Thesis Review, US Treasury and Emerging Markets

Prior to discussing our model update and 2019 sector outlook, we want to review our investment thesis from last month (Nov 24th), which has been panning out nicely. In the post we wrote:

“In the anticipation of Fed backing-off from rising rates further in 2019, we do believe equity markets will rally with EM outperforming DM. Our conclusion from studying previous cycles and yield curve inversion is that the market will have another up leg before major correction happening in the current cycle…

…We like U.S treasury securities and believe that yield will go down further. Our forecast is for 10-year yield to drop toward 2.8%, giving us expected return of 5% from the holding. As discussed above, lower inflation expectation and accumulation of safe haven assets in anticipation of downturn should bode well for bond prices.”

And we want to credit ourselves for getting these two events correctly. Last week’s Powell dovish speech has initiated a market rally and the short-term risk of worsening trade war has dissipated after Trump-Xi meeting in Argentina on Sunday. As a result of these two events, among other things, the 10-year UST yield had drop from 3.05% to 2.91% today (Dec 5th), equivalent to 1.5% unleveraged return. Previously we have been very defensive on the portfolio, with Treasurys allocation at 80% of total portfolio value. And although we are still on a defensive stance, we initiated a significant shift in our tactical position by entering emerging markets equity. We have shifted 30% of the portfolio from UST to emerging markets equity after Powell’s dovish speech; we also noted a huge ETF inflow to EM by global investors, which has been long overdue.

Our research shows that in the past 10 years, real yield of 10-year UST is averaging at 0.86%. With the real yield currently at 1.15% (based on PCE), we forecast a further 0.29% downside for the yield to 2.61%, assuming PCE inflation stays at the current level. We think that the risk of inflation is tilted to the downside due to slowing economic growth and significant decrease in oil price. And yes, it means that the 10-2 yield curve will invert by 10-20 bps and before that time we hope to exit our EM position.

The reason behind the shift in allocation to emerging markets equity is simple. The asset class has been battered badly that valuation has become very cheap, trading at 12.5x earnings compared to the average of 13.83x. Forward P/E has also dropped into an attractive level at 10.64x relative to the average of 11.03x. Hence, we are forecasting around 10% upside potential from multiple expansion alone. Combined with short-term EPS growth rate of 7-9% this year, our target for emerging markets equity is to rebound to a slightly lower level than this year’s high.

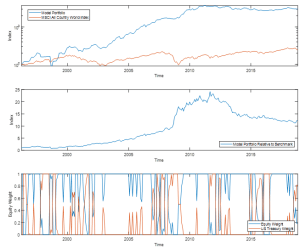

December Model Update

For the month of November 2018, our asset allocation model outperformed the benchmark (MSCI ACWI) by 0.33%. The model’s suggestion for allocation to equity increase from 18.3% last month to 18.9% this month, hence decreasing the recommended exposure to bonds to 81.1%.

We decided to overrule this recommendation by shifting allocation to EM equity as we think we are early, and the model will catch up with our view next month. Should this not be the case, we will become more cautious and prepare to reduce our exposure if the high frequency data supported our view. As for the country equity allocation, our equity model still holds its recommendation on Russia, Hong Kong, Finland and Indonesia.

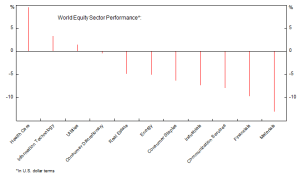

Sector Valuation Overview

As investors are increasingly aware of being in the late cycle, procyclical sectors such as financials, energy, materials, consumer discretionary are being underweighted. Meanwhile consumer staples, health care, IT and utilities are being favored. We understand these factors in play, but we increasingly like financials because of its attractive valuation, even after accounting for the risk. This sector has been trading at a discount due to market’s fear that in the next downturn, banks will experience increasing NPL and must set large amount of provision. Also, with tighter regulation and implementation of CACR and Basel III, banks should become safer and less profitable going forward, which warrant lower multiple. Although all these reasons are valid to underweight financials, we think the correction is overdone and the sector deserves higher multiple considering the profitability, even after accounting for the recession risk.

Meanwhile, we are bearish on health care due to several headwinds. First, there are collective efforts worldwide to suppress increasing drug cost, limiting the price increase of OTC drugs and revenue growth of generic pharma. But within the sector, early stage firms involved in gene editing, stem cells, gene therapy and new drug discovery, are still promising. Investing in these firms, however, require deep understanding of the scientific procedures involved and bottom-up valuation. We hold an option position on Supernus Pharmaceuticals (SUPN) and have a target price of $55/share. We have been following this company since early 2017 and our investment thesis has been panning out nicely so far, which we believe will continue going forward.

Kevin Yulianto, PFM