Download PDF: Monthly_201909_The Effects of Money Printing by Central Bank Globally

Why has inflation stay benign despite massive quantitative easing by most developed countries central bank?

Negative Yields and Inequality

It is natural that if something is not sustainable, it will stop. That is my general thoughts in the past few years after reading Thomas Piketty’s book, Capital in the Twenty First Century. After decades of wealth accumulation in the hands of few and fewer people, I believe we are reaching the extreme point where the trajectory of inequality going forward is certain to go down.

The negative yields on government bond is just one of the natural consequences of such wealth accumulation in the past century. It is like a symptom of a sick world, with inequality as the cause. Wealth that is saved rather than consumed and redistributed is truly the underlying factors pinning all the symptoms we see today. Negative yield is essentially a tax on the “rich” and a subsidy for the government to enact social spending towards the lower income population. The Modern Monetary Theory (MMT) is indeed already happening today and will likely intensify until the global savings glut reach its equilibrium, wherever that is.

From a social point of view, this is a positive development for spreading equality within and across countries. Moreover, the sum of all human utility or happiness should increase as people from lower income class would experience a better living standard from government subsidy while the upper income class would suffer from higher taxes and lower income, but the decline in overall utility is much lower than the increase in lower income household. During its heyday, risky government such as Argentina could borrow for 100 years at a relatively low yield. Today, Greek borrowing rate is below 3%, an unprecedented shift from its 30%-plus rate during the European crisis. None of these developments would happen without the excess global savings.

The world, just like our body, has its own healing and counterbalance system and cycles. In a democratic country, it is rather unsustainable that more than 50% of global wealth is owned by 1% of the population. It has always historically led to revolt; the creation of worker union in the past century is one from many developments that counterbalance the accumulation of wealth by capital owner or entrepreneur. Today, we see the counterbalance force in other mechanism, among them low investment return and the tendency of socialist government to win the election. This tendency is dangerous due to the slippery slope of socialist and strong leader type of president to undermine the integrity of its institutions and capitalism in general.

There are several factors leading to these developments. First, if we have too much money chasing too few goods, the result is spiraling inflation. But the problem is that one’s capacity to consume is limited: there’s only so much caviar one can eat and only so much sport cars or luxury watches/bags one can collect before the marginal benefit of more of the same thing turned zero, or even negative (from storage and maintenance cost, and also psychological burden). Hence, the excess money must be in some way invested; too much money chasing too few investments leads to deflation in investment return. When the trend reaches its extreme, as it is now, then investors are willing to suffer from negative real return or even slightly negative nominal return. Why? The answer is storage, security and convenience cost. The ability to easily move wealth between investment exceeds the penalty cost of storing money in the banks or money market. The analogy is similar to being charged service fees on our checking account for the convenience of storing money in the banks and having access to ATM and debit card.

Where Would Superior Return Be Found?

Alternative risk premium will continue to offer higher ROI for investors with high risk tolerance. Illiquid alternatives, investment with term lock-up and seed funding are likely to offer the risk premium associated with each factor. Superior returns would also still exist in a country with restricted capital flow, where investors will not have free access to the capital and move funds out of the country quickly. In this case, however, there will a discount priced for compensating the risk that investors could not withdraw their funds outside the country.

In the developed world, VC and PE activities are also likely to proliferate further, putting a huge premium on growth companies. Since borrowing is a cheap way to finance a venture, companies are likely to gobble debt further as long as their interest coverage ratio does not deteriorate into junk level. Hence, investment grade bond investors are faced with the greater fool theory, with real rates for some of them below zero and the expected capital gain is diminishing in the already low-rates world.

High-yield bond, priced based on spread against treasury, will also benefit from the decline in yields. In our opinion, these companies possess the greatest risk in economic slowdown. The compression of yields has resulted in complacency among risky borrowers to issue ever higher debt level relative to its earnings. What was a 6x EBITDA leverage could easily turned to be as 7.5x leverage if earnings declined by 20%. This could easily tip such borrowers from the lower end of investment grade rating (BBB), which currently stands at a record amount, to junk. Cascade of companies experiencing such difficulties in one sector of the economy could easily spread into a systemic crisis, halting bank’s willingness to lend and increasing their bad debt, which in turn, feeds into further provisioning and contraction in credit.

Emerging Market countries are likely to be in a better position. EM currencies should be stronger as capital inflow toward higher yield corporate and government debt from European and American institutions push yields down. Emerging Markets policymakers, traumatic from previous balance of payment crisis, are likely to shift their focus from inflation target towards stronger growth and mitigating external risk, as the subdued global demand will also have its deflationary impact on emerging countries, which has already been seen in the current low inflation figure for Mexico, Brazil, Indonesia and other countries with twin deficit and history of inflation problem.

When Will Inflation Be Back?

Mass production and increased in productivity have resulted in cheaper price of many consumer products in the last few decades. Price for clothes, electronics and toys have declined as offshore manufacturing and more efficient production emanates goods in these sectors. Generally speaking, the price of goods has been stagnating while the price of services has been rising much faster. Problem is, the majority of consumption basket for the bottom half of household remains concentrated on goods consumption, the reason why it is difficult to stoke higher inflation.

In a developed country such as the U.S., where majority of people afford foods in the table (or government subsidized coupon) and cheaply imported clothes, renting cost is the only big burden for many low-income families. And for many of low-income family, education in state school is free and medical treatment is covered by Medicaid, with only few children go to university.

The answer of when inflation would accelerate above 2% may lie in how fast and effective the government could channel funds from negative borrowing cost to the population. This is essentially a transfer of wealth from the rich to the poor, just like taxes. Once enough lower income household moves to a higher income level, it is likely that their demand for more consumer goods and services increase alongside with inflation. The likelihood is, it may take decades, if not century to reach that point.

We are currently bracing a world with lack of stimulus and hence, lower growth; among the three major central bank, only the Federal Reserve is able to stimulate significantly, but even its tools are diminishing and less effective than what it was; fiscal policy is being constrained in major countries, where U.S. will suffer from fiscal drag, the European governments are either unwilling or not allowed to stimulate and China is only half-heartedly stimulating.

If this thesis is proven to be correct, demand for spending and investment will be much lower and corporate earnings are likely to have difficulty growing. Meanwhile, the multiple on equities should also be lower in the world with lower growth. This, however, is partially offset by the further decline in yields and cost of financing. The result of these two conflicting factors has yet to be concluded, but a simple assumption of dividend payout ratio of 45% (average 1960-2018), cost of equity of 6.68% (average earnings yield 1960-2018) and terminal growth of 4% (2% real and 2% inflation) results in justified P/E of 16.7x, which is slightly lower than at its current 17.7x level.

Long-Term Investment Implication

Due to the structural low return of bonds, pension funds and family offices are likely to shift their allocation toward equities and alternatives, propping up the multiples globally. Under-owned equities sector and region will have a readjustment of valuation. The shift from bonds to stocks as core portfolio position should benefit Chinese A Shares, Emerging Markets and European equities.

Moreover, the growth of private capital will surmount public capital as the attractiveness of going public is reduced for companies. Bargaining power of founders indeed have been increasing of late: dual class share structure and more attractive financing terms from PE and VC are some examples. In a world lacking investment opportunities, entrepreneur has increasingly greater say on the negotiation table and is able to shop around for the best deal.

Demand for clean energy is going to eventually lead to surge in alternative energy production, putting pressure on coal and oil prices as developed countries switch their electricity sources to windmills and solar panel, both of which already become cheaper relative to coal-based source. ESG themed equities are likely enjoy further recognition from institutional investors, replacing allocation to traditional energy firms. Regulatory push in developed world is also going to accelerate the switch among electricity producers.

Medium-Term Investment Implication:

Various countries’ Leading Economic Indicators published by OECD have shown a turnaround in the economic condition of Latin America and Asian region, while those in U.S. and Europe is still on the process of bottoming. Accumulate under-owned equities. We continue to advocate building risk position with overweight on Mexico and Turkey. Our call on long Argentine stocks earlier this year failed spectacularly after the primary result showing CFK is likely to win the presidential bid. Argentine assets are a bargain and the Fernandez pair could temper down their rhetoric on debt default, which are likely to boost asset prices. On currency and fixed income side, long CAD and AUD against JPY, a classic global reflation trade and long EM local currencies bond unhedged.

Model Update

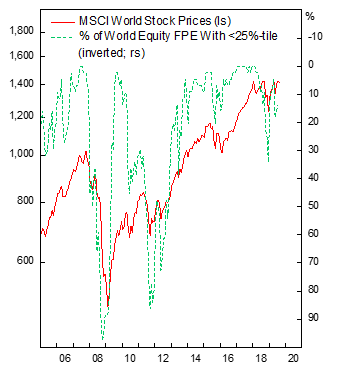

Our quantitative models recommend taking a more aggressive posture toward the equity markets and we think this is a good time to accumulate on select countries’ equity. On the chart below, we show the MSCI All-Country World Index performance in U.S. dollar terms since 2006 and the percentage of the number of countries recommended by our Global Equity Strategy (GES) model. Historically, a number above 30% has led to a massive rally and return in the next 24 months. This is a contrarian indicator to measure the attractiveness of world equity market. The model considers not only valuation, but also other fundamental factor such as profit and liquidity profile for corporates. Countries that are deemed to be attractive are: Austria, China, Colombia, Germany, Spain, Finland, France, Ireland, Italy, South Korea, Mexico. Malaysia, Netherlands, New Zealand, Philippine, Portugal, Thailand and Taiwan.

We also cross-validate these recommendations against our Global Equity Relative Strategy (GERS) model, whose result is shown in the table below. Countries in the model universe is ranked from those with low probability of falling further to those with highest probability, based on its valuation picture. Countries that are attractive according to both models are Austria, Colombia, Spain, Italy and Mexico.

We like Turkey for its extremely cheap valuation, improving earnings prospect and cheap lira; Colombia for its improving profit outlook, valuation and cyclical play; Japan for valuation perspective; and Mexico for both valuation and cyclical play. We have been positive on Italy in the past months, but the narrowing spread of Italian bonds against German bunds and recent rally have made the equities less attractive. Meanwhile Canada is still weighted by its weak currency and oil price, which we expect to rise as more data shows clarity on the global turnaround that we expect to bottom this year.