Facebook-Instagram

Something that first look like megalomania turns out to be the smartest technology acquisition of the decade. Mark Zuckerberg decision in 2012 to acquire Instagram, a two-year-old photo-sharing app with 30 million users for $ 1 billion, turns out to be one of the best decisions he made. Forbes estimates Instagram currently worth $ 25-50 billion with 400 million users, while Citigroup values it at $ 35 billion in 2015. Credit Suisse analyst expects Instagram to generate $ 3.2 billion in 2016. Today, Instagram has over 300 million users. As a note, Facebook market cap in October 2016 is $ 370.37 billion.

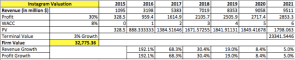

Using analysts projection of revenue growth, I’m valuing Instagram using Discounted Cash Flow (DCF) model through 2021. Growth is high during the next 5 years, and decline steadily to 5% in 2021, terminal growth is expected to be 3% (in-line with US GDP growth). Average WACC of Facebook (Instagram parent’s) is 8%, I discounted the expected profit and arrives at the present value of each year profit. Terminal value is derived from 3% terminal growth until perpetuity. With the estimates outlined, I arrived at Instagram firm value at $ 32.77 billion; the estimate is in line with Forbes $ 25-50 billion valuation.

Figure 6.1 Instagram Valuation Table

From the valuation above, I would say Instagram acquisition by Facebook is a huge value creation to shareholder’s value. For only 4 years, Instagram value has increased from $ 1 billion to $ 32.77 billion, an annual compound growth of 240%. Even in 2015, Instagram revenue exceeds $ 1.095 billion with profit around $ 320 million. In this year alone, Instagram is expected to record a profit of almost $ 1 billion from the ads revenue it generated. Valuation aside, youngster saw Facebook as their parent’s social media while Instagram was seen as something vibrant and energetic. The acquisition diversifies and broaden Facebook market segment. Those are reasons of why I believe Facebook acquisition of Instagram is a value-creating decision.

Facebook-Whatsapp

Facebook acquisition of Whatsapp amounts to $ 19 billion, $ 15 billion of Facebook stocks and $ 4 billion cash. At the time, Facebook PE was 116x, a lofty valuation in traditional sense. Referencing to Aswath Damodaran calculation, $ 19 billion valuation could be justified by $ 1.52 billion of profit in a steady state; meanwhile Whastapp is expected to generate only 30 million revenues (not profit) in 2016. Whatsapp doesn’t generate revenue from advertisement and since 2016 it doesn’t charge $ 1 customer fee anymore. The revenues Whatsapp generated derives from the data it provides to be used by Facebook data analytic via transfer pricing. It could be said that Whatsapp alone doesn’t generate revenues, but it enhance the revenues of Facebook (synergy).

Figure 6.2 Whatsapp Valuation Table

From various analysts expected growth rate, I projected Whatsapp revenue and EBITDA for the next 8 years and use DCF method to arrive at the firm value. Using 8% WACC (Facebook CoC) and 3% terminal growth, I estimate the firm value of $ 2.4 billion, well below the price Facebook paid. But remember that $ 15 billion was paid using Facebook stock, which essentially costs nothing to Facebook itself and justified by the synergy that may results from interaction between social medias. It may also took long time and more capital for Facebook to have its own “Whatsapp” built in house. So essentially, Facebook may only overpaid $ 1.6 billion for Whatsapp. But nevertheless, should Facebook be able to monetize Whatsapp revenue significantly, the purchase may be justified in the future.