Download PDF: A Look at EM Financials K

List of Interesting EM Banks: EM Banks

- EM banks are relatively more interesting compared to its DM counterpart, especially European and Japanese banks, that have become a collateral damage from negative interest rate policy.

- EM firms are heavily underleveraged compared to its DM counterpart. Banks in Indonesia, Mexico and India will inevitably benefit from faster economic growth and credit creation. With less developed financial market, majority of EM firms rely on bank loans to lever up its capital structure.

- Monetary easing by central banks will result in the steepening of the curve. Potential pick-up in global growth and cheaper debt cost for many EM countries from declining yields will encourage firms to expand and stimulate credit creation

- EM could be divided into the “more developed” and “less developed” bucket based on credit to GDP ratio. However, each EM countries have its own cycle and growth characteristics, which require investors to analyze each country individually.

Brazilian Financials; Positive Outlook Amid Short-Term Cyclical Headwind

- The dramatic decline in long-term yields last year have translated to margin contraction among Brazilian banks. The country’s financial sector has largely priced this in, as reflected by the underperformance relative to Brazilian equity benchmark. The fall in yields, however, will have a twofold positive impact to Brazilian banks. First, it will likely stimulate credit demand from domestic firms that have previously shut out from the credit market due to expensive borrowing cost, increasing the volume of credit distributed by domestic banks in the medium term. Second, falling yield eases firm’s financing cost, reducing the numbers of firm having difficulty in repaying their loans and required provisioning by banks.

- Brazilian banks are not cheap when compared to other EM country’s banks, but the high profitability of the sector and still under-levered economy justify current high valuations. On the other hand, Brazilian banks are one of the most levered across EM bank universe, with debt-to-asset ratio of 34%, which will limit further rise in the sector profitability. It is likely that deeper penetration of financial access among Brazilians will increase the deposit base of Brazilian banks and allow them to reduce the proportion of debt as funding source going forward.

- We made the case last year that Brazilian central bank’s ability to ease monetary policy further is limited, as the cycle pick-up last year has resulted in inflation increasing to the upper band of central bank’s target. The combination of tighter fiscal policy this year and reversal of easing monetary policy will translate to weaker Brazilian growth this year. Investors should look forward to overweight Brazilian banks once early signs of cyclical upturn emerge.

Turkish Financials – Very Attractive

- Recent financial market development has all been supportive for Turkish banks’ recovery. Turkey’s yield curve has steepened dramatically as inflation has came down and the central bank slashed interest rate aggressively to prop up growth, which bode well for banking sector profit. Average borrowing cost has declined almost to its pre-crisis level, after spiking to 25% early last year, and the Lira has been stable of late, which should limit further rise in non-performing FX-denominated loans and bank’s provisioning.

- The country’s export-oriented manufacturing sector was hit particularly bad during the last crisis, with many firms restricted from credit and imported input cost rising meaningfully from lira weakness. However, recent high-frequency data has been encouraging, as highlighted by January’s manufacturing PMI increasing above 50 for the first-time post-crisis. Business confidence has also staged a V-shaped rebound after 2018 crisis and retail trade has accelerated significantly since the second half last year. The improvement in macro picture will release the pent-up demand for credit driven by business/inventory restocking and consumer’s durable good purchase.

- Trading at 7.2x trailing earnings and 0.8x tangible book value, Turkish banks are very attractive. Currently, earnings are 17% below its pre-crisis level and multiples are at a 25% discount compared to historical averages. Both earnings and multiples are likely to expand this year as the macro picture improve further, boosting Turkey’s financial sector performance, both in stand-alone basis and relative to benchmark.

Russian Financials – Positive Outlook Amid Sluggish Domestic Economy

- Russian firms, heavily concentrated in oil and gas sector, is very conservatively ran. Credit-to-GDP ratio of Russian economy, at only 60%, is comparable to those of Brazil and is less than a third of South Korean, a trend partly driven by the high borrowing cost and limited availability of credit to Small and Medium Enterprises (SME). This has resulted in state-dominated economy concentrated in oil & gas and an economy heavily influenced by the ebb and flow of oil prices, which is also reflected in the banking sector’s book.

- The 2014 oil price dramatic decline and sanctions against Russian firms resulted in a massive tightening of Russian credit condition, which led to increasing non-performing loans that have only began to decline of late. As a part of sanction-proofing the economy, Russian banks have been building buffer to withstand external shocks. Debt portion of the banks’ capital structure has been more than halved since the 2014 sanctions, substituted by deposits, which is a cheaper and more stable funding source.

- Weak domestic growth and below-target inflation will force the Central Bank of Russia to be more aggressive in easing monetary policy, which should steepen the yield curve further and boost Russian banks’ profit. ROE of Russian bank, at 19%, is the highest among EM banks. Meanwhile, the sector is trading at only 6.2x trailing earnings and 1.3x tangible book value. The combination of high profitability and depressed valuation translate to generous dividend yield of Russian banks, currently at 6.2% and is among the highest in EM.

Indian Financials – Negative Outlook Amid Undergoing Economic Recovery

- In the past two years, India has been experiencing stress in its banking system, especially related to the concentration of bad assets on its Non-Bank Financial Companies’ (NBFC) book, as highlighted by the ILFC takeover by Indian government in 2018. Weaker domestic growth and concentration of highly levered firms in Indian banks’ book has resulted in some banks failure. Indian banks’ liquid assets ratio, at 8%, is the lowest among EM and concerning, as the lack of liquidity could potentially result in systemic failure of the banking system.

- The good news is that Indian economy has been showing early signs of recovery; terms of trade has improved markedly of late, which has historically lead credit expansion. After a lackluster consumer spending and business investment that dragged India’s economic growth to 4.5% in Q3 2019 from its peak of 8.1% in Q1 2018, it is likely that growth will stabilize around 5% this year instead of staging a V-shape rebound. The government is unlikely to deliver further stimulus as it already runs 3.8% of GDP deficit and further monetary easing by Central Bank of India will be limited as core inflation has likely bottomed. Hence from macro perspective, Indian yield curve is likely to flatten and hurt the banking sector profit, which has not been priced in by the market.

- In the medium-term basis, Indian banking sector is unattractive. It will take some time for Indian banks to deal with its non-performing loans, which at 9%, will require heavy provisioning and hurt earnings. Despite all that, Indian banks are trading at 26x trailing earnings and 3.2x tangible book value, the most expensive among EM bank universe. Investors should underweight Indian banks in an EM portfolio, a position in line with our negative view on Indian equity relative to EM benchmark initiated last year.

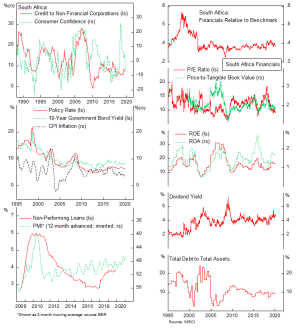

South Africa – Short-Term Rebound is Likely Amid Weak Growth

- South African banks sit on the more favorable rank among our EM banks universe, with decent profitability and dividend yield while trading at a reasonable multiple. Relative performance of South African financials relative to benchmark has been largely flat in the past two decades, as sluggish economic growth, social and structural issues have limit availability of credit mostly to large enterprises, which is a drag on bank’s revenue.

- Due to frequent economic crisis, South African banks are run conservatively. Capital ratio is well above Basel III requirement and debt-to-assets ratio of the banking sector is low, meaning that South African banks have a more stable and cheaper funding source compared to banks in other countries, such as in Brazil, Mexico and India. However, South African banks have a high operating cost compared to other EM countries, as highlighted by its non-interest expenses to income ratio.

- The underperformance of South African financial sector relative to benchmark is overdone and likely to mean-revert to the upside. With inflation under control and growth undershooting target in the past year, South African Central Bank is likely to continue its monetary easing, which will reduce banks’ funding cost. The risk is that South African economy may remain in slump this year, as recent monetary easing has not resulted in rising confidence among business and consumers. All these will hold non-performing loan ratio to remain elevated.

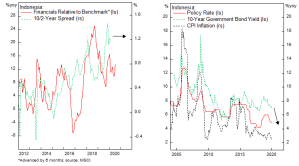

Indonesia – Positive Outlook

- Indonesia and Mexico are among the most under-levered economy in the EM space, giving an ample room for the banking sector to expand its loan book in the foreseeable future. Still low financial literacy and penetration among Indonesian population mean household savings are often not reflected in banking sector’s deposits. Combined with high credit demand from both large corporates and SME, Indonesian banking system has loan-to-deposit ratio exceeding 90%.

- The trauma from 1998 crisis, when many large banks went bankrupt, result in very conservative governance of Indonesian banks. The country has the highest banking capital ratio among EM countries, and probably in the world. Debt-to-assets ratio is also among the lowest in the world, at only 8%, which translate to a cheaper funding cost. As a result of its conservative governance, dividend yield has been kept low despite the wide Net Interest Margin (NIM) and high ROE, as profits are used to build up capital for further assets expansion.

- The long-term growth potential and fewer risk compared to other countries banking system placed Indonesian banks to trade at premium, but still at a lower multiple than those of Indian banks. Even before the recent banking crisis in India, Indonesian banks had better profitability and capital ratio relative to its Indian counterpart. Going forward, Bank Indonesia will maintain its loose monetary policy, as below potential growth and negligible inflationary pressure allow policy rate to be slashed further, which should prevent the yield curve from flattening significantly

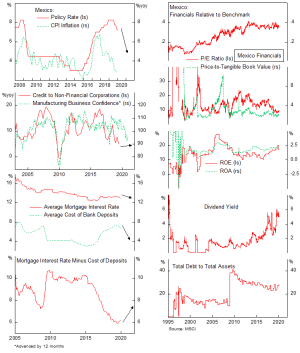

Mexico – Very Attractive Due to Further Monetary Easing

- Similar to Indonesia, Mexican economy is grossly under-levered, and banks will benefit from further penetration of credit to the real economy. However, Mexican economy barely grew in 2019 due to uncertainties related to USMCA and downturn in global manufacturing cycle, especially related to auto production, which has depressed credit growth and will limit credit expansion in the short-term.

- There is a wide room for the central bank to cut its policy rate further, as inflation is undershooting target and price expectations are moderating to the downside. This will likely push the yield curve to steepen dramatically this year and benefit banks’ profit margin.

- Long-term outlook for Mexican banks is positive. The sector has a decent profitability and NIM, similar to those of Indonesia, but with a cheaper valuation, higher dividend yield and higher leverage (less conservatively run). The banking sector experienced NIM compression starting in 2015, but the trend has shown early sign of reversal as cost of funding decrease alongside with policy rate cut.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.