Download PDF: Q12019_LATAM_EMEA_Update

A revisit of our investment thesis on emerging markets equities

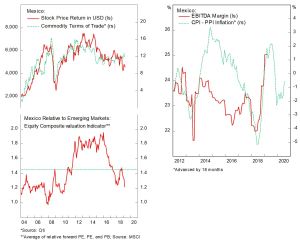

Mexico + (Overweight)

Last year Mexican stocks were among the worst performer in the EM universe for two main reasons. First, the domestic economy is experiencing a sharp slowdown from industrial and oil production. Second, the increase in global risk aversion has shifted the flow of fund out of emerging market countries, especially those with twin deficits. To stem the weakness in Mexican Peso, the Central Bank raised rates four times to 8.25%.

This year, the reverse power should be at work. As the Federal Reserve is expected to hold or even cut interest rates, Central Banks across EM should be able to reverse the monetary policy toward easing and fund flow to EM assets should increase further. The effect is two-fold: 1) easing monetary condition drives manufacturing activity higher and increase corporate profitability as cost of borrowing decreased, 2) Money flowing inside the country will be a catalyst to bring Mexican equity valuation back to historical level.

On a short-term basis, the risk in Mexican assets is driven by two main factors. First, PEMEX overleveraged balance sheet and deteriorating profitability may induce another credit rating downgrade. PEMEX contributes 9% to government fiscal revenue and 10% of total exports. AMLO agenda to boost oil output, hence substantial investment in PEMEX, may result in a backlash if oil price slump. Second, AMLO unpredictable policy may be interpreted as a hostility toward the private sector, shunning foreign investment in the country.

Mexican equity is trading at an attractive level and we overweight the country in EM portfolio. We argue that Mexican equity index should be trading at a higher multiple relative to EM amid the domination of consumer staples and communication services sector in the index, unlike most EM countries whose market are dominated by financials that generally trade at lower multiples. Currently it is trading at 18.8% discount relative to the historical average. On the earnings side, we also expect an increase in margin among Mexican corporates, which should give a boost to stock prices.

Turkey = (Overweight)

Last week the Turkish market is facing another government-made turmoil. As the country approaches local election date on March 31st, the government has been tightening the borrowing of Lira in the offshore market to defend the currency and avoid further inflationary pressure. The central bank may have also intervened in the foreign currency market as the gross foreign exchange reserves dipped US$ 5.3 billion.

The difficulty for foreign investors to hedge their Lira position translates to higher borrowing cost in the domestic market and triggered a sharp selloff in the equity and bond market (10-year yield increased 170 bps and stock price in LXR declined 7%).

On the fundamental side, however, the economy is showing signs of improvement. Inflation continue to abate to 19.7% in February, driven by lower inflation across categories except for food prices, which only fell slightly from its January top. Business confidence, a leading indicator for industrial production, has been surging and exports growth remained at a healthy level.

Turkish equity, currently trading at 6.9x forward earnings, remain as one of the cheapest markets in the world. Earnings are set to improve after 20% contraction last year as Turkish stock market is dominated by industrials firm (21% of market cap) with export-oriented revenue, which should benefit from a cheapened currency.

Turkish banking sector is especially attractive at 0.54x book value and capital ratio is at a healthy level being above Basel III standard. Net NPL increase only by 20 bps despite gross NPL increasing above 100 bps as provision for bad debt continue to eat banks’ margin. Lira’s stability and improvement in general business condition should give a boost to Turkish bank as earnings improve and multiples normalize.

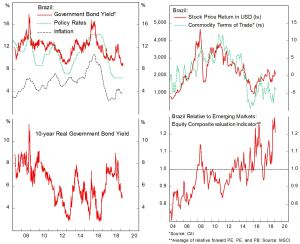

Brazil – (Underweight)

The honeymoon period of Bolsonaro’s presidency seems to be over. The market had put high hope that he would be able to pass the long-awaited pension reform bill, which is now fading along with the drop in Bolsonaro’s approval rating (34%).

There are several reasons for market’s pessimism. First, Bolsonaro may be distracted from his government agenda by the problems inside his own family, especially relating to his sons. Flavio Bolsonaro is under investigation for corruption and Carlos had been publicly clashing with politicians (Rodrigo Maia, the president of lower house, who later retaliate by convincing his allies to not show up on the hearing) whose support are important to pass the pension reform bill.

Second, the president’s credibility is also being questioned after he fired Gustavo Bebianno, the Secretary General, due to campaign financing scandal of his Social Liberal party. Carlos Bolsonaro, backed by his father, had been denying the existence of negotiation between Bebianno and Bolsonaro, which later proved to be a lie.

Third, the arrest of Michael Temer, the former president and leader of the biggest party (PMDB), may also complicate the matter as investors perceived that it will shift the legislative attention from the pension bill.

Meanwhile, Brazilian economy also start to show signs of weakness. Despite the bullish business sentiment after the election, hard data shows that industrial production is contracting, creating a divergence between soft and hard data. Moreover, economic growth post-2016 recession has also been weak despite the aggressive 775 bps cut in policy rates, which should put the Central Bank on easing bias. In fact, the current 3-month bill rate is below the SELIC target rate, which historically preceded an interest rate cut. Inflation number has also been low at 3.77%, below the Central Bank’s 4.25% target. All of these factors are bullish for bonds.

Brazilian equity, on the other hand, is expensive relative to EM and historical level after rallying since the middle of last year. The uncertainty related to the pension reform bill and prolonged weak growth should demand lower multiple on Brazilian equity relative to the rest of EM. We are downgrading Brazilian equity to neutral for the next quarter.

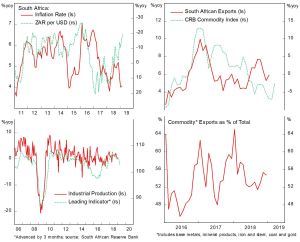

South Africa = (Overweight)

Economic activity in South Africa is very weak and will likely continue to be so this year. Historically a depreciation in the Rand will exacerbate inflation to go on an upward spiral due to higher cost of import goods. However, since late last year the depreciation in Rand is accompanied by lower inflation, highlighting the weakness in domestic economic activity. Latest industrial production figure also show that manufacturing activity is on the brink of contraction, supported by leading indicator pointing downward.

The fluctuation in commodity prices, especially base metal and gold, greatly affects South African economy and exports. Hence, the sharp decline in commodity prices and heightened risk aversion last year are a double whammy for South African stock prices, which declined by more than 20%. Foreign investors record a net investment outflow from both stocks and bonds since the second quarter last year, only to come back to the bond market this year.

On the surface, equity valuation in South Africa does not look particularly cheap. However, if we look deeper into the breakdown, the valuation picture is skewed by Naspers, owner of 46.5% Tencent stocks (P/E 36x). Moreover, the larger weight of materials sector compared to EM average also skewed the P/E and forward P/E ratio upward during the downturn, which is happening in South African economy currently. Looking solely on the P/B ratio, South African equity is currently trading at 10% discount relative to historical average (2.13x against the average of 2.37x).

Foreign investors have also been coming back to South African bonds, which has historically been accompanied by inflow to the equity market as well. The sharp correction last year and prospect of bottoming in the global manufacturing sector this year are tailwinds for South African equities to rally this year.

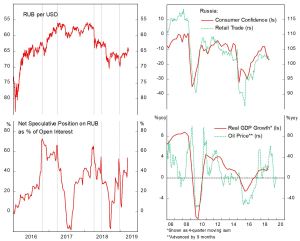

Russia = (Underweight)

Apart from the political pressure from U.S and European countries, Russian domestic economy is also facing several challenges. First, the 40% drop in oil price last year will be a drag for growth in 2019. A 10% increase in oil price has been historically associated with 1% higher GDP growth in Russian economy (see chart). Second, consumer confidence and retail sales have been trending lower as a result, after peaking in the second quarter last year as the rubble depreciates 17% last year and inflation creeps back to 5% level. Meanwhile, to counter the slowdown, Russian Central Bank’s ability to ease policy rates is rather limited.

We maintain our “Underweight” recommendation for Russian equity as it continues to be a value trap for investors. Energy sector is contributing 60% of Russian equity market cap, especially related to oil and natural gas, making the stock market highly correlated with oil prices. Speculative position on Rubble is also currently at a historically high level, a reliable sign of reversal in the past.