Download PDF: TLKM_March2019

Continued Transformation to Data-based Revenue

Rising Cost Hurts the Bottom Line

Maintain Buy Rating with Target Price of Rp 4450/share

Telkom’s 2018 annual report is likely to be disappointing, based on the recent trend in the sector and third quarter statement. After years enjoying high return and strong growth, the sector is challenged by a combination of two factors: rapid decline in voice and text revenue, and fierce competition in the rapidly growing data-revenue.

Contribution from telephone usage and SMS revenue continue to shrink at an accelerated pace due to transition from voice and text to internet-based application. As per 3Q18 both segments continue to contract by 19% and 29%, respectively, which we expect to continue decline at double-digit rate in the coming years. However, strong growth in revenue from data more than offsets the decline by growing at a rate above 20% YoY. By 2022, we expect data revenue to contribute 74% of TLKM’s total revenue.

Low Average Revenue per User (ARPU) in Indonesia will be a positive long-term factor for TLKM’s growth. However, the price war among the three major telco company last year has hurt their bottom line, with consumers being the beneficiary. That is the reason for weak revenue growth in 2018 despite strong subscriber growth. It is likely that this year the competition for market share will ease and each player to focus on operational efficiency after a burgeoning operating and G&A in 2018. We are expecting margin to stabilize in 2019 and 2020, before an improvement in 2021.

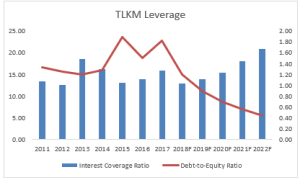

From balance sheet perspective, the higher leverage of ISAT and EXCL should put them into defensive positioning. Debt-to-asset ratio for EXCL and ISAT are around 40% compared to TLKM’s below 20%, which will constrain the ability to fund capital expenditure aggressively. The need to return to profitability will likely consume the management of both ISAT and EXCL to structure their internal operation rather than enacting another price war.

Using Free Cash Flow to the Firm valuation method, we derived the fair value for TLKM equity share at Rp 4550, with assumption of 12.2% WACC and 6.8% terminal growth rate. The fair value implies 24.1x P/E FY19 and 21.6x P/E FY20.