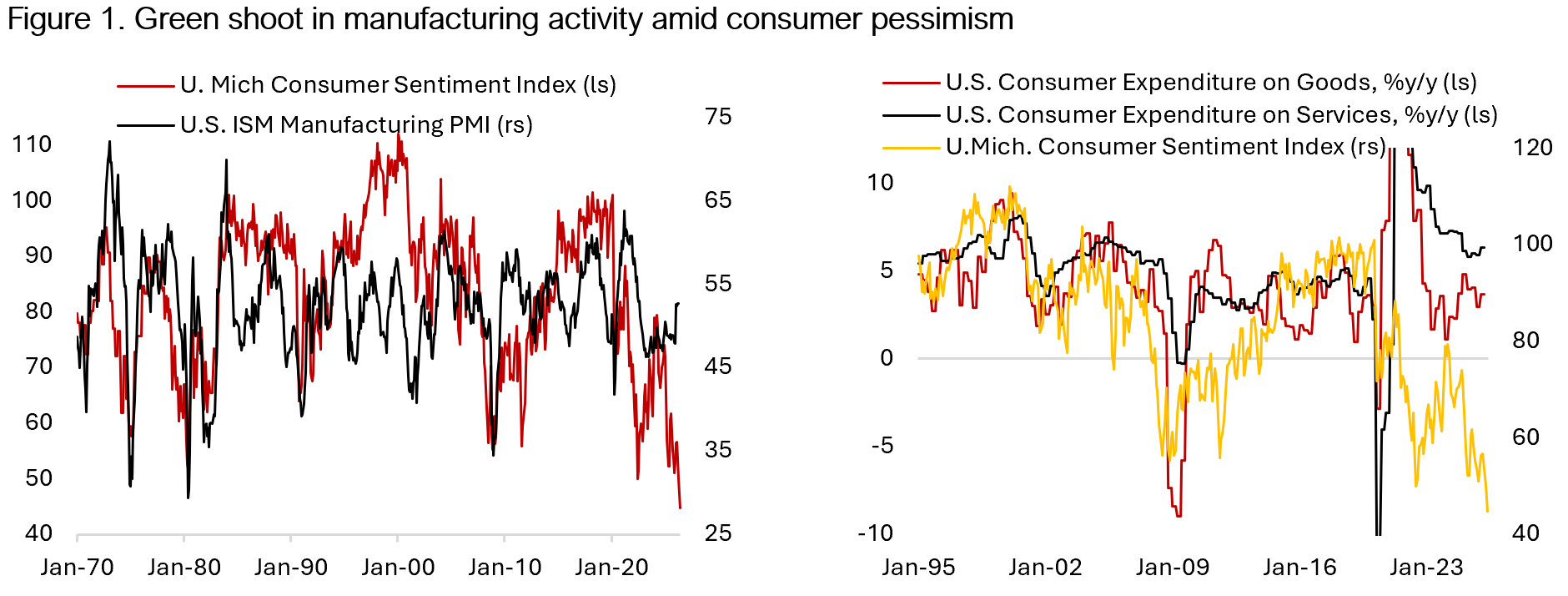

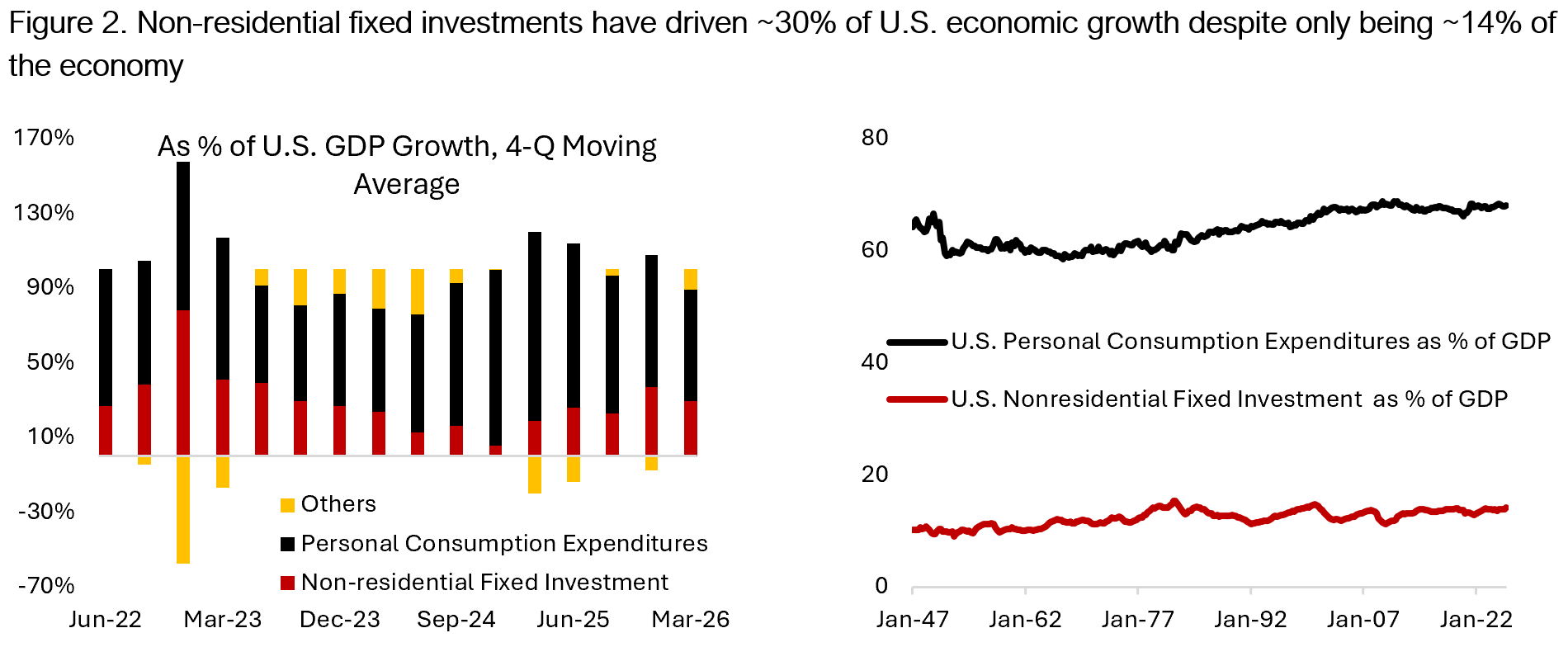

This acceleration in industrial activity amid consumer slowdown is also reflected in the U.S. GDP growth figures. Although consumer spending accounts for roughly 70% of U.S. GDP, economic growth in the past five years has been driven by investment – particularly in AI-related infrastructure. Non-residential fixed investments historically account for only 13-14% of U.S. GDP but has been contributing to over 30% of U.S. GDP growth in the past five years (Figure 2). Data centers, advanced computing systems, and energy networks are becoming the new engines of economic expansion. This shift has important implications. Industrial cycles tend to be more capital-intensive – driving real yields higher – more volatile, and more sensitive to policy and interest rates. The risk today is that long-term bond yields could march even higher and make it more expensive to finance all this investment spending.

Understanding the ongoing industrial-led business cycle upswing is important for investors. Within equity market, AI is the only theme that matters so far this year. Energy sector relative performance is back to below where it was before the U.S.-Iran conflict began, and investors’ focus remain firmly on the upward revision of hyperscalers’ capex plan. With ten largest companies in the S&P 500 now contributing to over 42% of the index, the fate of U.S. equity market is hinged on this one theme continuing to play out. Given that more U.S. and global investors have been gaining exposure through passive ETFs, and active mutual funds’ holdings are increasingly also resembling the benchmark, concentration risk is indeed very high across many major markets today. Since 2023, being more diversified and underweight on technology exposure has detracted from performance, with lots of active managers having to chase the AI-related stocks, whatever that means at different point in time, higher. Is this a market where the tail (passive) finally wags the dog (active)?

In spite of the boom in anything AI, it is important to note that underneath the hood there are signs of a non-AI industrial-led upswing in the U.S. and global business cycle. Backlog across industrial subsectors is growing again as their customers replenish inventories and enter another capex cycle, while the rate-sensitive transportation subsector seemed to have bottomed. For example, Ametek Inc. – manufacturer of electronic instruments and electromechanical devices – noted that the prior year saw headwinds from excess inventory at the customer level due to supply chain crises, which are now turning into a tailwind as de-stocking occurs. In other instance, Infineon advised its automotive customers that inventories might be too low, posing a risk of shortages if disruptions occur. Although there are concerns that the surge in new orders reflects a pull in demand in advance of the higher tariffs, increasingly we are seeing real demand growth across subindustries. Lastly, the buildout of datacenter to feed hyperscalers’ demand is bolstering needs for industrial machinery (i.e., Caterpillar) and all sorts of parts and raw materials required for the construction of AI physical infrastructure.

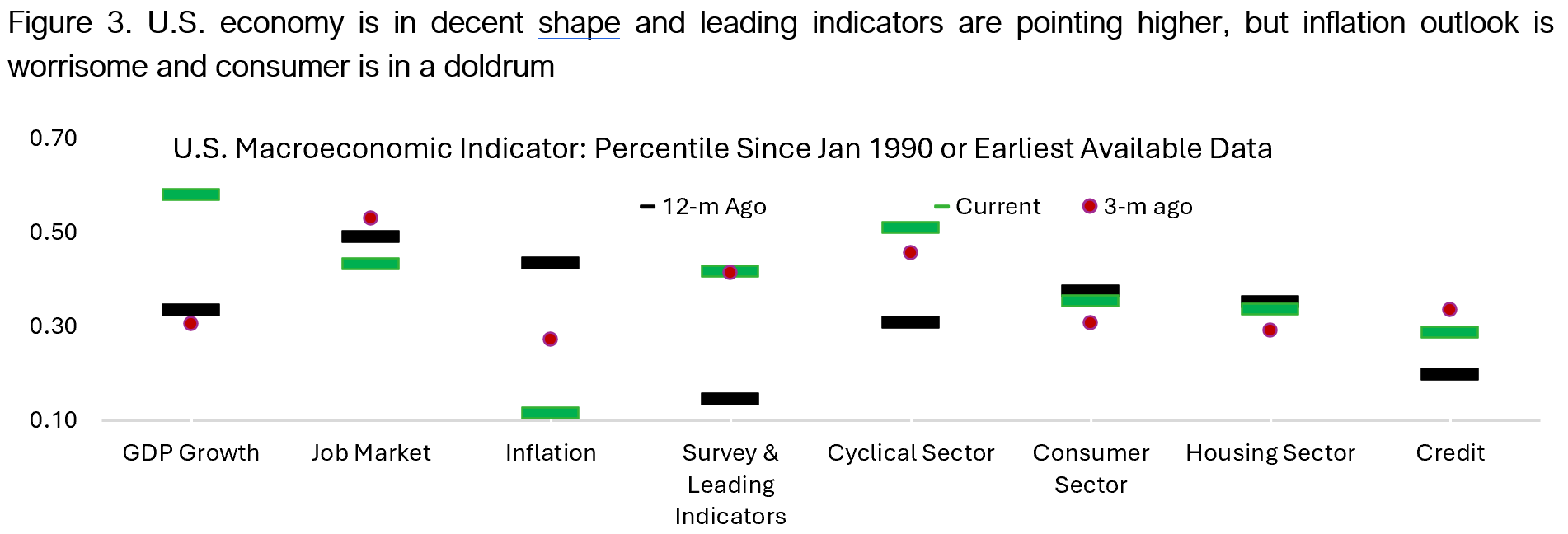

Our base case of continued acceleration in manufacturing activity and the AI tailwind persisting mean economic growth and corporate earnings should also be driven by these two themes. Figure 3 shows that our indicators of GDP growth has risen to the 58th percentile from less than 35th percentile three and twelve months ago, coinciding with the improvement in cyclical sector (51st percentile). Meanwhile, we expect consumers (36th percentile) to stay relatively weak for the rest of the year amid the backdrop of slowing wage growth, stabilizing but weak labour market, and headwinds on real spending amid inflation. The outlook for the housing sector will likely also be slightly negative until long-term yields decline more meaningfully.

AI is Inflationary in the Short Run, But Potentially Deflationary Down the Road

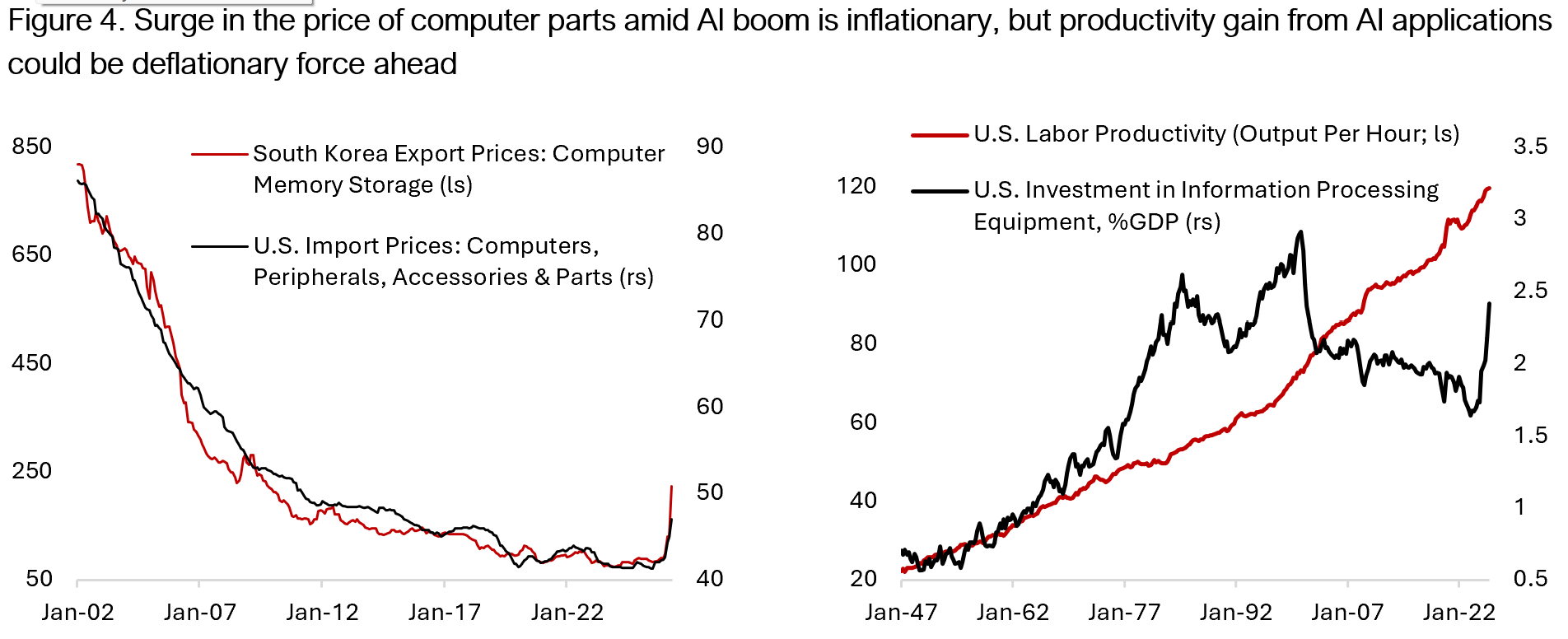

Over the long run prices of electronics and its components tend to decline over time, including computers and TV units. Since January 2002 to just prior to the AI boom, the prices of South Korean computer memory storage fell 91% and U.S. import prices of computers and parts declined 52%. The boom in AI capex spending, however, has bolstered demand for memory, chips, and other electronic components – pushing prices higher. The prices of memory storage have tripled from the low in mid-2023 while the prices of U.S. computers import increased by 14% over the past one year (Figure 4a). For consumers, this means households electronics’ prices will likely increase in the medium term, contributing to higher goods inflation in the U.S. Data centers, semiconductor fabrication plants, and energy networks are being constructed at an unprecedented pace, driving up demand for commodities such as copper, steel, and energy, reinforcing inflationary dynamics across the industrial economy.

Although the current AI investment spending is inflationary in the short run, the longer-term impact of AI application could be deflationary through improvement in productivity, which is determined by the available capital per worker and the adoption of technology. By automating routine tasks, optimizing decision-making processes, and reducing labor intensity, AI can lower costs over time. This is particularly significant in the services sector, which has seen much slower productivity gains and has played a major role in sustaining inflation.

Since the end of World War 2, the U.S. has seen tremendous productivity growth in its economy thanks to its thriving manufacturing industry in the 1960s and technological advancement in recent decades. Figure 4b shows that output per hour – a measure of labor productivity – has grown almost six times in the past eighty years. The ongoing boom in AI capex spending has driven investment in info tech equipment sharply higher. The adoption of AI in workplace will likely boost workers’ productivity even higher in the coming years, in addition to boost in “residual” (total factor) productivity arising from the use of AI agents. This will be important to support economic growth of many developed countries, many of which will see their population growth decline in the coming decades.

Apart from the buildout of AI infrastructure, there are several other factors that could drive inflationary pressure in the near term:

- A key driver is energy. Recent jump in oil prices amid U.S.-Iran conflict has caused damages on energy infrastructures in the Gulf, which will prevent oil price to falling quickly below the pre-conflict price even as the geopolitical tension ease. These higher energy prices are feeding directly into higher transportation and input costs for companies, affecting every sector from manufacturing to consumer goods, and acts as a broad-based inflationary force.

- At the same time, deglobalization is introducing inefficiencies into supply chains. Companies are increasingly reshoring production or adopting “friendshoring” strategies to reduce reliance on geopolitically sensitive regions. While these moves enhance resilience, they come at a cost. Building redundant supply chains requires additional capital expenditure and often leads to higher operating costs. For executives, it is not just a matter of where your factory is located, but also the supply of raw materials and other intermediary goods.

- Tariffs and trade barriers further compound the issue. These measures effectively function as taxes on both consumers and corporations, raising prices while constraining trade flows.

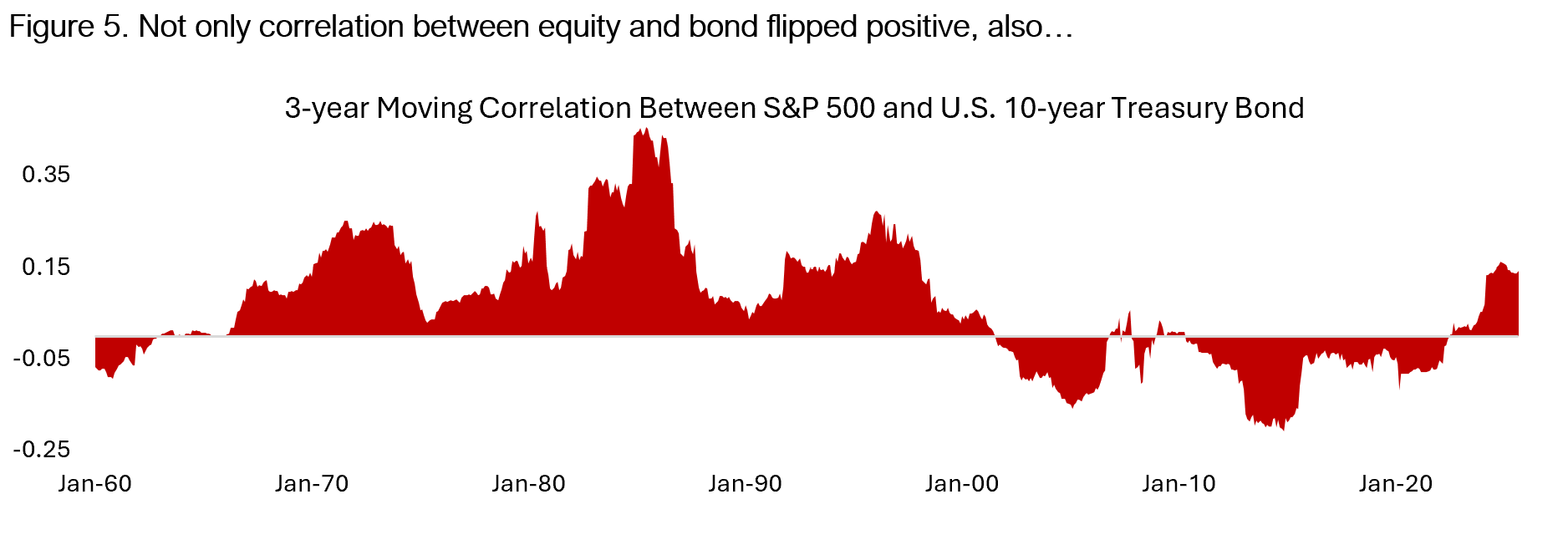

For fixed income investors, this means strategies that rely on duration exposure would see much higher volatility than in the past. The correlation between stock and bond price is also less reliable during this rising inflationary pressure, as we have seen since 2021 (Figure 5).

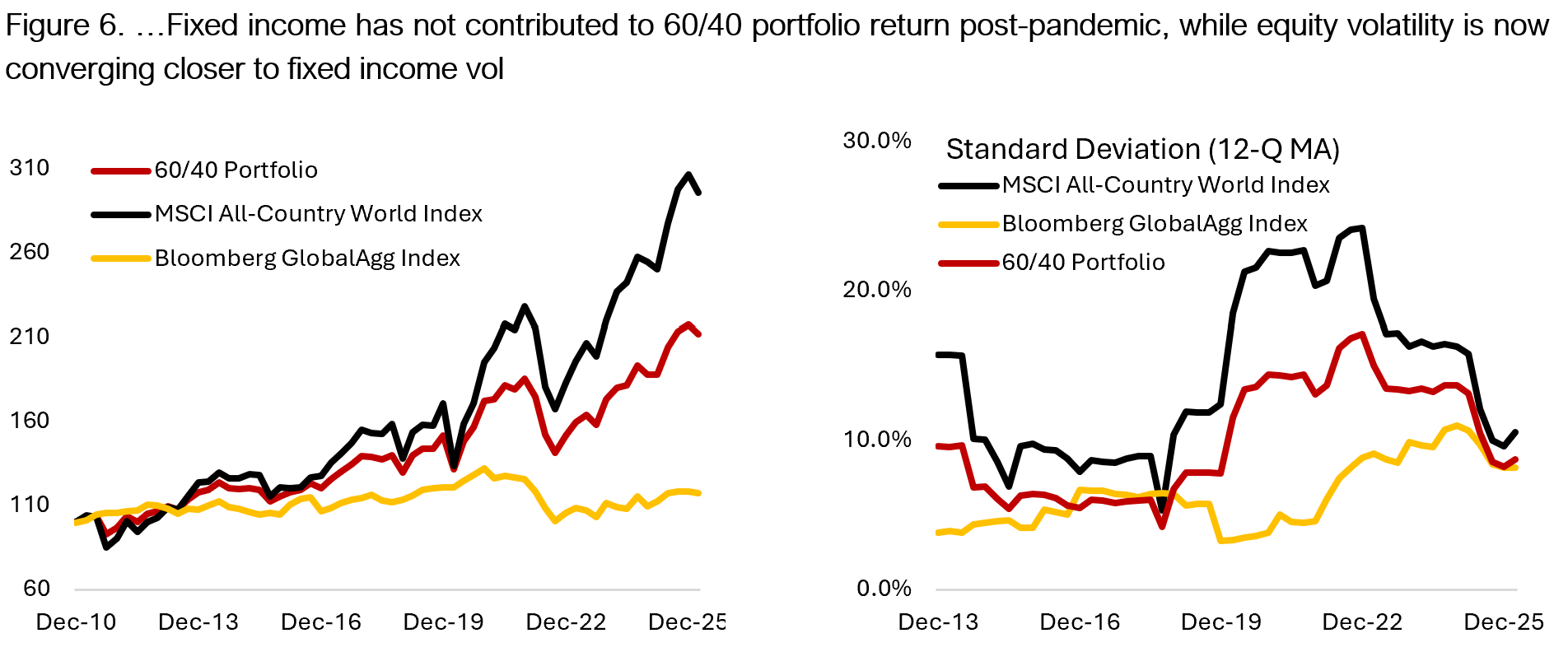

Rising yields—driven by energy shocks, fiscal concerns, and expanding term premia—have turned bonds into a source of volatility rather than stability (Figure 6). Meanwhile, defensive equity sectors with pricing power are acting as a better diversifier compared to fixed income exposure. As a result, investors are seeking alternative sources of diversification. Commodities, long/short credit strategies, and multi-strategy mandates are gaining traction as a replacement of long-only fixed income exposures.

The Investment and Social Consequences of AI Revolution

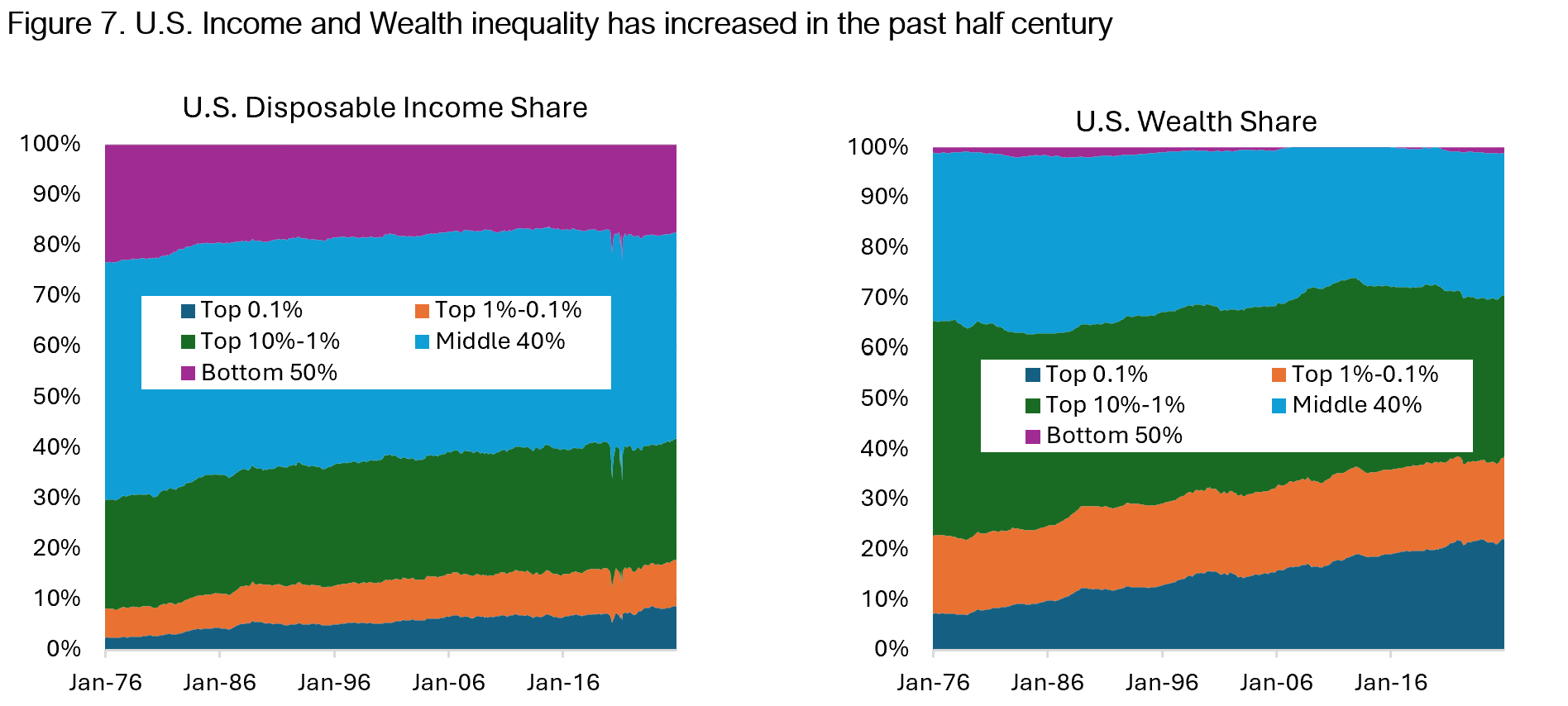

The sharp rise in valuation of AI model makers, such as OpenAI (US$852bn as of March) and Anthropic (US$900bn as of May), and the rally in semiconductor stocks have bolstered the wealth of their founders and equity investors. Global equity investors have also been rewarded richly by staying invested. Retail investors in South Korea, for instance, have enjoyed massive gains as the KOSPI index rallied over 100% YTD following a 75% rise in 2025. Meanwhile, American investors have enjoyed 115% rally since the S&P 500 bottomed in October 2022. Given that the beneficiaries of this AI-driven economy growth are relatively concentrated, income and wealth inequality have continued to rise in recent years. Meanwhile, the average workers – particularly those in roles susceptible to automation – face the risk of wage stagnation or job displacement. The chart below (Figure 7) shows that the top 0.1% of U.S. population now owns 22% of the wealth, with the rest of the top 1% accounting for 16% wealth share. Altogether, the top 10% Americans own 71% of the country’s wealth. The remarkable boom in wealth and inequality will carry significant social implications. From investment perspective, this could be an environment where companies catering to the wealthy could outperform those serving the mass – think of luxury goods and travel over consumer staples – as companies are increasingly incentivized to chase the wallet share of high-income and wealthy population.

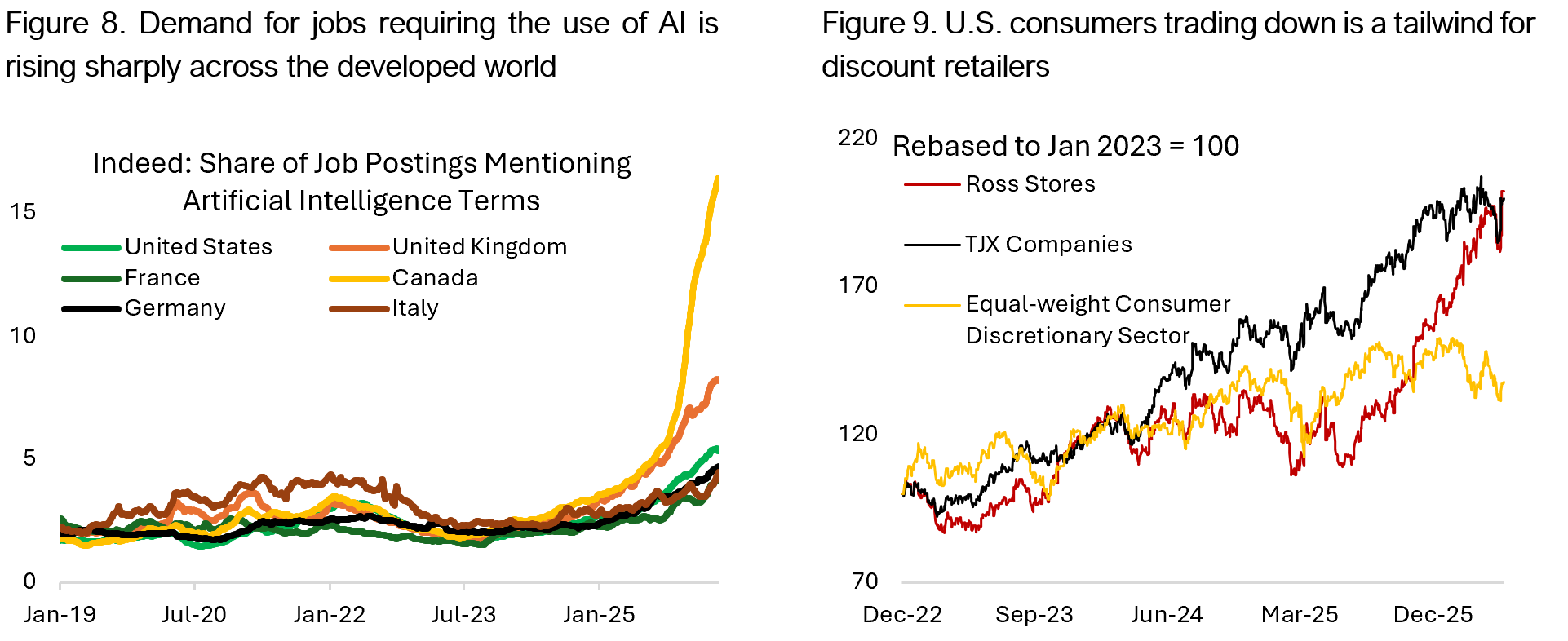

The broader concern is the emergence of a bifurcated society, where access to technology and capital determines economic outcomes. This could hinder the mobility of lower-income groups to access education, healthcare, job opportunity, and better life in general. Governments are beginning to explore measures such as increased taxation on AI-related profits and greater regulatory oversight of dominant technology firms. This trajectory echoes themes seen in science fiction, such as the film Elysium, where technological advancement coexists with deep social inequality. With that said, it is not all doom and gloom. At the same time, AI is an opportunity for workers who are able to leverage the technology and use co-working tools to increase their efficiency. Figure 8 shows Indeed tracker of jobs requiring the application of AI has surged in Canada and the U.K., outpacing those in the U.S. This is interesting as both countries have seen much lower productivity growth in the recent decade. Perhaps, application of AI tools could be an equalizer for workers in lower-productivity countries to catch up with their counterparts.

In the near term, this leaves us with a relatively downbeat outlook for lower and middle-income consumers. For almost two years now, U.S. consumers have been trading down their consumption – one of the reason discount retailers such as ROST and TJX have done relatively well (Figure 9) as people look for better value. There is scant evidence that the macro headwinds have turned, based on the commentaries we heard during the Q1/26 earnings season:

- Kraft Heinz Co. Chief Executive Officer Steve Cahillane said that poorer households were “literally running out of money at the end of the month.”, requiring them to tap into their savings for the purchase of necessities.

- Walmart noted that its customer gains were being led by upper-income families, indicating that the more aspirational luxury shopper perhaps isn’t immune from some of the cost pressures hitting the middle class. Also, “…when I look at the consumer, especially here in the US, they’re telling us they’re feeling some pressure and they’re looking to Walmart for value… the high income customer is spending with confidence… while the lower income consumer is more budget conscious and perhaps navigating financial distress… the number of gallons that customers fill up with when they come to our fuel stations fell below ten for the first time since 2022. That’s an indication of stress.”

- Kimberly Clark: “Consumers in a market like North America are really under stress. And while our premium business continues to grow… 90% of the population has incomes at $100,000 or below… as category leaders, we don’t really want to ignore the bulk of the population. And so we decided to innovate as aggressively in our value tiers.”

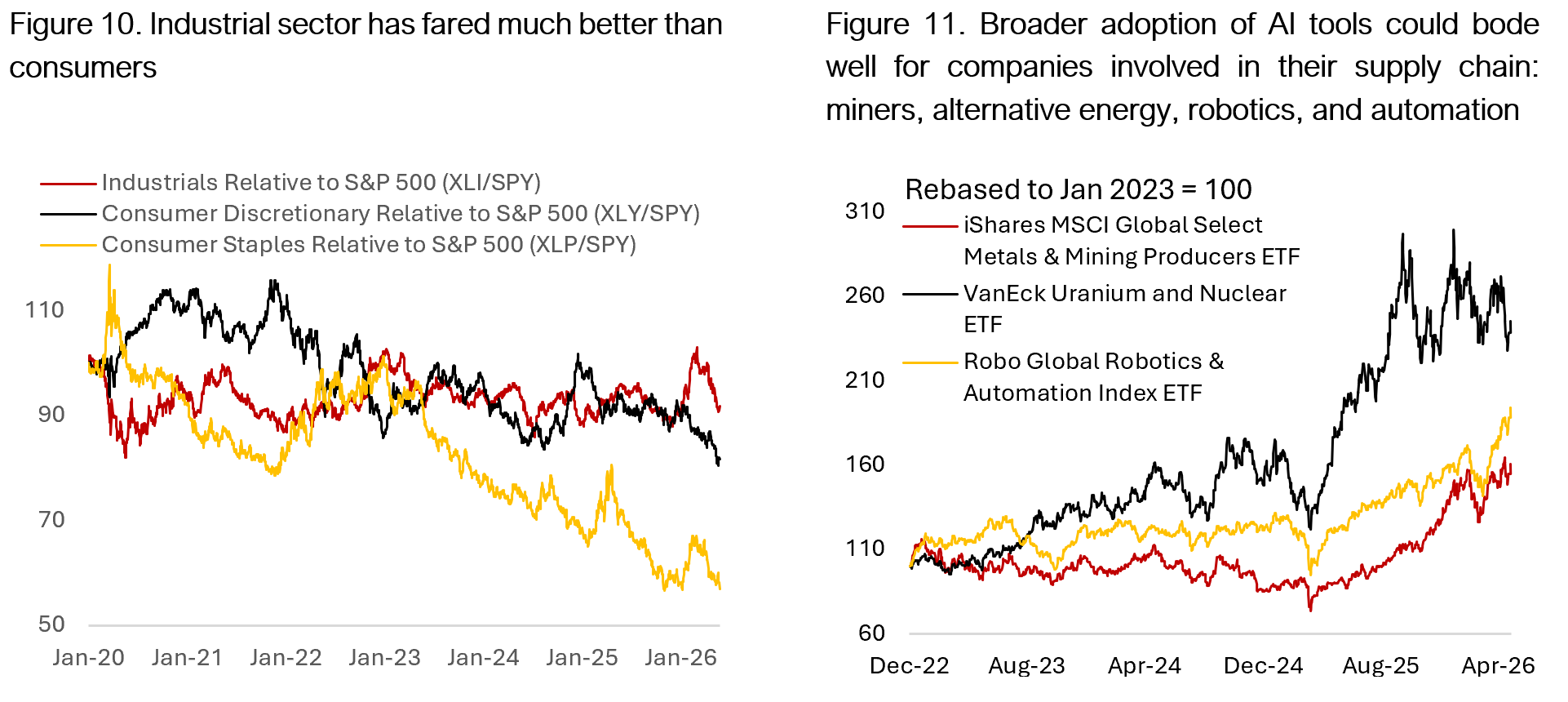

Back to our core theme that this is an industrial-led cycle, we believe there are still legs in the more cyclical parts of the economy (Figure 10), and the potential for physical AI could be another tailwind for companies involved in automation and robotics (Figure 11).

Conclusion: Navigating a Transitional Era

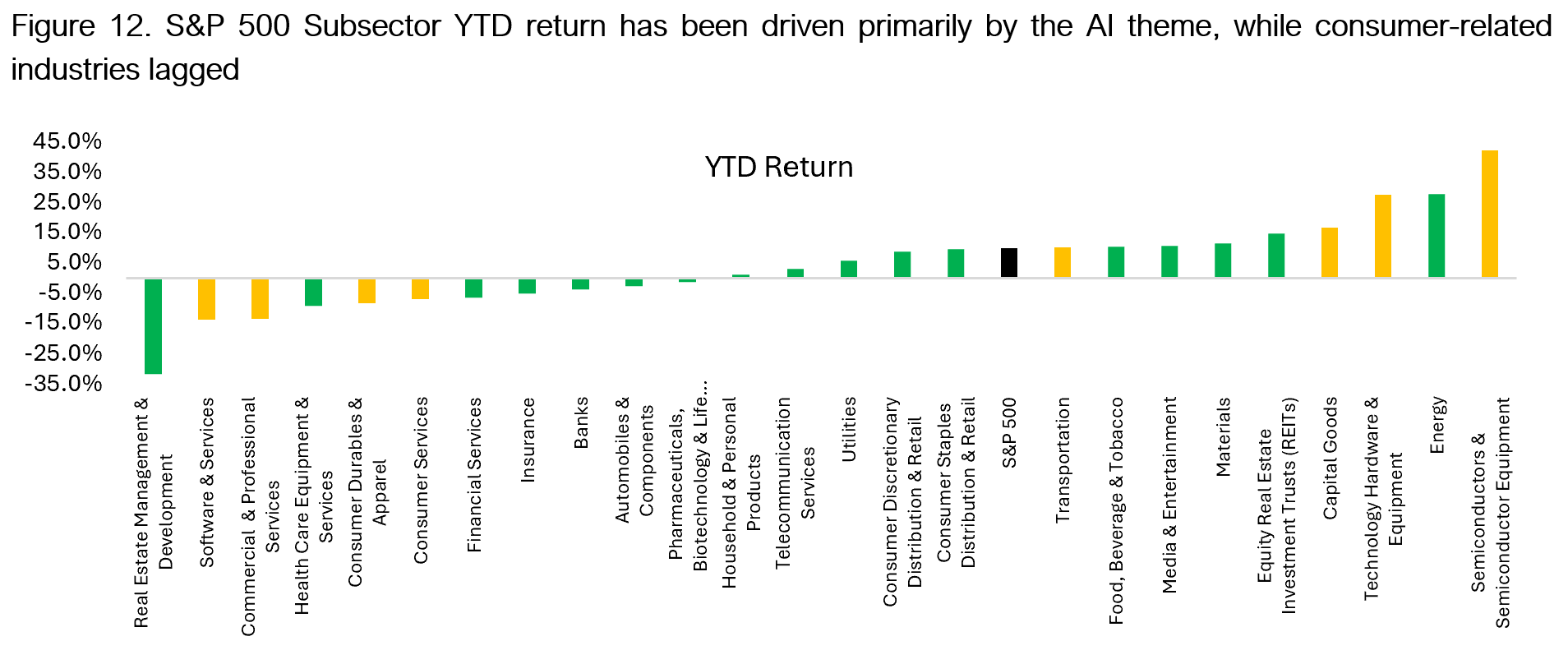

In this evolving landscape, certain sectors and asset classes are positioned to benefit, while others face significant challenges. Winners include the AI and semiconductor ecosystem, which sits at the center of the current investment cycle. Industrials linked to infrastructure development, as well as commodities and energy, also stand to gain from increased demand and strong pricing power (Figure 12). On the other hand, rate-sensitive sectors such as housing and real estate face headwinds from higher interest rates. Long-duration growth assets are vulnerable to yield spikes, and fixed income continues to struggle in a rising rate environment.

Copyright © 2026, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.