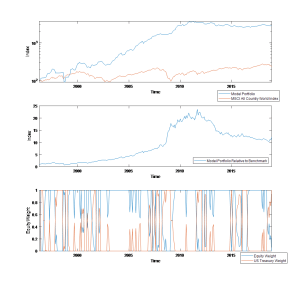

Our strategy last quarter to allocate small portion for equity paid off handsomely. Since we first launched our asset allocation model in October 2018, our model portfolio returned by 1.8% while our benchmark, MSCI ACWI, lost 6.0%. This month, the model recommends increasing the defensiveness of the portfolio by allocating 100% to bonds, a safe-haven asset.

Mind you that volatility is not one of the model’s input, hence the decision to become defensive is driven by a fundamental factor rather than by the market. We concur with this decision, although we do still carry our Emerging Markets equity position since last October, which currently still within +/5% of our purchase price. Despite being cautious, we do still believe that there will be a last “hurrah” or rally in the equity market before the economy tumble into a recession and EM equities are going to be the one that benefit most.

Equity or No Equity?

Growth across the world is still robust, especially in the U.S. and most emerging market countries, and the correction across equity markets in 2018 has made the valuation in both emerging markets and developed markets significantly cheaper. This creates a conundrum in our asset allocation decision, on whether we want to have a significant equity position in the portfolio, after acknowledging that we are in the late phase of economic expansion and our model’s defensive positioning. On the other hand, we know that the equity market usually rallies during the flattening of the yield curve, even during the early phase of the inversion, which is happening currently.

Our risk management policy allows our current 30% weight on EM equity, on the assumption that even if EM equity continue to drop for another 10%, our portfolio would drop 3%. However, it is likely that we would cut our position when the market is against us for another 5%, limiting the downside. And if such event happens, we would also continue to benefit from our 50% weight in long-dated U.S. Treasury. On the other hand, if we do see a rally in the equity market and our forecast turned out to be correct, we would clear 4.5% gain on the portfolio for our core equity strategy. Assigning 60% probability on our forecast happening and 40% on the bear scenario, we have a positive expected return on this strategy.

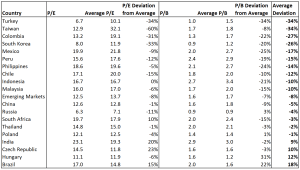

Emerging markets equity are currently trading at 10.4x forward P/E and we forecast the multiple to expand to 12.0x in 2019. Meanwhile, we think that EPS growth will average in the 5-10% range, giving an upside potential of over 15% for EM stocks this year. U.S. stocks multiple will stay at the current level of 13-15x forward P/E. After a time-consuming research on EM equity at the firm I’m working at, I have a deep conviction that EM equity offer an excellent risk-reward trade off currently.

Among EM itself, we favor Turkish equity due to possible re-rating of the market from currently depressed valuation level. Assuming end of 2019 forward P/E multiple of 8x, Turkish equity may have an upside in the north of 30%, after accounting for EPS growth and currency appreciation from the current level. Mexican equity also provides an attractive upside potential, above 20%, with the equity multiple expanding to 14.0x Forward P/E from currently 12.5x and after accounting for 10-15% currency appreciation.

U.S. Treasury Notes

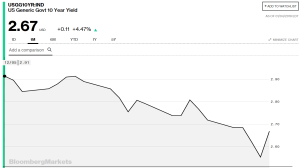

Regarding our heavy position in U.S. Treasury, we would like highlight that the drop in nominal yield for 10-year U.S. Notes has bring the valuation into fair value territory. Quoting our previous post on December 5, 2018:

“Our research shows that in the past 10 years, real yield of 10-year UST is averaging at 0.86%. With the real yield currently at 1.15% (based on PCE), we forecast a further 0.29% downside for the yield to 2.61%, assuming PCE inflation stays at the current level.”

Our forecast turned out to be correct, with the 10-year U.S. Notes yielding 2.91% on December 5, 2018 and 2.67% today, a 2.4% profit on unleveraged position. Hence, we see limited upside potential from our Treasury position and plan to shift the capital toward other safe-haven assets that have more attractive upside potential.

Emerging Markets Bond

We continue to see upside potential on EM bonds, especially from Brazil, India, Indonesia, Mexico and Colombia. Real bond yield for these countries are above 4%, and with local investors shifting their allocation toward more defensive assets, we think nominal bond yield for these countries will shrink further on the backdrop of controlled inflation. We also believe that MXN, COP and INR will appreciate relative to U.S. dollar in 2019.

Conclusion

Overall, we still believe that we should not be too defensive as our model suggest due to the conducive environment for equity to rally this year on the backdrop of a dovish Fed and a healthy but decelerating growth across the world in 2019. We see that up to 40% allocation to equity is prudent in such environment, combined with a constant mix rebalancing strategy. A bond portfolio combined with long-dated equity call options strategy is also a reasonable alternative to limit the risk of downside.

Trade Ideas:

Long Emerging Markets Equity

Long Turkish Equity, Unhedged

Long Mexican Equity, Unhedged

Long Colombian Equity, Unhedged

Long Japanese Equity, Unhedged

Long 10-year Mexican Bond, Unhedged

Long 10-year Indian Bond, Unhedged

Long 10-year Indonesian Bond, Unhedged

Long 10-year Colombian Bond, Unhedged

Long Gold vs USD

Long JPY vs USD

Long JPY vs EUR

Long CAD vs USD

One thought on “Putamen Capital: January 2019 Update”