This year proved to be a volatile one, starting with the volatility jump in February, which led to emerging markets turmoil. Argentina and Turkey have suffered from increasing inflationary pressure that was exacerbated by the plunging currency, and other emerging market countries have suffered too, albeit at a lower intensity. Chinese A-share has been beaten down significantly in U.S. dollar terms. However, it is only until this month that U.S. stock market start feeling the pain. Analysts have been downgrading their forecast across the sector; combined with the increasing risk premium for equity and rising interest rate, valuation must drop. In our view, however, some of the corrections are overdone and unjustified based on the fundamentals. Here, we would like to decipher which countries offer an attractive opportunity for alpha generation in a world equity portfolio.

Economies across the world, except in U.S., have start slowing down. High frequency data shows a rollover in industrial production, PMI, and housing sector. In the U.S., housing sector has started rolling over too, but PMI and IP are still at a very high level, indicating the strong economic activity from fiscal boost. Our view is that U.S. economy will eventually slow down too, in the first quarter of 2019. Currently, Putamen Growth Fund allocates less than 10% of the portfolio assets into equity, as we believe that the correction is still on its early phase and volatility is going to be increasing in the medium term. As the equity valuation gets more attractive, we would reassess our allocation.

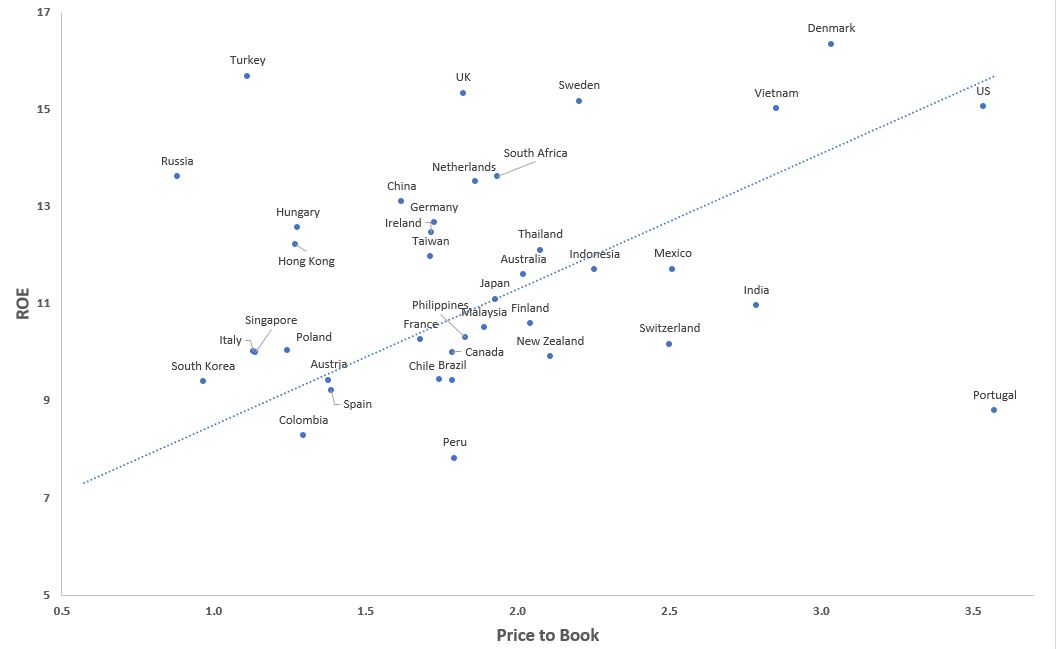

In the table below, three traditional valuation metrics for 40 developed and emerging countries are ranked from the highest to lowest. It’s true that these metrics are backward looking in nature, however it’s still useful to assess the relative valuation across the countries listed. Combining these valuation metrics together by standardizing them is useful for ranking purpose. For example, if we rely solely on single metric such as P/B, we would think that Greece equity market is very attractive, when actually it is not the case considering the relatively high P/E ratio.

P/B ratio figure tend to be more stable relative to P/E and EV/EBITDA, but it does not tell the earnings generation capability of the overall market. Meanwhile, EV/EBITDA assess the valuation of the overall firm, regardless of the capital structure, giving a wider perspective of valuation compared to market capitalization based metrics such as P/E and P/B ratios.

Relying solely on valuation ranking, however, does not tell investors the whole picture. Profitability and solvency of the market are also crucial in assessing the downside risk. For example, although Chinese equity market is currently trading at below than the world average equity valuation according to P/B and P/E metrics, we need to also consider the fact that it is highly leveraged compared to other emerging market countries. The net debt/EBITDA of Chinese equity is 5.9x; should revenue growth slows dramatically due to the effect of trade war, companies with high USD debt will see its EBITDA contract while interest expense increase, which could spin into liquidity crunch.

These indicators are then translated into three main indicators representing relative valuation, profitability and solvency across countries. This will be the base of Putamen Capital equity allocation, among other qualitative consideration.

We like the equity market of Hungary, South Africa, Russia, Singapore, Japan, Indonesia, Turkey, South Korea and Thailand. The only market we have difficulty to invest in is Hungary due to the lack of reliable ETF security. Russian equity is cheap by any metrics, profitability is above average, and leverage is moderate. The only risk investing in Russia is the political and governance risk, which we think is being outweigh by the reward in the medium term.

Putamen Capital assign different weighting for these countries in our portfolio allocation, depending on their attractiveness in our quantitative strategy. Instead of allocating equal-weight for the markets we like, we use exponential weighting for our allocation weights, amplifying the gain should our call prove to be correct. For example, we currently assign Russia 24% of our equity allocation and Turkey 8.1%. We are mindful that as a U.S. dollar-based investor, we are also exposed by the currency fluctuation of our overseas equity allocation. Investing in emerging markets equity are also much more volatile because period of equity corrections is often accompanied by currency depreciation. Undershoot in equity and currency, however, provide an attractive reward should the market bounce to an equilibrium level.