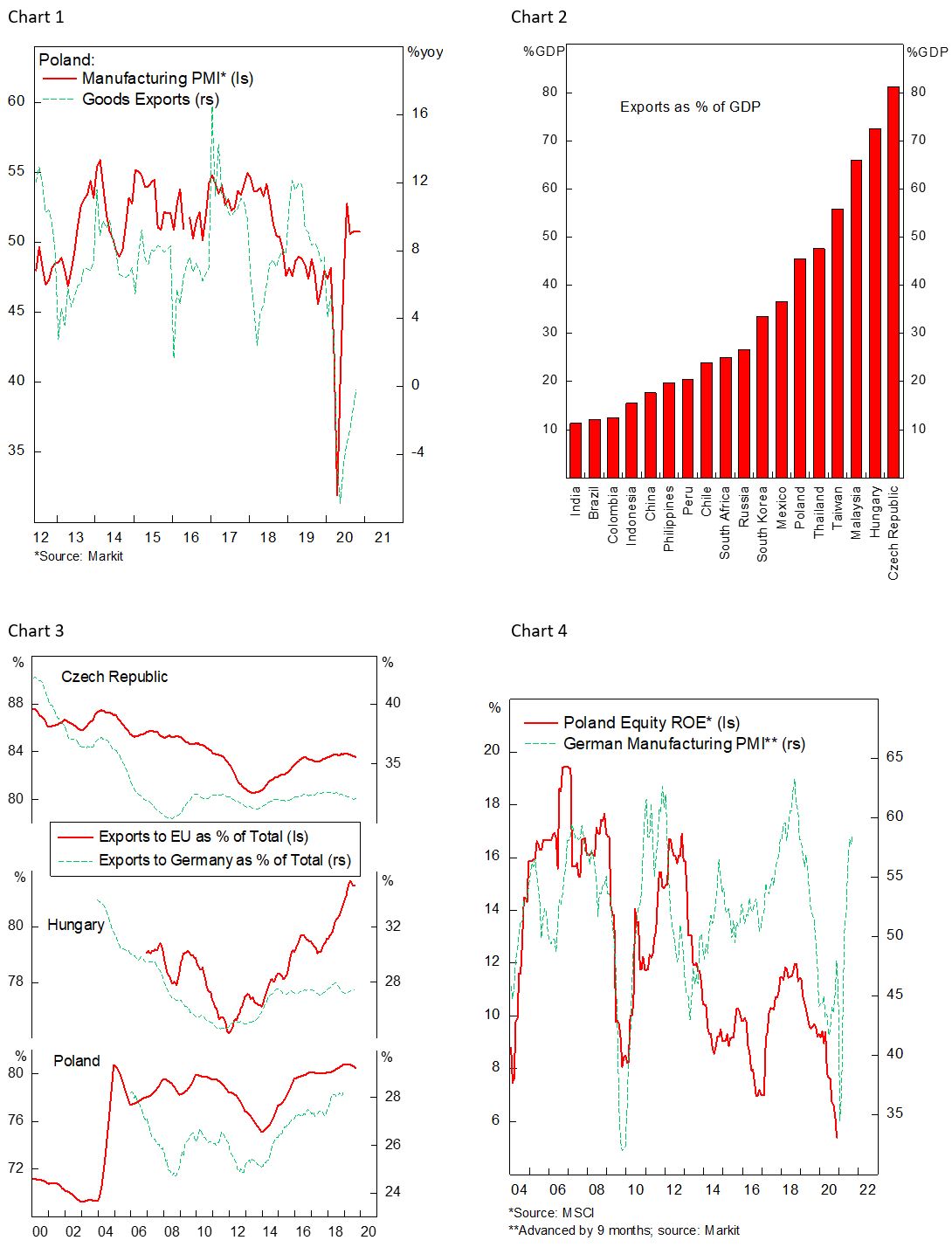

Poland

- Polish manufacturing sector and exports have both staged a V-shaped recovery despite the reintroduction of a strict lockdown across major European countries (Chart 1). As an open economy that is highly integrated with European manufacturing sector Poland has benefited from the sharp recovery of German manufacturing (Chart 2-4), which points to a much higher profitability for the country’s equity market. Moreover, new daily confirmed Covid-19 cases in Poland has come down significantly and cases across other European countries are showing signs of peaking, which will aid the recovery of its lagging service sector and retail consumption.

- The approval of EU Multiannual Financial Framework (MFF) and recovery fund (NexGenerationEU) last month, despite earlier feud with EU related to rule of law regulation, is a very good news for Poland. The EU 2021-27 budget, which includes EUR 1.074 Tn under MFF and EUR 750 bn under NexGenerationEU allocates a sizable EUR 75 billion, or 20% of EU total Cohesion Policy budget, to Poland due to the country’s less-developed region, far above the allocation to Italy and Spain. In total, this will provide a 14% of GDP boost to Polish economy over the next seven years (Chart 5). Separately, the European Commission last month approved EUR 2.9 billion of government aid to support Polish Small and Medium Enterprise, which should further boost business confidence and aid the economic rebound.

- Subsequent to years of underperformance, Polish Equity is currently trading at only 1.1 x book value and 12.7x forward earnings, the later based on a trough earnings (Chart 6). Low yields environment has weighed European banks badly over the past decade, but recent push for a larger fiscal support among European countries, unity for Covid recovery fund, and a cyclical upturn could all boost the performance of value relative to growth stocks and drive the outperformance of Polish equity.

Peru

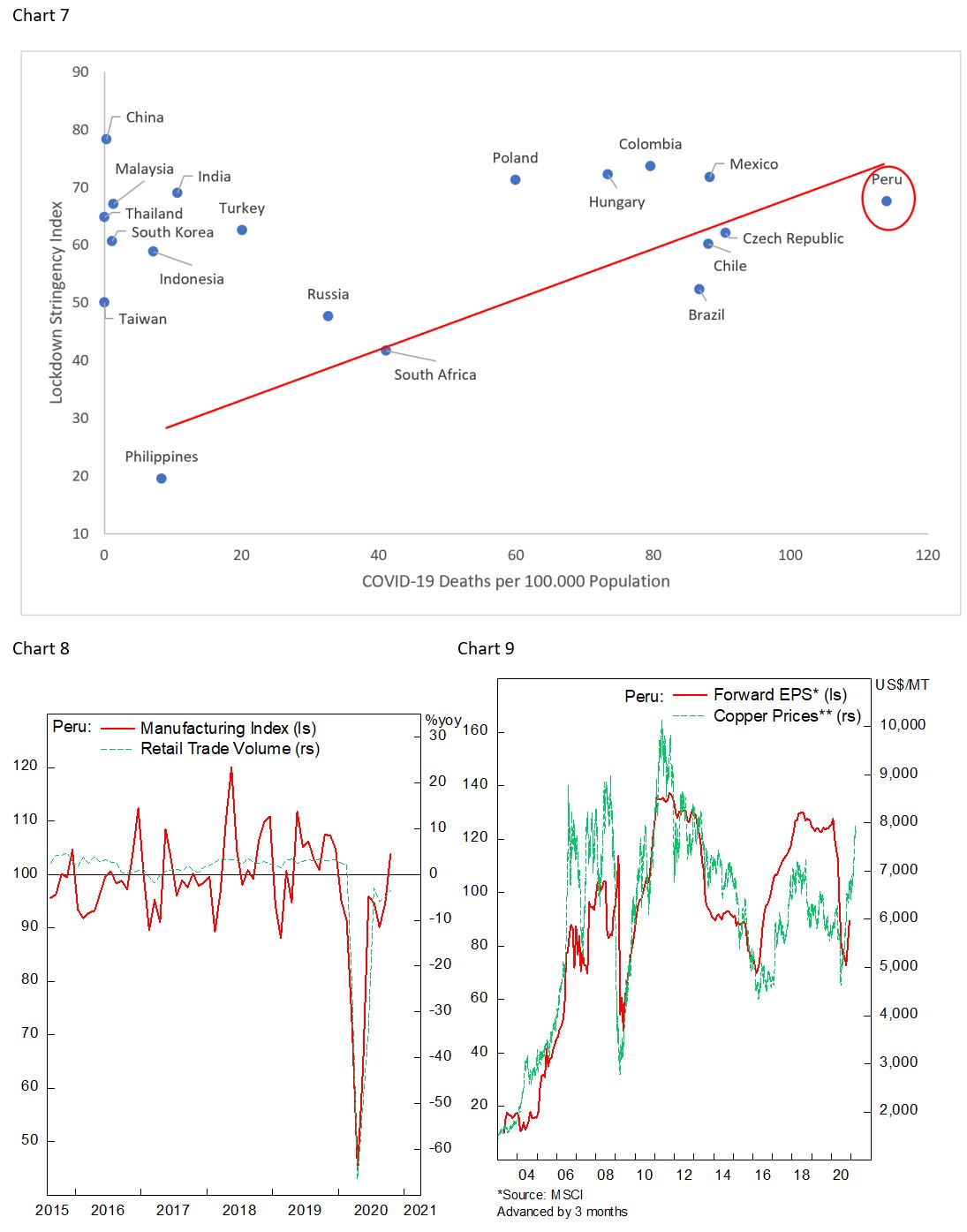

- Peru is among the worst to suffer from Covid-19 pandemic in terms of deaths per capita and economic damage (Chart 7), which make the case that a rapid distribution of an effective vaccine could help the country quickly reach the threshold for “herd immunity”, supported by the already high infection rate among large portion of the population. Currently, Peruvian manufacturing activity has rebounded above pre-pandemic level while retail trade is still slightly below last year’s level, both of which will be further aided by inoculation of the country’s citizen (Chart 8).

- Higher copper prices and improvement in the country’s terms of trade will boost Peruvian equity earnings, which currently is a third below its recent high (Chart 9). Copper accounts for 30% of the country’s exports and continuing growth rebound in the Chinese economy bodes well for commodities demand. Moreover, a broad-based dollar weakness will likely boost the metal’s price higher.

- Last year’s political drama related to the impeachment of former President Martin Vizcarra over corruption allegation by the Congress will likely colored Peru’s presidential and congressional elections starting next April, with candidates supporting the country’s anti-corruption drive likely enjoying popular support. The general public, 90% of which disapprove the Congress decision to impeached former President Vizcarra, likely pour their anger by punishing Accion Popular and Fuerza Popular, two party that support the impeachment.

Chile

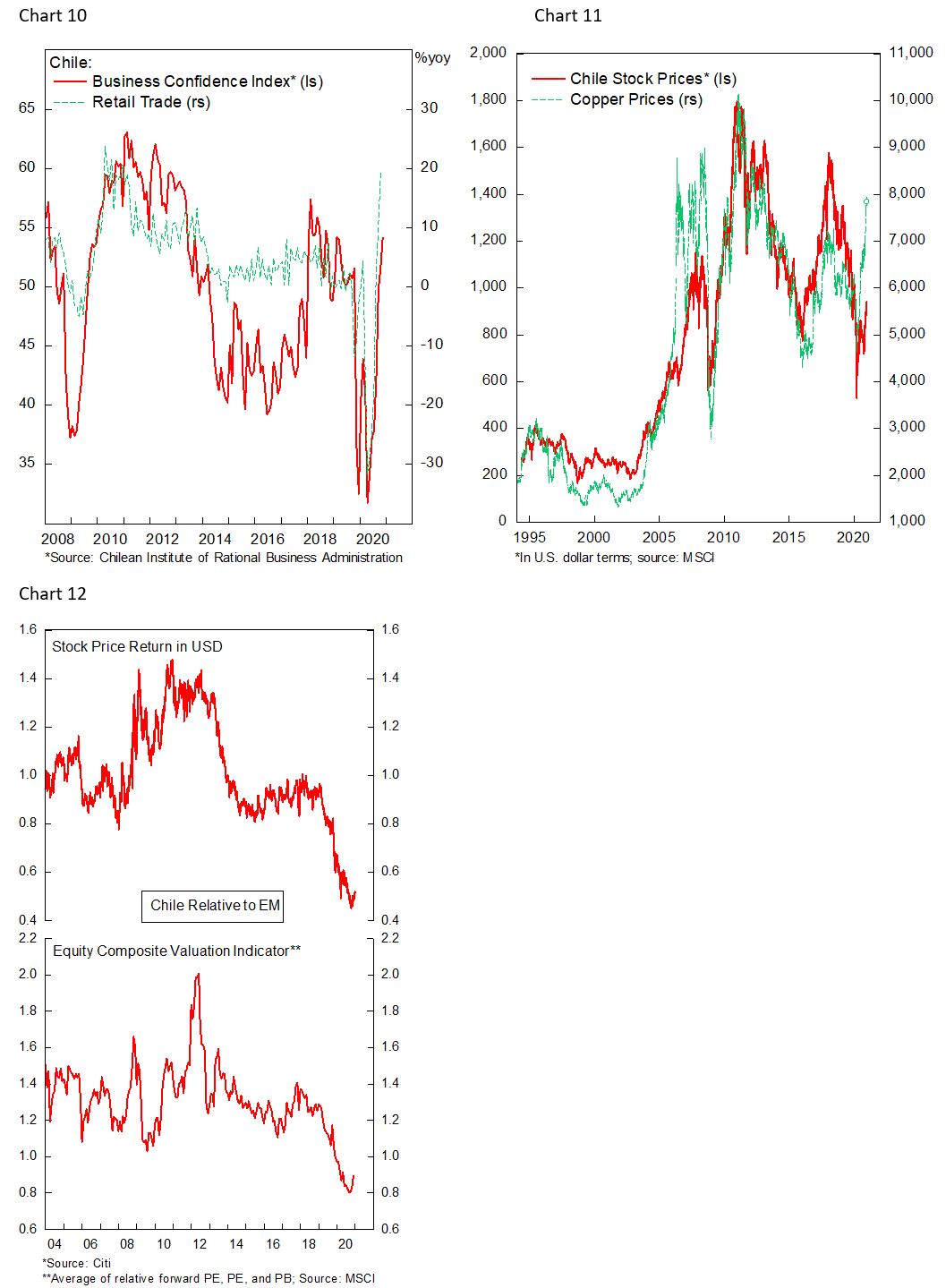

- Similar to Peru, Chile is a commodity-intensive economy, with copper accounting for over half of the country’s exports. The country will likely also benefit most from inoculation of its population, which ranks poorly in terms of death per capita. However, Chilean economy has fared relatively better, with business confidence soaring and retail trade surging 20% above last year’s level amid the approval of fund withdrawal from pension funds to aid consumption during the pandemic (Chart 10).

- The country’s equity market has deviated from the movement in copper prices (Chart 11), and the bull market in commodity prices and dollar weakness should further improve Chilean terms of trade. Moreover, Chilean equity valuation de-rating is likely over, with the market currently trading at 1.3 x book value and 17.2x forward earnings, the later based on a trough earnings cycle (Chart 12). Based on Cyclically Adjusted P/E ratio, the country is among the top 3 EM countries with the largest downward deviation from its long-term average, next to Czech Republic and Colombia (Chart 13). This points to the likelihood for multiples to expand going forward while earnings are boosted by higher commodity prices.

- On the risk side, the country is going to hold a local election in April, alongside vote on the constitutional bill, and followed by a presidential election in November, which could result in the country drifting left as a result of public anger over inequality and inadequate government role in the economy. Although the short-term impact may be contained, it could result in fiscal profligacy in the long run, with shake-up in the bond and currency market could not be ruled out.

Turkey

- Sweeping changes in the Ministry of Finance and replacement of the governor of Turkish central bank have brought back orthodox policies and boosted investors confidence on Turkish assets. Policy rate is now back above CPI inflation and the new governor has committed to a tighter monetary policy to curb inflation and building up the country’s grossly inadequate reserves, which if done successfully will propel the deeply undervalued Lira higher (Chart 14).

- Turkish economy has staged a V-shaped rebound fueled by credit binge (Chart 15). The tighter monetary policy comes amid the backdrop of easy global liquidity, weakening dollar, and rebound in global growth that could allow the country to escape another crisis or growth slowdown. Moreover, high carry in the midst of record low global policy rate potentially attract high risk-tolerance investors to load up on Turkish local-currency debt and drive inflows into the country, making it easier for the country to build up foreign-currency reserves (Chart 16).

- Turkey’s equity and currency valuations are both deeply discounted and reflect worst-case scenario for the country, with significant upside should it be avoided. The stock market is currently trading at 0.9x book value and 6.5x forward earnings, whereas the Lira is still trading 26% below our fair-value assessment after the recent sharp rally (Chart 17 and 18).

Our view on Mexico (SOW, although much of the upside has been realized this quarter. MXN is still 10% undervalued and equity multiples are still reasonable amid depressed earnings), Brazil (SOW/N, less bullish on stocks due to valuation but BRL is very cheap), Russia (N, view on oil and Biden foreign policy/sanctions over recent hacking of U.S. government agency) and South Africa (SOW, valuation still cheap) remained unchanged since 2020H2.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.