A regime change is underway in markets. The two decades of disinflation, globalization, and central-bank dominance that shaped a generation of portfolios are giving way to a more fragmented, inflationary, and fiscally driven world. This note lays out the new playbook across three lenses: the geopolitical backdrop, the shift from monetary to fiscal dominance, and how to navigate a market cycle that increasingly rhymes with past manias.

Geopolitics: Hot Peace

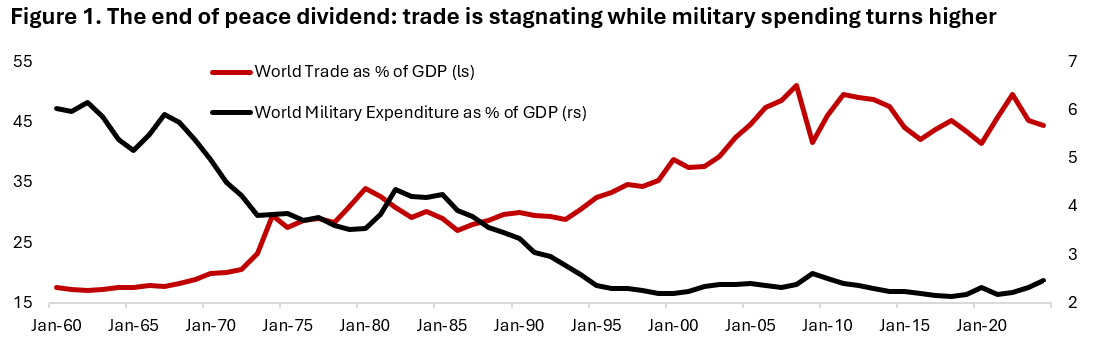

The past decade has been defined by two clusters of large-scale regional conflict. The first is Russia’s aggression against Ukraine – the annexation of Crimea in 2014 and the full-scale invasion of 2022. The second runs through the Middle East, where Iran and its proxies – Hezbollah in Lebanon and Hamas in Gaza – confront Israel and, by extension, the United States; that theatre escalated sharply after Hamas’s surprise attack on Israel on October 7th, 2023. These are material events, disrupting commodity and risk-asset prices and bending the trajectory of the global economy. Crucially, none has yet tipped into a global-scale war. But the absence of open war is not the same as peace. NATO has stayed out of the fighting in Europe, and internal divisions – alongside open questions about the credibility of the U.S. commitment to Article V – are quietly testing the usefulness of the alliance. This is the texture of a hot peace: no single rupture, but a steady erosion of the order that markets spent decades taking for granted (Figure 1).

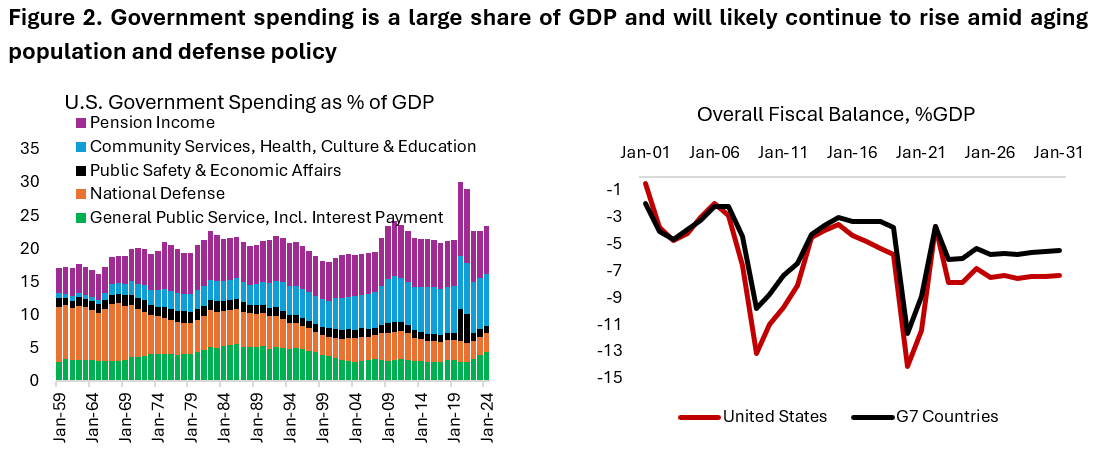

The backdrop rhymes uncomfortably with the 1930s, and three reinforcing forces explain why. The first is the rise of populism and authoritarianism, fueled by widening inequality and mass discontent with the status quo. Governments face pressure to spend more on education, healthcare, and pensions without the ability to raise taxes, forcing them to borrow (Figure 2). History rhymes here – 1929 was our 2009 – as the Great Depression then, and the combined legacy of the 2008 financial crisis and the COVID shock now, leave behind the same residue of social conflict, eroded trust in institutions and elites, and a reordering of the balance between superpowers.

That loss of trust feeds directly into the second force: the dismantling of the global order across defense, trade, and economic policy. Supply chains are being rearranged, bilateral deals are replacing multilateral ones, and protectionism is rising while global institutions and shared ideology recede. Social media accelerates the dynamic by letting the average person observe the lifestyle of the top 1%, sharpening resentment over how income and wealth are distributed. Much of that resentment traces back to globalization itself, which lifted China from poverty into a middle-class economy while hollowing out U.S. manufacturing – a rebalancing that never fully happened because Beijing’s long-running intervention to keep the yuan undervalued blocked the market mechanism that would otherwise have corrected trade with the U.S., Europe, and others. The historical warning is the 1930 Smoot-Hawley tariffs, which triggered retaliation and a collapse in trade – a cautionary parallel to today’s drift toward tariffs and industrial policy.

The third force is technological disruption, which raises uncertainty and creates sharp winners and losers. The industrial revolution inflated a bubble in railway stocks and displaced manual labor across agriculture, textiles, manufacturing, and transport; the AI revolution now carries the same potential, except that this time it reaches into skilled, white-collar work.

These forces are not abstractions – they translate into concrete investment implications, and each consequence maps back onto the dynamics above. The retreat from a shared global order is the most immediate. The closure of the Strait of Hormuz has exposed how dependent many economies remain on Gulf crude, a vulnerability that will only accelerate the buildout of alternative energy – nuclear, solar, and wind – and push buyers to diversify their oil and gas suppliers, to the clear benefit of Canada and the United States. The same retreat makes defense and industrial innovation necessities rather than options, as nations move to reduce reliance on allies. Europe and Japan have pivoted from passive participants in regional defense toward shaping their own policy, and the winners may well lie outside the legacy defense contractors that have historically dominated government budgets.

That same fragmentation reshapes the opportunity set for global businesses. Rising trade restrictions shrink the addressable market for firms built on open borders, whether Unilever and Nestlé in consumer goods or Nvidia and ASML in advanced chips and chipmaking tools. The economies caught in between fare worse still: more risk becoming stuck in the middle-income trap in a more hostile environment, and those with large cohorts of young, unemployed workers – India, Indonesia, Nigeria, and Egypt among them – inherit the same populist and social instability described at the outset, now exported to the developing world. And the erosion of trust is perhaps reflected in the prices of gold and other precious metals, which tend to be a hedge when confidence in institutions and fiat money erodes. For the past two years, central banks themselves have been diversifying reserves away from U.S. Treasuries and repatriating gold held in the Federal Reserve’s vaults. This creates tailwind for Latin American economies that potentially benefit from both higher commodity prices and deeper integration into North American economies friendshoring continues.

The bottom line is that infrastructure, defense, alternative energy, and commodities will play an increasingly important role in the decade ahead, while fixed income stays under pressure as government fiscal positions deteriorate.

From Monetary to Fiscal Dominance

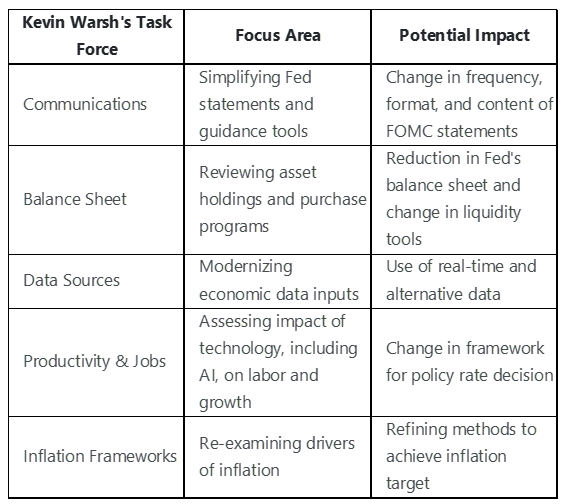

Aside from the change in geopolitical backdrop, perhaps more importantly for several years now the driver of the world economy and financial markets has been shifting – from central-bank dominance toward fiscal dominance. The appointment of Kevin Warsh as Federal Reserve Chairman has the potential to further crystallizes that transition as the Fed could potentially take a backseat and become less of a driver for the financial market (Table 1).

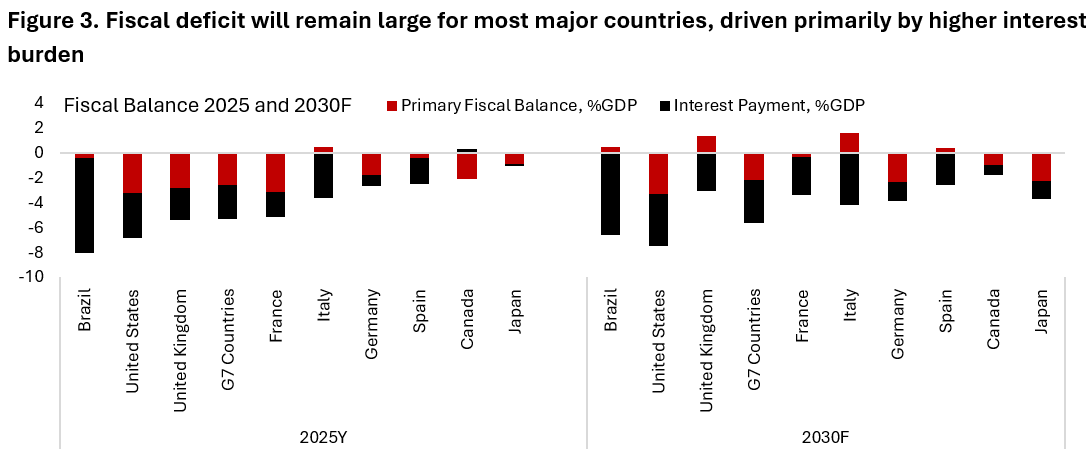

Today, the global economy is being driven more by what governments spend than by what central banks set. Fiscal policy – defense budgets, industrial subsidies, energy and infrastructure outlays – has become the marginal mover of growth and inflation, and monetary policy is increasingly reduced to reacting to it. This trend is unlikely to end anytime soon as most major countries in the world is expected to maintain large fiscal deficit in the coming years (Figure 3). To see how far the pendulum has swung, it helps to return to the era that defined the opposite extreme: the long reign of Alan Greenspan, when the Federal Reserve sat at the very center of the financial universe.

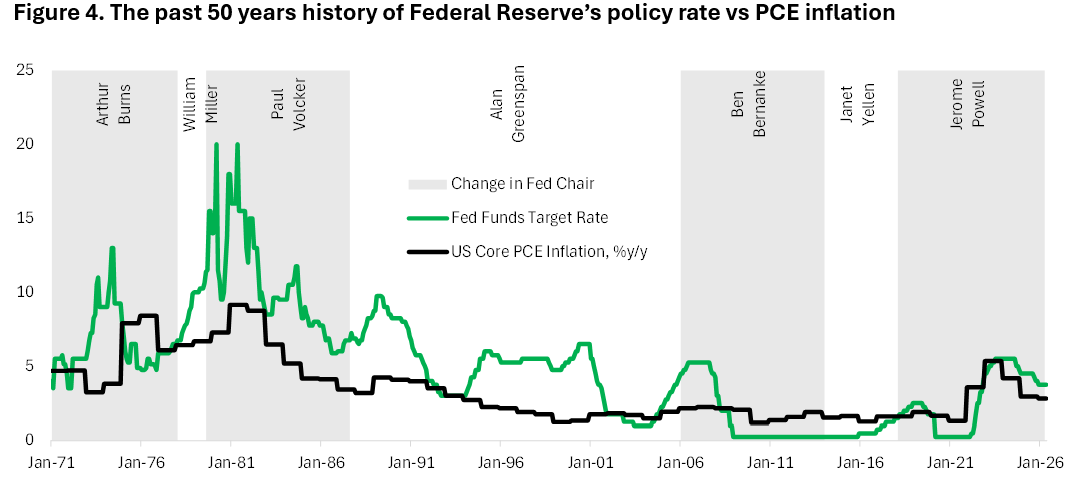

Paul Volcker may be remembered as the chair who tamed inflation, but Greenspan’s record is just as consequential. The second-longest-serving chair in the Fed’s history, at 18 years and 173 days, he presided over an era of relative peace, globalization, and rising prosperity. His reputation for bold policymaking was cemented during Clinton’s second term, when a booming economy put the Fed under pressure to raise rates and choke off any hint of inflation. Greenspan resisted. He suspected that rapid technological change was quietly lifting the economy’s speed limit in a way the official statistics had not yet captured, which meant he could afford to run policy looser than the textbook prescribed.

On the real economy, his judgment proved prescient. Where productivity had grown about 1.5% a year from 1970 to 1995, that pace roughly doubled between 1995 and 2003. The harder question was the stock market. As the tech sector boomed in the late 1990s, concern inside the Fed about overvalued equities intensified, and Greenspan had flagged the risk as early as his 1996 “irrational exuberance” speech. Yet he never mounted a sustained effort to lean against the boom with interest rates (Figure 4). The lesson investors drew – that the Fed would tolerate asset-price excess so long as inflation stayed contained – hardened into an enduring expectation that monetary policy existed to support markets.

That expectation is precisely what we have grown wary of. For years our view has been that the Fed has become too influential – shaping not only how markets behave but how they interpret the data itself, because every release is now read through the lens of how the Fed is likely to respond. The growing reliance on forward guidance has dulled many of the market signals we find more reliable than the Fed’s own interpretation; left to themselves, the wisdom of crowds tends to be the better guide.

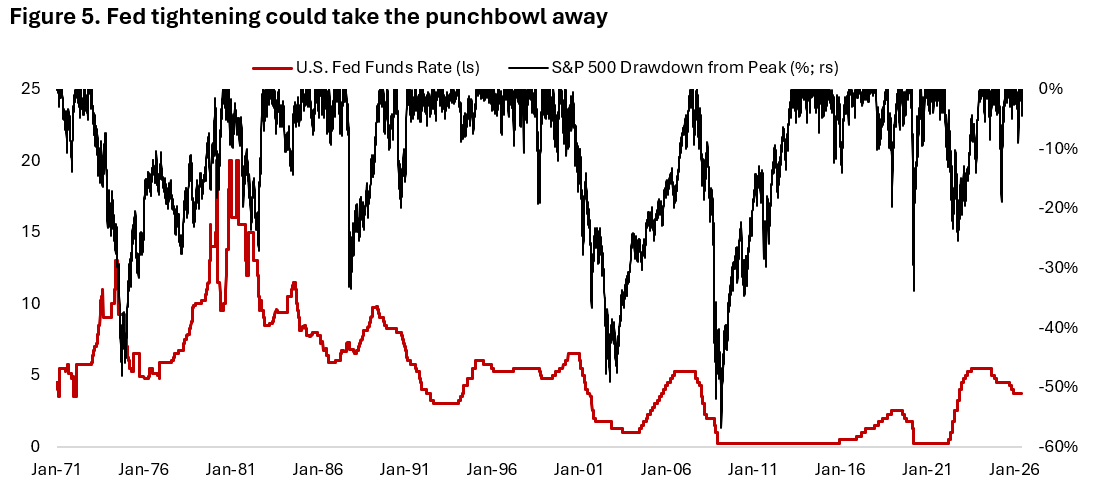

The backdrop ahead looks like the mirror image of those years. AI could once again lift the economy’s productivity ceiling, much as the 1990s tech wave did – but where Greenspan operated in a world of disinflation, excess savings, and a Fed that could afford to stay loose, today’s policymakers face abundant investment demand, scarce savings, and fiscal authorities setting the pace. With opportunities to deploy capital plentiful – the AI capex cycle chief among them – the cost of capital is repricing higher: the term premium has swung to roughly +60bps from –100bps in 2022. In this more inflationary, fiscally driven regime, the Fed’s bias may tilt toward hiking rather than easing (Figure 5), and its hand on the wheel is no longer the only one that matters. The 2000–2020 window of central-bank dominance increasingly looks like the exception rather than the norm.

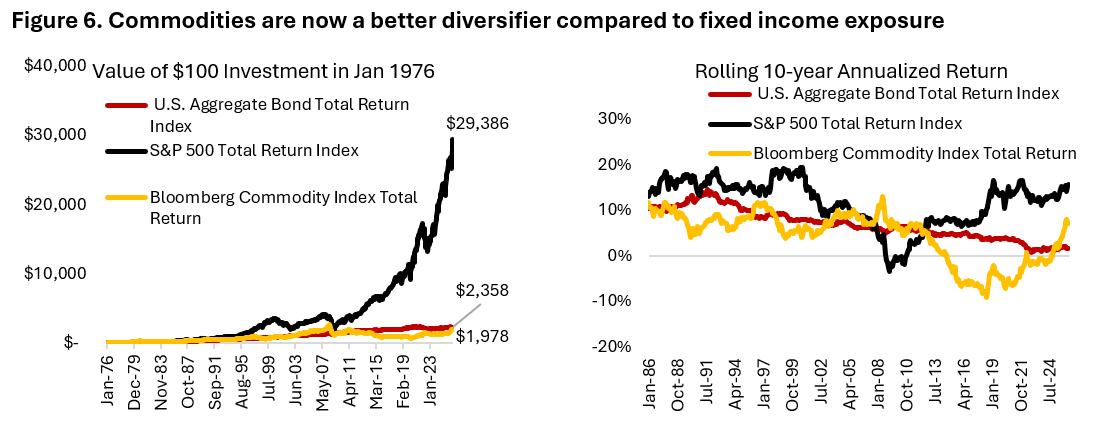

Taken together, the change in geopolitical trend and shifts from monetary to fiscal dominance point to higher portfolio volatility, greater inflationary pressure, and reduced attractiveness of fixed income. They also imply stronger investment demand – and therefore higher neutral rates – alongside lower trend growth as protectionism adds to deadweight loss in the global economy. Real assets gain importance as they become critical infrastructure, and the stockpiling of commodities and access to critical minerals moves up the agenda (Figure 6). This makes portfolio construction more relevant than ever. The new standard is 60/20/20 split across equities, fixed income, and real assets or diversifiers – an allocation we have championed in the past several years as a replacement for 60/40 portfolio. Today, most investors remain under-allocated to real assets and diversifiers – precisely the exposures best suited to the regime now taking shape.

Navigating Through the Market Cycle: Mania, Panic, and Crashes

Market returns over the past four years have been fantastic. Despite the fact that we have had a multi-year war in Ukraine, regional banking crisis, tariffs war, and more recently, the war between the U.S. and Iran, equity markets globally continue to break new highs. Retail favorites are ripping, SpaceX stock is up meaningfully from its IPO price, semiconductor stocks are going vertical, and FOMO is impossible to ignore.

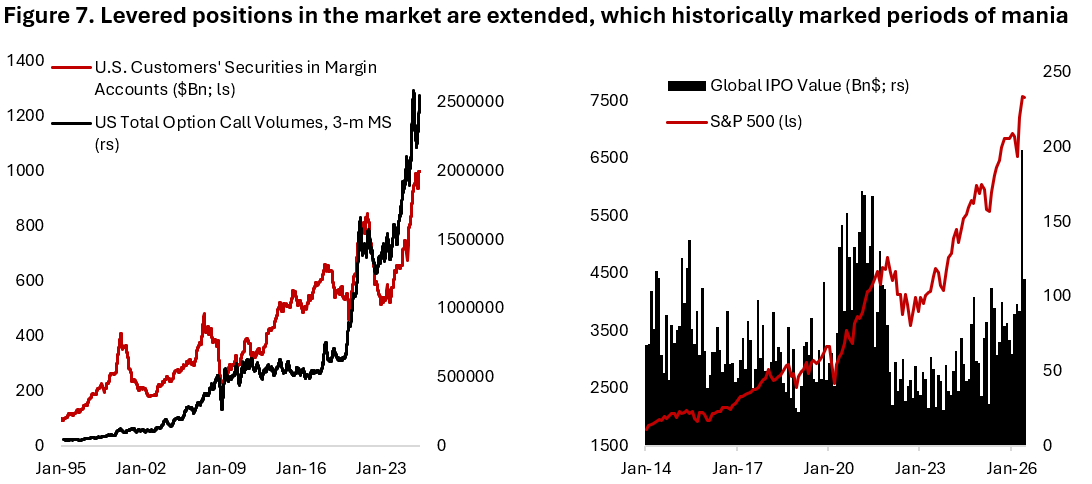

This is especially visible among younger investors, many of whom were shaped by a long bull market and a persistent buy-the-dip mentality. Risk assets are no longer simply owned; they are often owned with leverage, through options, or through instruments that shorten the distance between investing and speculation. The proliferation of zero-day options has blurred that line further. As Figure 7a shows, margin balances have jumped while call-option trading volumes have risen roughly fivefold from pre-pandemic levels – both classic signs of animal spirits. Meanwhile, companies are also going public and raised capital at an elevated valuation, with SpaceX raising $75 billion at valuation of 90x revenue ($1.8 Trillion) and Anthropic and Open AI slated to go public later this year at valuation close to US$1 Trillion. Similar to in 2021, there are signs of froth in the market (Figure 7b) More seasoned investors, having lived through the late-1990s technology bubble and the 2008 financial crisis, are therefore asking a different question: not why the market is rising, but what could finally arrest the bull market.

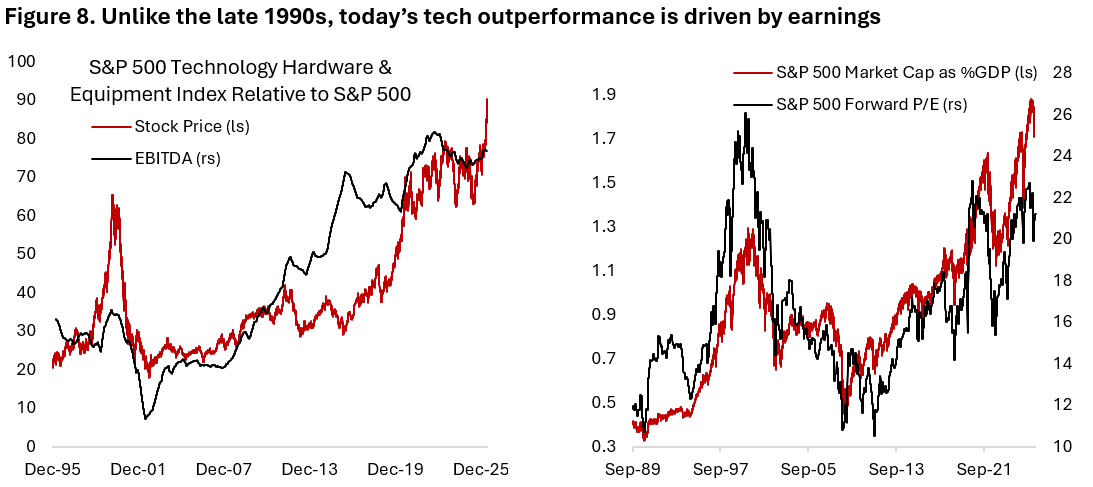

The semiconductor complex sits at the center of that debate. Its parabolic advances have not been built on imagination alone: revenues and profits have been expanding explosively for several years, far outpacing the growth of the broader market (Figure 8). Yet genuine earnings power does not preclude speculative excess. In fact, the most dangerous manias often begin with a powerful real-world story and then overshoot it.

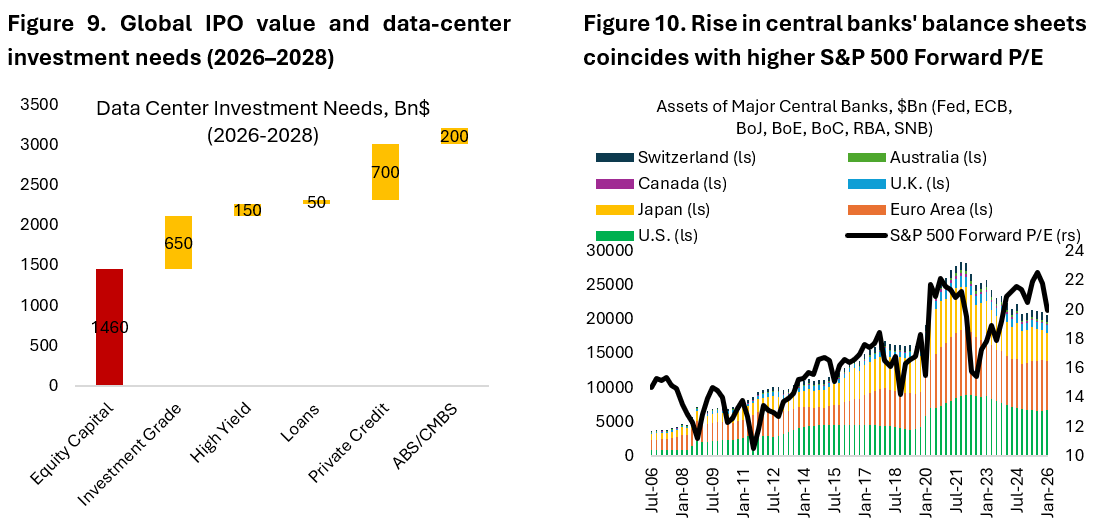

Technology manias are especially powerful because they begin with imagination colliding with genuine bottlenecks and opportunity. Today’s AI cycle has the same tension. Demand for compute is explosive, data-center investment needs are enormous, and the long-term productivity promise is real (Figure 9). Yet the returns on AI tokens, applications, and infrastructure remain uncertain. The parallel is not that AI is the same as the dot com boom, but that long-term adoption and near-term valuation can diverge sharply, just as they did in the late 1990s.

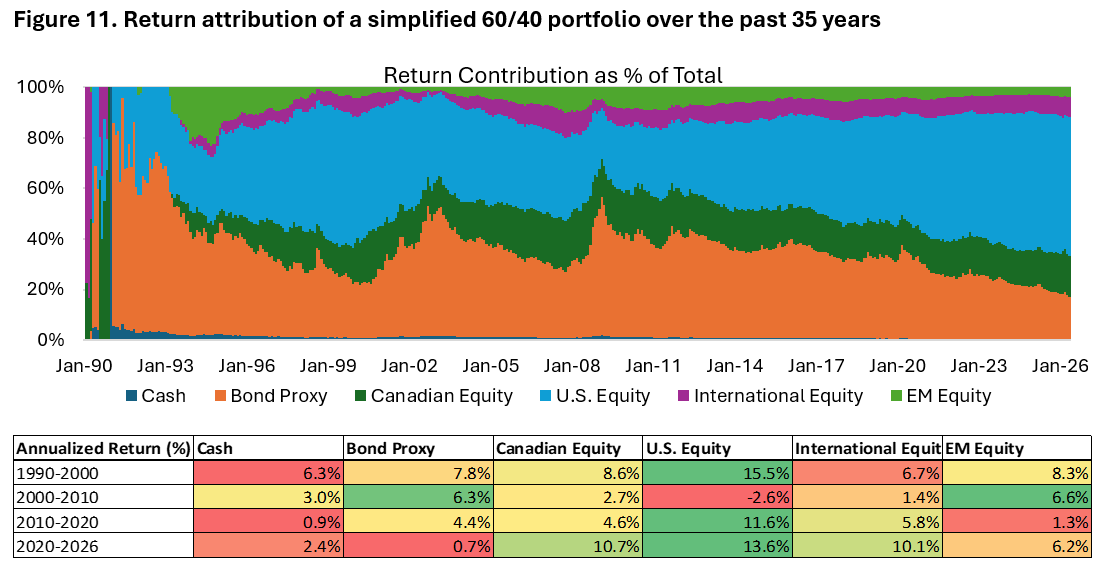

The easy liquidity backdrop today allows speculation to flourish. After more than a decade of quantitative easing, markets have been conditioned to abundant liquidity, suppressed discount rates, and the belief that central-bank balance sheets can expand whenever stress threatens the system (Figure 10). That legacy matters: cheap money lowers the cost of speculation, encourages leverage, and extends risk-taking far beyond what fundamentals alone might justify. It also teaches investors to treat volatility as temporary rather than dangerous, because for much of the post-2008 period the answer to market stress was more liquidity, not less.

That dynamic is amplified by the repeated willingness of central banks to intervene during crises from the pandemic to the regional-bank failures. This goes back to the change in the Fed discussed in previous section. Backstop may be necessary in the moment, but it also creates moral hazard by weakening the discipline of private lenders and investors. If market participants believe policy will rescue the system whenever stress becomes acute, they have less incentive to price risk conservatively in advance.

This is where Charles Kindleberger’s Manias, Panics, and Crashes remain essential reading. Despite the rise of quantitative strategies and algorithmic trading, markets are still governed by human nature: emotion, envy, FOMO, and herd behaviour. “There is nothing as disturbing to one’s well-being and judgment as to see a friend get rich,” he wrote in his book in 1978. The mechanism is familiar. As prices rise, investors see others getting rich and begin to chase the rally, pushing prices higher still. Rising prices then become their own justification until the marginal buyer is exhausted and the feedback loop reverses. Even sophisticated investors are not immune: many recognize that a bubble may be forming but convince themselves they can exit just before it bursts.

Kindleberger’s framework is useful because it does not dismiss the underlying innovation. Instead, it shows how real economic change can become the raw material for financial excess. The harder question is how to distinguish a genuine boom from a bubble while living through it. The reassuring answer in today’s market is that earnings are growing several-fold, so this cannot be pure speculation. Also, the market today prices semiconductor and semi-cap earnings as though it is near the end of a cycle – far from a bubbly level.

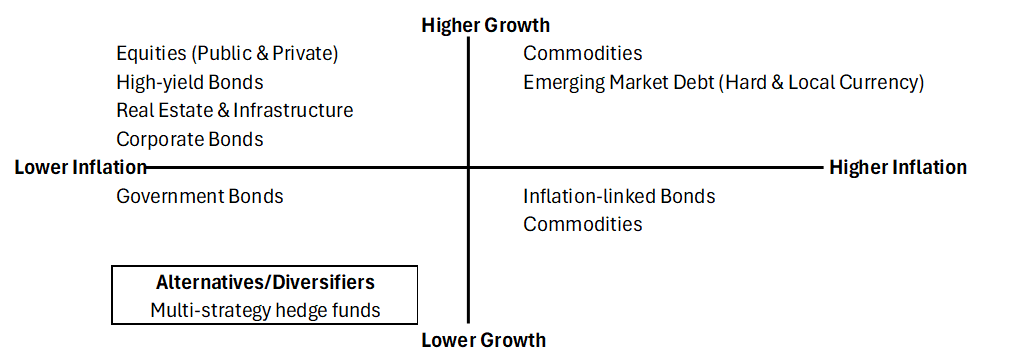

Over decades, equities have compounded far ahead of bonds and commodities, but never in a straight line. Leadership has rotated across asset classes, sectors, and regions, and periods of exceptional returns have often been followed by painful reversals (Figure 11). In today’s context, the leadership of U.S. equities, especially tech, in the past two decades could rotate into other regions and sectors.

The key risk today is whether returns are increasingly driven by the same underlying factor – AI. That single theme now runs through private equity, public equity, infrastructure, real estate, credit, and even sovereign and corporate bonds. As a result, many portfolios are less diversified than they appear. Mapping exposures across a growth-and-inflation framework can help identify where genuine diversification still exists and where the portfolio is simply expressing the same trade in different forms. Multi-strategy funds are probably the best diversifiers in this new world, as their returns have low correlation to the broader equity and bond market. A strategy that is based on manager’s skill, rather than market beta, provides a ballast during periods of inflationary shock when both equity and bonds tend to do poorly.

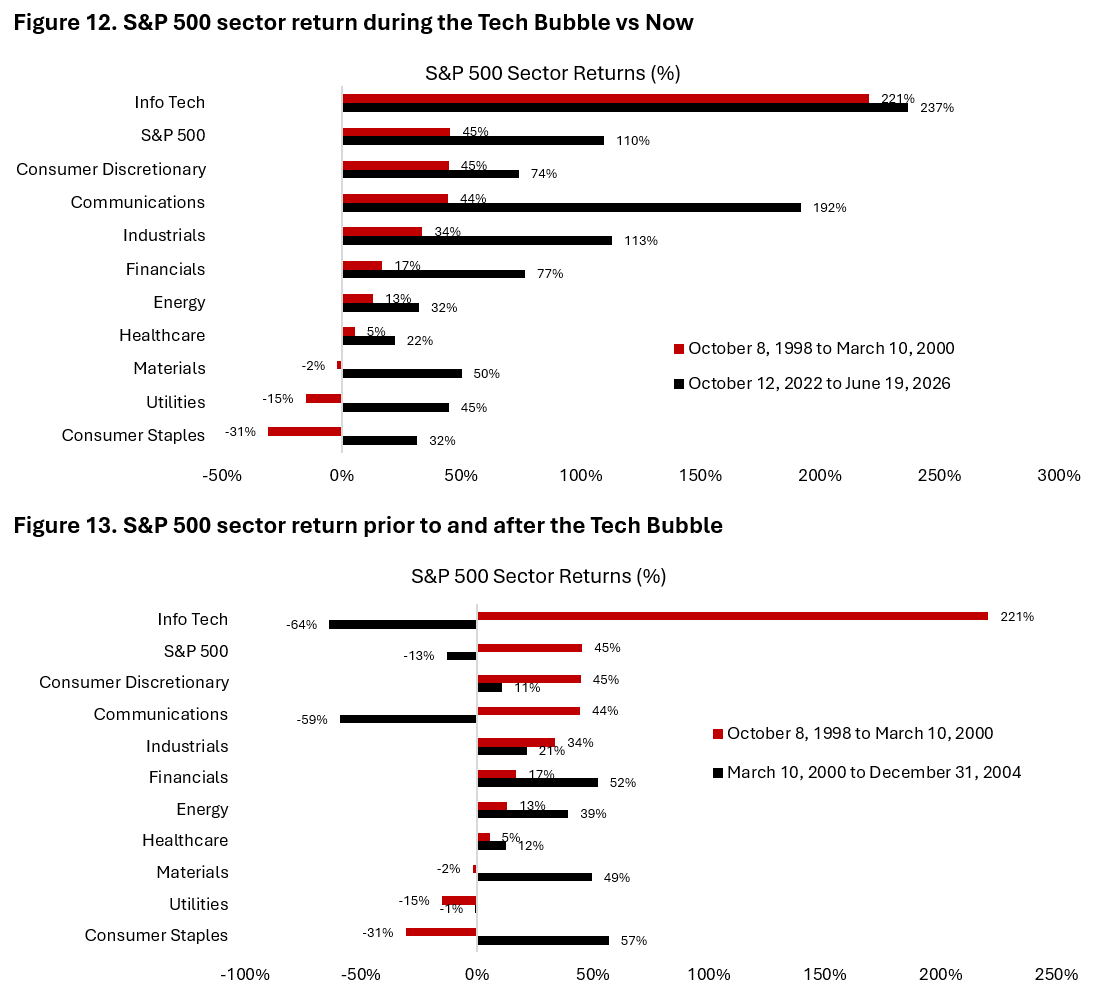

If the bullish case is right, the opportunity on AI-related stocks remains plentiful. But if it is wrong – or merely too aggressively priced – the hedge lies in active long-short equity and market neutral managers running alpha-focused mandates, where returns do not depend on the market simply grinding higher. Within long-only equity books, diversification across sectors is the key, as the market will rotate away from info tech and communication services sector – similar to what happened following the tech bubble burst in March 2000 (Figure 12 and 13).

The comparison with the dot-com peak is therefore instructive, but it should be used carefully. In 1998–2000, the rally was narrow and largely valuation-led; today’s leadership, while concentrated, rests on a broader and more durable base of actual earnings growth. That distinction matters. The central task from here is to monitor whether earnings continue to justify the price, or whether a powerful real-world story begins to harden into a market mania.

Copyright © 2026, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.