Download PDF:

EM local-currency bonds

- EM bonds still have room for spread tightening against U.S. Treasury. The 10-year Treasury yield will have difficulty to break 1.2% level as the Fed is unlikely to raise rate until inflation overshoot its 2% target, creating an anchor for yields globally to remain low. Moreover, the relatively modest fiscal stimulus across EM countries versus its DM counterpart warrant a reduction in country risk premium, with the notable exception of countries that are facing increasing share of interest payment on their fiscal resources such as Brazil and South Africa.

- In the shorter-term, however, rise in Treasury yield could lead to rebound in the dollar and trigger a temporary selloff in EM currencies and bonds, which have rebounded sharply. Moreover, the recent increase in food and oil prices, and rebound in economic activity mean headline inflation is likely to rise in the coming months, reducing the real yield and attractiveness of holding local-currency EM debt.

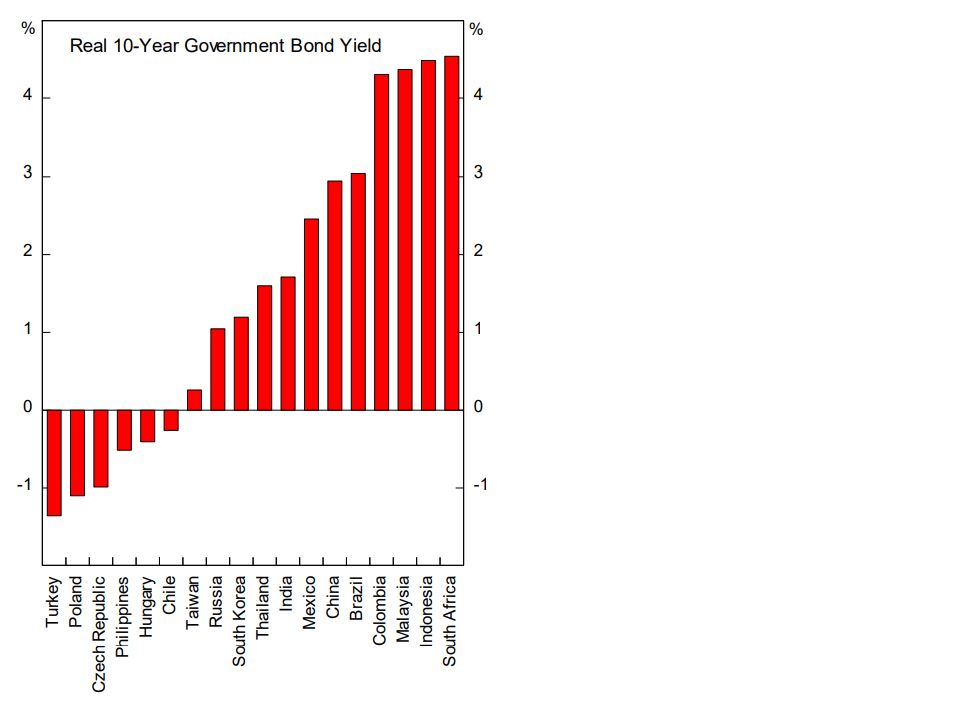

- Investors need to be selective in country selection as EM countries are facing idiosyncratic risks. Our overweight recommendation includes South Africa, Indonesia, Mexico, and Brazil’s local-currency bonds. Both Indonesian and Mexican government’s fiscal stimulus last year is modest, and these countries public debt levels are sustainable. Mexican peso is still 12% undervalued, according to our fair value model, and Indonesian bond’s real yield is among the highest in EM. Meanwhile, we see the case for tactical long position in South African and Brazilian bonds, despite the well-known high public debt level, as both countries’ currency is deeply undervalued and improving terms of trade from rise in commodity prices means spread could still tighten.

Brazil

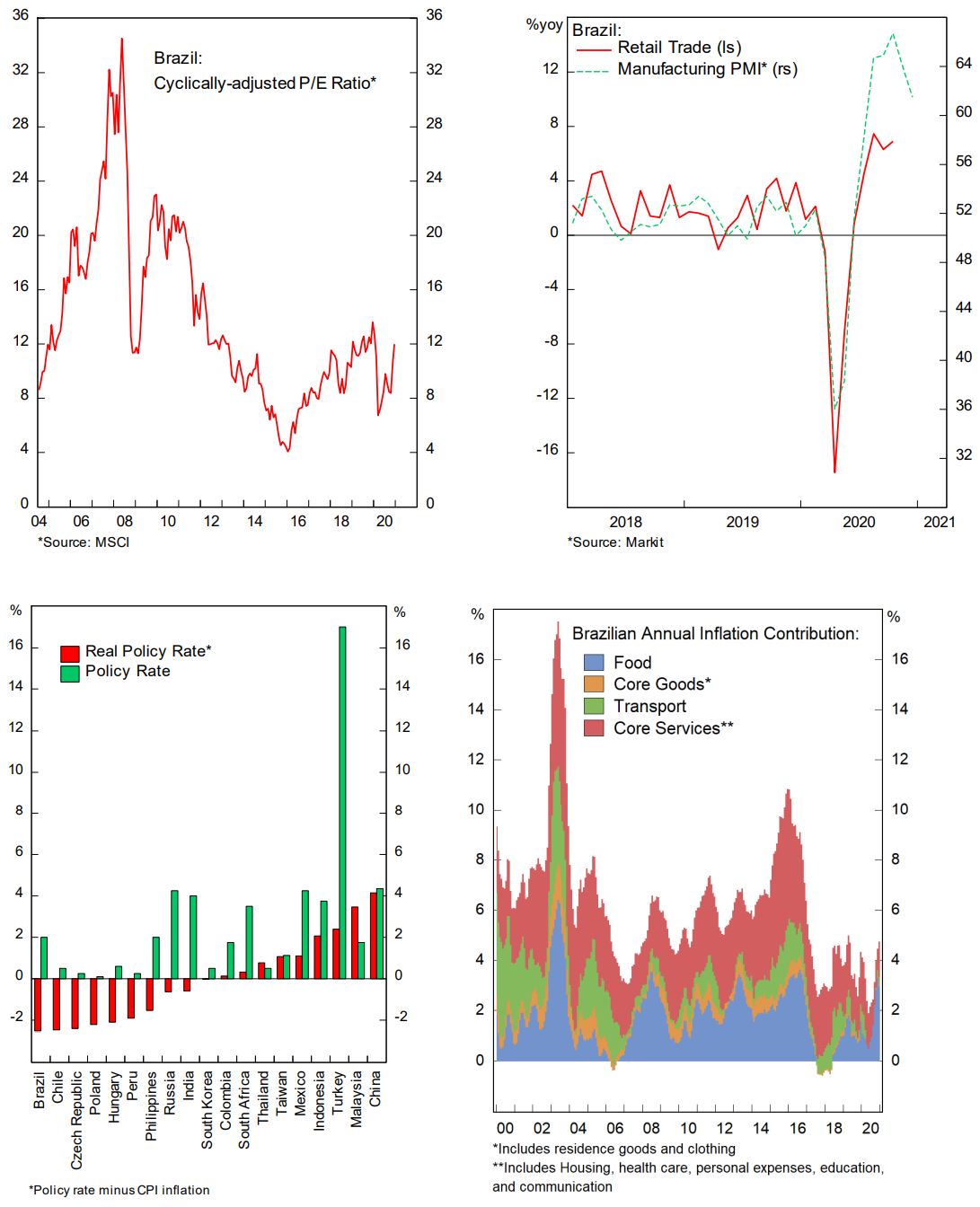

- Brazilian equities and currencies remain attractive on absolute and relative basis, at a time when commodity prices and the country’s terms of trade is improving, which will lead to rise in equity earnings and provide tailwind for the real. Moreover, large fiscal stimulus in response to the pandemic last year has helped the economy to rebound much faster than other Latam countries, with retail trade and manufacturing PMI surging to a record high level.

- Since the second half last year, we have been more bullish on Mexican peso relative to the BRL, a stance that has been well rewarded, but potential rate hike from record-low level by Brazilian central bank could be what the market needs for the real to finally outperform amid very low real yield relative to other EM currencies. The market is currently pricing in a 25-bps rate hike within the next 6 months that we think is driven more by domestic growth consideration rather than the recent tick in the country’s headline inflation, which is driven by higher food prices and does not warrant outright policy tightening.

- The risk for Brazilian assets lies in the country’s ability to quell the virus spread and continue its reforms, which have been put on a backburner as the country focus on the pandemic. Already there are reports that the government vaccination effort is mired in chaos that potentially hamper growth. Meanwhile, the legacy of high public debt level and sizable stimulus in response to the pandemic has left the government with few fiscal powders. With Bolsonaro facing re-election in 2022, it is doubtful that fiscal spending would be reined in significantly this year. In addition, should fiscal (tax) reform be further delayed and domestic political environment worsen, the country’s bond yield could march higher.

Turkey

- Sweeping changes in the Ministry of Finance and replacement of the governor of Turkish central bank have brought back orthodox policies and boosted investors confidence on Turkish assets. Policy rate is now back above CPI inflation and the new governor has committed to a tighter monetary policy to curb inflation and building up the country’s grossly inadequate reserves. As a result, the Lira has been strengthening of late, which will cap inflation from creeping higher.

- Turkish economy has staged a V-shaped rebound last year that is fueled by credit binge. Current tighter monetary policy comes amid the backdrop of easy global liquidity, weakening dollar, and rebound in global growth that could allow the country to escape another crisis or significant growth slowdown. Moreover, Turkish bond’s high carry amid the outlook of declining inflation potentially attract high risk-tolerance investors to load up on Turkish local-currency debt and drive inflows back into the country, making it easier for the country to build up foreign-currency reserves.

- Turkey’s equity and currency valuations are both deeply discounted and reflect worst-case scenario for the country, with significant upside should it be avoided. The stock market is currently trading at 1x book value and 7x forward earnings, whereas the Lira is still trading 24% below our fair-value assessment after the recent sharp rally. With inflation set to decline, the adjustment to Lira’s undervalued real exchange rate will come from nominal appreciation.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.