Download PDF: Brazil and South Africa Update

- Brazil’s economy is slowing, but positive development on pension reform has charged the market of late. Much of the positive development has been priced in and the risk of further slowdown in the economy is rising.

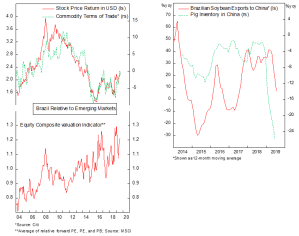

- Brazilian stocks are not cheap relative to EM overall, currently at its 96th The 70% rally in iron ore prices this year are likely overdone and the depletion of pig population in China has reduced demand for Brazilian soybean. These factors will weight Brazilian terms of trade and stocks to advance further.

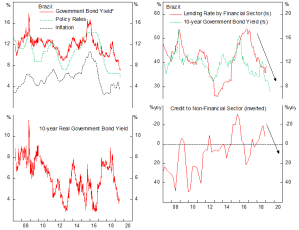

- Decline in policy rate and government borrowing rate are likely to depress corporate borrowing cost of further, which is good news for credit creation. Meanwhile, inflation will continue to stay benign as the economy weaken and government bonds still provide attractive return profile compared to rest of EM.

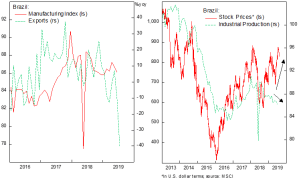

Brazilian equity market is currently near its three-year high on the backdrop of optimism of pension reform that last month passed the lower house of congress with the help of Rodrigo Maia, the house speaker with whom Bolsonaro’s son has a spat earlier this year. However, counterforces are lurking in the background; the economy is slowing down, driven by the contraction in manufacturing sector, and demand for Brazilian export products are decelerating. Q1 2019 GDP growth is a paltry -0.2% QoQ and Q2 data release at the end of the month will likely to disappoint as well. Brazilian manufacturing sector PMI in July is contracting for the first time since June last year and exports have slumped as global demand slows.

Meanwhile, Brazilian equities have year-to-date rallied 15% after peaking at 22% in July, massively outperforming EM equities 3.5% rally. This has push Brazilian stocks’ valuation relative to EM to a near record level, currently at its 96th percentile since the data available in 2004. Brazil’s stock market is dominated by growth-sensitive sectors, namely financial, energy and material sector that comprise 64% of the index, making it highly procyclical.

The outperformance in Brazilian coincides with its improvement in terms of trade, mainly driven by the 78% rally in iron ore prices up to last July, before correcting to 54% this month. Recent slump in commodity prices due to trade war escalation, global manufacturing recession and swine flu fever in China will likely depress economic activity in Brazil further. Stay underweight Brazilian equity in EM portfolio.

Last week escalation of the trade war and risk-off sentiment have sent emerging market currencies depreciating and yields rising. We continue to maintain our positive view on Brazilian government bond, as inflation remain benign and 4% real yield is attractive across EM universe. In the longer run, lower lending rates will likely accelerate credit creation in the economy and boost investments, helping Brazilian firms to expand and trigger a positive feedback loop in corporate profits.

On South Africa

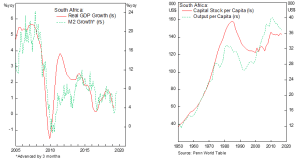

- The long-term outlook for South Africa’s economy is gloomy, but the country is at its cyclical bottom. Low savings rate and weak government have hindered investment in the country, resulting in lower productivity and higher unit labor cost in the economy. This is highlighted by the high and rising unemployment rate.

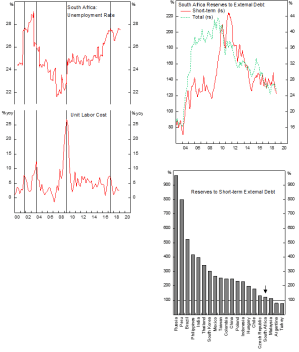

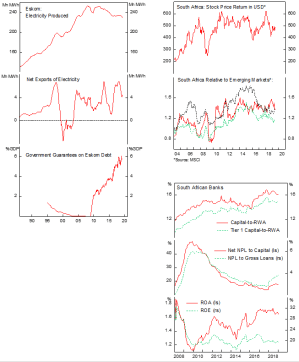

- The country external risk profile is weak. International reserve is only slightly above its total short-term foreign currency debt and ranks poorly among Emerging Markets countries. Government guaranteed debt on Eskom, its national electricity company, jeopardize the country’s external profile further and a rating downgrade is likely.

- South African equities have lagged its Emerging Markets counterpart since 2015, but the monetary easing, prospect of government reform by curtailing public sector salary and boosting developmental and infrastructure expenditure and improving short-term outlook, may trigger a rally in stock prices. South African banks are well capitalized, highly profitable and well positioned to profit from the trend.

- Fighting between Ramaphosa and Zuma faction within the ANC party, and the corruption accusation against the president may leave the government paralyzed in doing further reform. Should Ramaphosa failed to pass the required land reform, it is likely that South Africa is going to undergo a prolonged period of stagnation.