When I was working as a junior doctor many years ago, one of my professors always stresses the importance of determining the cause (etiology) of a disease rather than simply alleviating the patient’s symptoms. The collapse of SVB in March and the associated ripples to other regional banks are one of the many symptoms of a tight monetary conditions that commonly occur during the late phase of the business cycle. A good doctor will try, without the guarantee of success, to both eliminate the cause of the disease and lighten the patient’s symptoms, rather than doing the latter only. Regulators guarantee on uninsured deposit could temporarily calm the market and prevent depositors from withdrawing their money from smaller banks, but it is short of fixing the true cause of the problem, which is tighter liquidity (Chart 1).

The Fed has a strong past track record of overtightening monetary policy until something breaks. Well, now something did break, but given that inflation is still far too high the Fed cannot simply cut policy rate and pause its quantitative tightening. Without inflation being a problem, the Fed would probably cut its policy rate following the market fiasco in March. The question now is whether the Fed can tweak its monetary policy to achieve a balance that allows inflation coming down to its 2% target while maintaining stability in the system. Our base case is that the Fed will be forced to cut policy rates in H2/22 as the lagged impact of previous policy rate hike push the U.S. economy into a recession and cause a spike in unemployment rate.

What worries us today is that banks will dramatically tighten their lending standard amid competition for deposit and deteriorating borrower’s credit outlook, creating a credit crunch for businesses and force them to further cut capex and lay off their employees. This, in turn, will cause a slump in consumer spending and higher default rate (Chart 2).

On inflation, we are on the camp that think it will eventually come lower to pre-pandemic trend, mainly due to structural factors. Both population and productivity growth in the U.S. is below 1%, and the rest of the developed world is going through a Japanification, despite the medium-term threat from deglobalization. More importantly, the market is doing Fed’s job in tightening financial conditions, lessening the need for policy rate to go much higher from current level. The chaos surrounding SVB’s bankruptcy saw both tighter financial conditions and lower Treasury yields, which are not contradiction. The bond market is currently pricing in a terminal rate of 4.8% from as high as 5.7% just few weeks ago. Although we are concerned on the resilience of service, ex-housing inflation that is driven by strong wage demand, we also think that a recession and spike in unemployment rate will force labor to be a price taker, which is deflationary.

Credit Crunch Ahead: The Already Tightening Lending Standard Will Get Even Worse

The largest implication of stress among regional banks is that they are going to be more conservative in issuing loans and compete more vigorously for deposit, which is negative for their earnings outlook. Even before SVB’s bankruptcy, lending standards have tightened to a level that historically led to a recession (Chart 3). With the Fed already raising 450 bps over the past year alone and signs of stresses are emerging, main street’s access to credit (volume) likely become more difficult to obtain while spreads (price of credit) should also continue to rise.

We are concerned on the balance sheet strength of banks with less than $250bn in assets, which account for roughly 60% of residential real estate lending, 80% of commercial real estate lending, and 45% of consumer lending. The first two sectors have cooled significantly amid higher rates, with both residential and office property values falling and their income barely catching up with the increase in borrowing cost.

Meanwhile, the pressure for banks to compete for deposit will increase as long as policy rate remains high and quantitative tightening continues, raising their funding cost at a time when loan demand is weakening amid slowing economy and higher rates (Chart 1 and Chart 4). Regional banks account for 35-40% of all bank lending in the U.S. and is an important intermediary for small and medium enterprises (SMEs) who do not have access to the capital market. This means the impact from tightening lending standards will hit smaller businesses harder than large corporations with access to the debt market, which is concerning given that SMEs employed a significant portion of the labor force. This is the reason we expect the labor market to cool faster for the rest of the year, as businesses will be forced to cut down their capex and hiring plan to protect their margin.

A Quicker Normalization of the Labor Market

The currently elevated vacancy rate in the labor market is driven primarily by workers demand from firms with less than 250 employees, which together account for over 70% of the total vacancy rate (Chart 5). As discussed above, the high likelihood of recession and greater difficulty in obtaining financing should lead to SMEs moderating their hiring plan, if not going for an outright lay off.

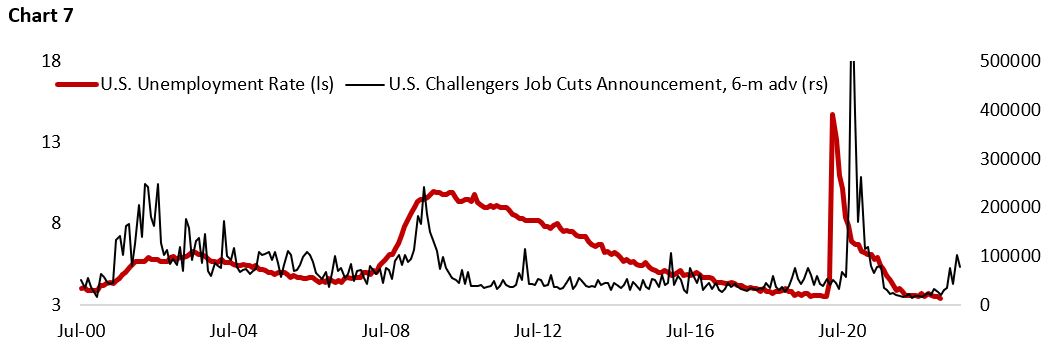

Already we are seeing early signs of cooling in labor demand in the January and February labor data. First, demand for part-time workers, which tend to adjust faster to the business cycle, is lower than the previous year. Chart 6 shows that change in demand for part-time employees has consistently led the direction of change in headline employment by 6 months (Chart 6). Second, we also expect that not only new demand for workers to cool, but businesses will also accelerate their effort to trim the fat in their operation. Challenger data points to a rise in unemployment rate in the coming two quarters (Chart 7).

Consumer Spending Will Turn from Fire to Ice

If we are right that the labor market is going to significantly worsen from here, consumer spending will inevitably fall. Not only consumers have been suffering higher inflation and higher borrowing rates, but their wealth has also been eroded over the past year from lower house, stock, and bond values. The declining real wealth should eventually lead to the deterioration in the outlook for their personal finance and translate to a pullback in spending (Chart 8). Housing sector activity, the most rate-sensitive sector has already weakened since mid-2022 and it historically led broader consumer spending by 12-24 months (Chart 9), which led us to the conclusion that the business cycle downturn will continue up until at least Q3/23.

Investment Implications

Since the Summer of 2022 we have been taken a more positive view on Treasury bonds relative to stocks amid the downturn in the business cycle, decline in earnings outlook and expensive equity valuation (Chart 10). We admit that we were several months too early and underestimated the strength and resilience of U.S. economy as consumer spending and the labor market have been stronger for longer than we forecasted. However, the trajectory of growth continues to be lower. The New York Fed Weekly Economic Index has declined to 0.96% from 2.05% at the end of December and 2.86% in June 2022. This is below average trend growth of 2% seen over the past decade.

We expect the decline in U.S. growth rate to accelerate in the coming six months due to the tightening in credit and consumer spending finally running out of steam. With our base case that inflation will continue to drift lower and the economic damage from higher rates will become more obvious, the Fed will likely have to cut rates later this year. This supports our view that Treasury yields will likely fall below 2.5% at the cycle bottom. Meanwhile, we expect the gap between 10-year yield and copper-to-gold ratio to narrow, with the former likely catching to the downside (Chart 11).

Within equities, we expect a rotation back to defensive sectors and quality names, which still have plenty of room for outperformance. Following its peak at 19.2x in early February, the S&P 500 forward P/E has now fallen to 17.5x, while equity risk premium rose from 1.4% to slightly above 2% (Chart 12). But at these levels, U.S. stocks are nowhere close to a level that would consider as cheap. The lagged impact of tighter monetary policy will continue to be felt at least until Q3/22 and is a significant drag to earnings. Our base case scenario for the S&P 500 entails forward P/E to decline lower than 16x (Chart 13) while forward earnings to fall to $190-200 level at the market bottom (Chart 14), which translate to a potential low around 3040-3200.

Copyright © 2023, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.