And a Once in a Decade Opportunity to Overweight EM Equity

In the last decade, Emerging Markets equity performance has been lagging its U.S. counterparts by a significant 50% margin. Undoubtedly, part of this is contributed by the gain of = hot technology stocks in the U.S. (FAANG). However, currently U.S. earnings growth is peaking out while EM’s may have just hit bottom, which could be the trigger for more manager to shift allocation to EM.

Since 2012, EM Relative decline in ROE vs U.S. has been accompanied by a greater amount of multiple contraction. It is unthinkable that going forward EM equity is going to underperform U.S. equity, even in the case of recession.

MSCI US and S&P500 Valuation Relative to World

At this point in time, should investors not have exposure to U.S. equity at all?

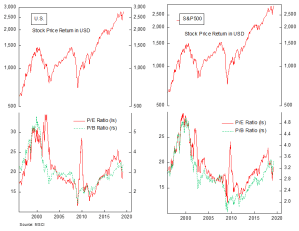

MSCI US and S&P500 Valuation

U.S. valuation is not ridiculously high based on its earnings, but record high margin is a concern for the current valuation.

SPX Profit margin